Zero-based budgeting sounds a little strict at first, but it’s really just a simple way to tell your money where to go.

Zero-based budgeting gives every dollar a specific purpose before the month begins. That does not mean your bank account should end at zero. It means your income is assigned to bills, savings, debt payments, groceries, spending money, and anything else your month needs.

Instead of waiting to see what is left over, you make a plan for the money before it disappears.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

Quick Overview: Zero-Based Budgeting

- Zero-based budgeting means giving every dollar a clear job before the month begins.

- Your budget should end at zero on paper, but your bank account should not hit zero.

- Savings, debt payments, bills, groceries, and spending money all count as part of the plan.

- This method works best if you want more control over monthly spending.

- It can feel detailed at first, so start simple and adjust your numbers as you learn your real expenses.

What Is Zero-Based Budgeting?

Zero-based budgeting is a budgeting method where you plan your income until every dollar has a clear purpose.

That does not mean you spend every dollar. Savings, debt payments, emergency fund contributions, sinking funds, and extra payments all count as part of the plan. The “zero” simply means there is no money left unassigned on paper.

For example, if your take-home income is $3,000 for the month, your budget categories should also add up to $3,000. That might include rent, groceries, utilities, transportation, savings, debt payments, personal spending, and a small buffer.

In personal finance, zero-based budgeting is much simpler than the business version of zero-based budgeting. You are not justifying company expenses from scratch. You are deciding where your own money should go before the month begins.

This makes the method useful if money tends to disappear without a clear reason. Instead of guessing what you can afford after spending, you make a plan first and adjust as the month goes on.

How Zero-Based Budgeting Works

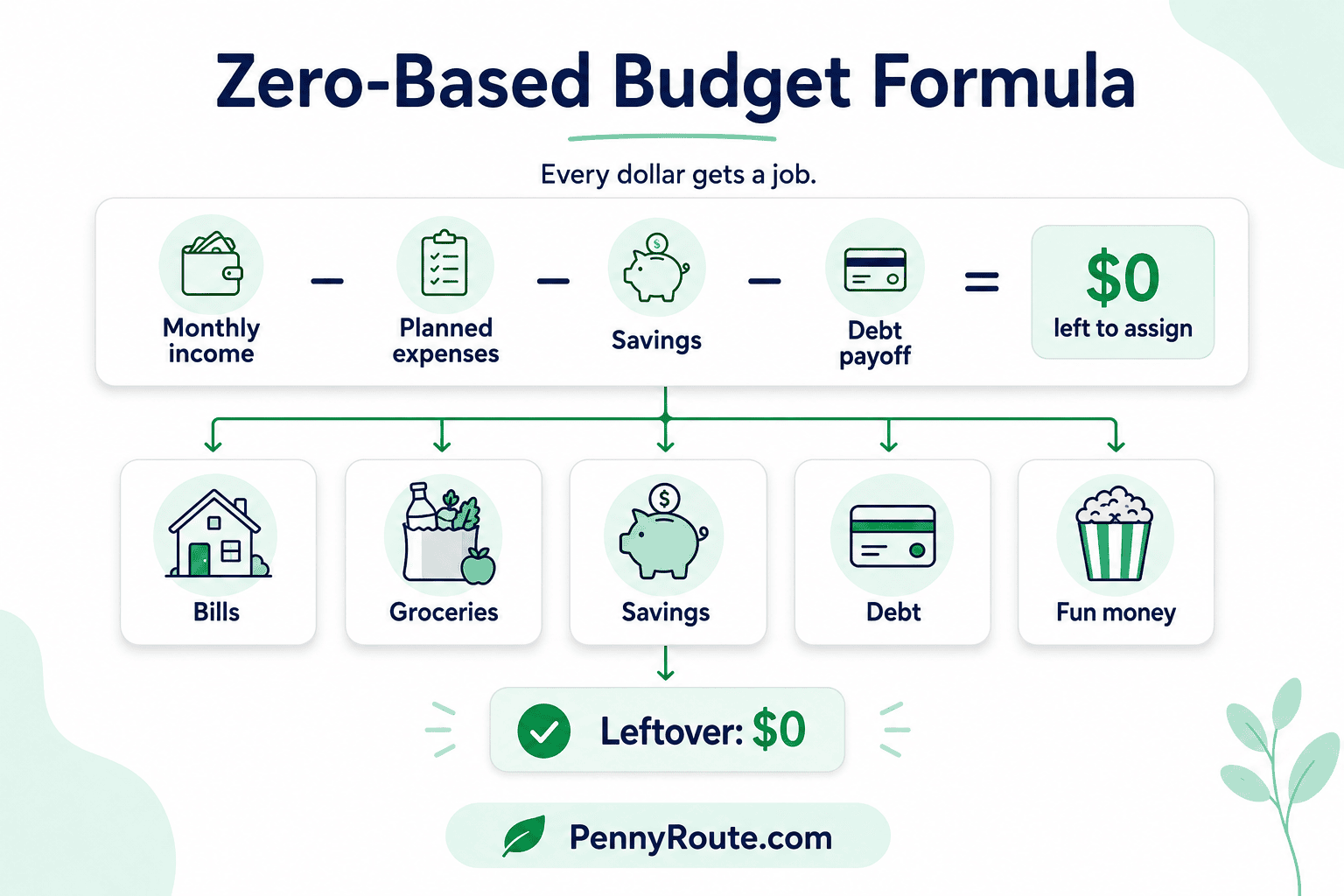

Zero-based budgeting works by planning your money before the month starts instead of waiting to see what is left.

You begin with your expected take-home income. Then you assign that money to the categories your month actually needs, such as rent, groceries, utilities, transportation, savings, debt payments, personal spending, and a small buffer.

The basic formula is:

Income – Expenses – Savings – Debt Payments = $0

Formula

That zero does not mean your checking account should be empty. It means each dollar has been given a job in your budget before it gets spent.

For example, if you bring home $3,000 for the month, your planned bills, savings, debt payments, and spending categories should also total $3,000. If you still have $150 unassigned, you decide where it should go before the month begins, such as savings, debt payoff, or a flexible spending category.

A Simple Zero-Based Budget Example

A zero-based budget is easier to understand when you see the numbers.

Let’s say your take-home income is $3,000 for the month. In a zero-based budget, you would assign that full $3,000 across your bills, savings, debt payments, and spending categories.

| Budget Category | Amount |

|---|---|

| Rent | $1,100 |

| Groceries | $400 |

| Utilities | $200 |

| Transportation | $250 |

| Insurance | $150 |

| Phone and internet | $100 |

| Minimum debt payments | $250 |

| Emergency fund savings | $300 |

| Personal spending | $150 |

| Eating out | $75 |

| Miscellaneous buffer | $25 |

| Total assigned | $3,000 |

| Money left to assign | $0 |

In this example, the budget reaches zero because every dollar has a planned purpose. Some money goes to bills, some goes to savings, some goes to debt, and some stays available for personal spending.

The important part is that savings are included before the month begins. They are not treated as whatever happens to be left after spending.

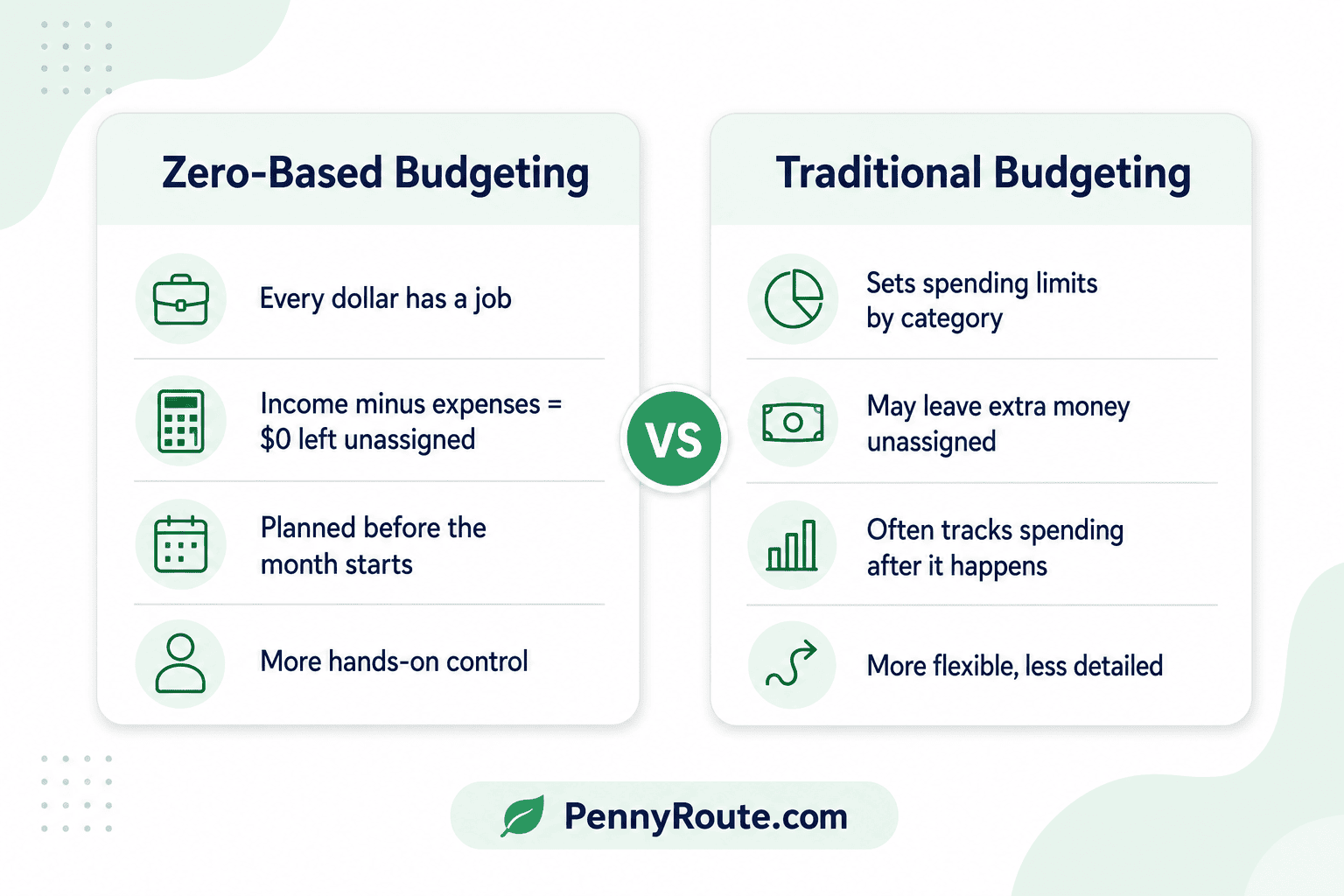

Zero-Based Budgeting vs. Traditional Budgeting

Zero-based budgeting and traditional budgeting both help you plan your money, but they work a little differently.

With a traditional budget, you may set general spending limits for categories like groceries, rent, savings, and entertainment. If money is left over, it might stay unplanned or get spent without much attention.

With zero-based budgeting, you assign every dollar before the month begins. That includes bills, savings, debt payments, spending money, and a small buffer.

| Budgeting Method | How It Works | Best For |

|---|---|---|

| Traditional budgeting | Sets spending limits for common categories | People who want a simpler monthly plan |

| Zero-based budgeting | Assigns all income to specific categories until nothing is left unplanned | People who want more control over where their money goes |

| 50/30/20 rule | Splits income into needs, wants, and savings/debt | People who prefer a broader budget structure |

Zero-based budgeting is usually more detailed than the 50/30/20 rule because it asks you to plan each category more closely. That extra detail can be helpful if your money often disappears into small purchases, subscriptions, or flexible spending.

The best method is the one you can actually follow. A simple budget you use every month is better than a detailed budget you abandon after two weeks.

Benefits of Zero-Based Budgeting

Zero-based budgeting can be helpful because it makes your money more intentional. Instead of letting income sit unplanned, you decide what each part of it needs to do.

You Plan Before You Spend

This method encourages you to make decisions before the month gets busy. Bills, groceries, savings, debt payments, and personal spending all get a place in the budget before money starts leaving your account.

That can make your spending feel less random and easier to adjust.

Savings Become Part of the Budget

With zero-based budgeting, savings are not treated as leftover money. You can assign money to an emergency fund, sinking fund, vacation fund, or other savings goal at the start of the month.

This is useful if you often plan to save but find that the money disappears by the end of the month.

Debt Payoff Feels More Intentional

If you are paying off debt, zero-based budgeting can help you plan minimum payments and extra payments more clearly.

Instead of hoping there is extra money later, you decide whether debt payoff gets a specific amount before the month begins.

It Shows Where Money Is Slipping Away

Because every dollar is assigned, it becomes easier to spot categories that are quietly growing.

Small subscriptions, extra takeout, impulse purchases, and flexible spending can hide inside a loose budget. A zero-based budget makes those areas easier to see, which gives you a better chance to adjust them.

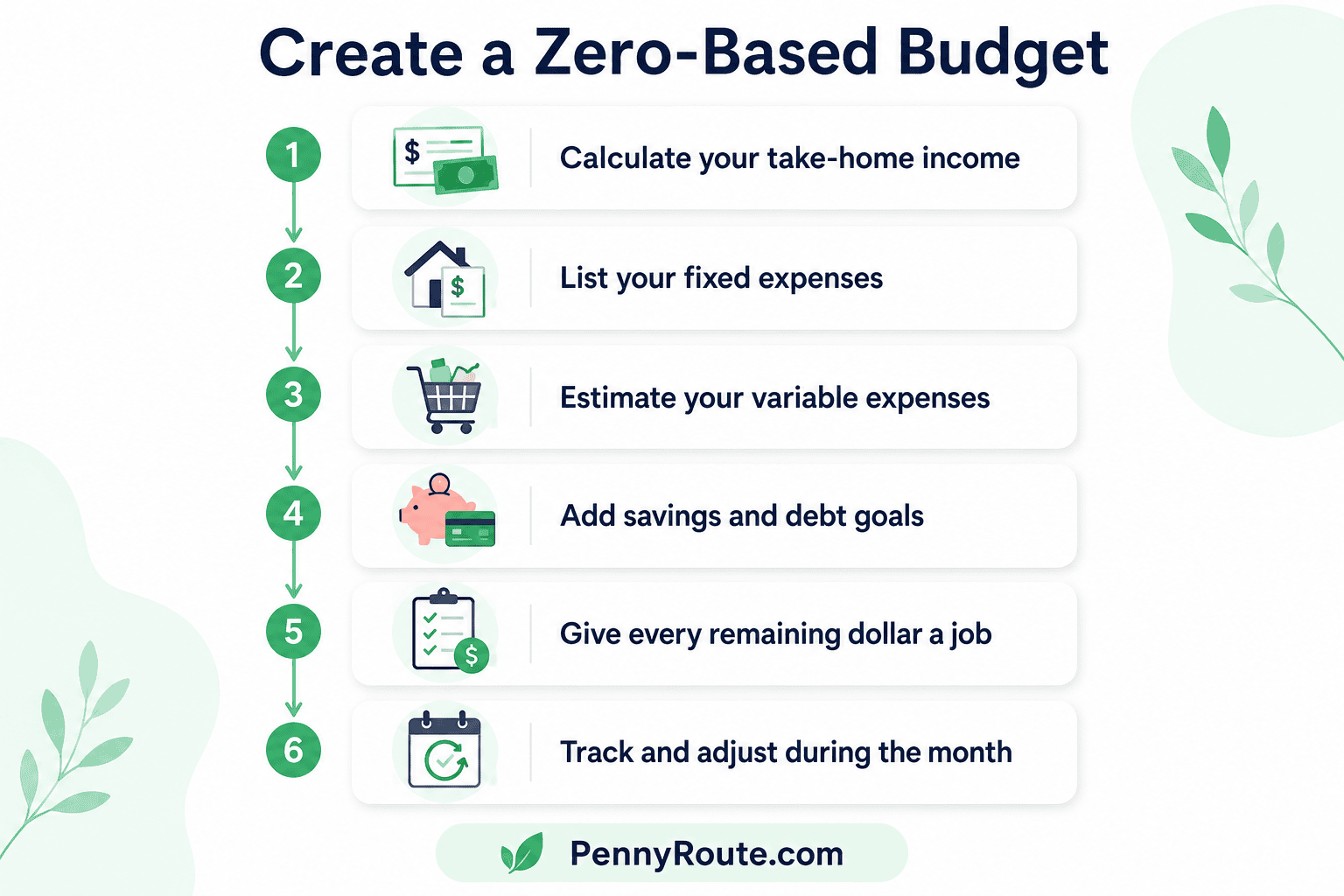

How to Create a Zero-Based Budget

A zero-based budget works best when you build it before the month begins. You do not need perfect numbers at first. You need a clear starting point and a willingness to adjust.

Start With Your Take-Home Income

Write down how much money you expect to receive for the month after taxes and deductions.

If your income changes from month to month, use a lower estimate instead of your best possible month. It is easier to adjust upward later than to build a budget around money that may not arrive.

List Your Fixed Expenses

Next, add the bills that are mostly the same each month.

This may include rent or mortgage, insurance, phone bill, internet, subscriptions, minimum debt payments, and other regular bills. These are usually the easiest numbers to enter because they do not change much.

Estimate Your Variable Expenses

Variable expenses are the categories that can change from month to month, such as groceries, gas, utilities, eating out, personal spending, and household supplies.

Use recent spending as a guide if you are not sure what to enter. Guessing too low may make the budget look good on paper, but it can make the month harder to manage.

Add Savings and Debt Goals

After your regular expenses, add money for savings and debt payoff.

This could include an emergency fund, sinking funds, extra debt payments, retirement contributions, or another savings goal. Treating savings as a category helps you plan it before the money gets absorbed by everyday spending.

Add a Small Buffer

A zero-based budget should not be so tight that one small change ruins the whole month.

If possible, add a small buffer for minor changes, such as a higher grocery bill, extra gas, or a small household need. Even $25 to $100 can make the budget easier to follow.

Give the Remaining Money a Job

Once the main categories are filled in, check whether any money is still unassigned.

If you have money left, decide where it should go before the month begins. You might add it to savings, debt payoff, a sinking fund, or a flexible spending category.

If the numbers go over your income, adjust before the month starts. That may mean reducing eating out, delaying a purchase, lowering a flexible category, or changing how much you save this month.

Check In During the Month

A zero-based budget is not something you create once and ignore.

Check your categories during the month, especially groceries, transportation, personal spending, and eating out. If one category runs high, move money from another category instead of letting the whole budget fall apart.

A quick weekly money check-in can help you catch overspending early instead of waiting until the month is almost over.

How to Use Zero-Based Budgeting With Each Paycheck

You do not have to wait for a full month of income to use zero-based budgeting. If you get paid weekly, biweekly, or twice a month, you can plan each paycheck instead.

Start with the paycheck you just received. Then list the bills, groceries, transportation, savings, debt payments, and other expenses that need to happen before your next paycheck arrives.

For example, if your next paycheck is two weeks away, your budget only needs to cover those two weeks plus any bills due before the next payday. If rent is due from this paycheck, that money gets assigned first. If groceries, gas, and a small savings transfer also need to happen, those get planned next.

This can make zero-based budgeting feel more realistic if your income does not arrive all at once. Instead of trying to plan a perfect month in one sitting, you are planning the money you actually have right now.

A simple budget calendar can help here because it shows which bills are due before each paycheck. That way, you are not assigning money to later expenses while forgetting something due this week.

Common Zero-Based Budgeting Mistakes

Zero-based budgeting is simple in theory, but a few mistakes can make it feel stricter or more frustrating than it needs to be.

Making the Budget Too Tight

A zero-based budget should not leave you feeling trapped.

If every category is squeezed too hard, one higher grocery bill or extra errand can throw off the whole month. Include realistic spending amounts and a small buffer so the budget has room for normal life.

Forgetting Irregular Expenses

Not every expense shows up monthly.

Annual subscriptions, car registration, school costs, gifts, home maintenance, and insurance renewals can sneak into the month if you do not plan for them. This is where sinking funds can help because they give irregular expenses a place before they arrive.

Guessing Instead of Tracking

Your first budget may include a few guesses, and that is normal. The problem starts when you keep guessing month after month without checking what you actually spend.

Look at recent bank statements, receipts, or a spending tracker to make your numbers more accurate. A budget based on real spending is easier to follow than one based on wishful thinking.

Forgetting to Adjust During the Month

A zero-based budget is not frozen once the month starts.

If groceries cost more than expected, you may need to move money from eating out, personal spending, or another flexible category. Adjusting the budget is better than ignoring the problem and hoping it works out.

Giving Up After One Bad Month

The first month may feel messy.

You might forget a bill, underestimate groceries, or realize your categories need work. That does not mean zero-based budgeting is wrong for you. It means your budget is giving you better information for next month.

Is Zero-Based Budgeting Right for You?

Zero-based budgeting can work well if you want a more detailed plan for your money. It gives each category a clear amount, which can make spending decisions easier during the month.

This method may be a good fit if:

- you want to know exactly where your income is going

- you often run out of money before the next paycheck

- you are working on savings or debt payoff goals

- you want more control over flexible spending

- you do not mind checking your budget during the month

Zero-based budgeting may not be the best fit if you hate detailed tracking or want a very simple budget. It can also feel like too much work if your income changes often and you do not want to adjust categories regularly.

If that sounds like you, a broader method like the 50/30/20 rule may feel easier to maintain. You can also start with a simpler budget first and move to zero-based budgeting later when you want more detail.

The best budgeting method is the one you can repeat. If zero-based budgeting helps you make clearer decisions without feeling overwhelmed, it may be worth trying for one month.

Best Tools for Zero-Based Budgeting

You can create a zero-based budget with a spreadsheet, budgeting app, notebook, or printable budget template. The best tool is the one you will actually update during the month.

Spreadsheet

A spreadsheet works well if you want full control over your categories and do not mind entering numbers yourself.

You can create columns for income, planned spending, actual spending, and the difference between the two. This is a good option if you like seeing all your numbers in one place.

Budgeting App

A budgeting app can make zero-based budgeting easier if you want reminders, automatic syncing, or cleaner tracking.

Apps like YNAB and EveryDollar are commonly used for zero-based budgeting because they are built around the idea of giving your money a job. Other finance apps may also help, but not all of them are designed specifically for this method.

Before choosing an app, check the pricing, features, and whether it connects with your bank in your country.

Notebook or Printable Budget

A notebook or printable budget can work if you prefer something simple and distraction-free.

This option is not fancy, but it can be effective if writing things down helps you slow down and pay attention to your spending. The main limit is that you need to update it regularly so your budget does not fall behind.

Simple Notes App

A notes app can also work for a very basic zero-based budget, especially when you are just starting.

You can list your income at the top, subtract bills and planned categories, and update the remaining amount as you assign money. It is not the most detailed option, but it is better than waiting for the perfect budgeting system.

The tool matters less than the habit. A basic budget you check often will do more for your money than a polished app you forget to open.

A Simple Zero-Based Budget Plan for Your First Month

You do not need to get zero-based budgeting perfect the first time. The first month is mostly about learning your real numbers and seeing where your money needs clearer direction.

Start with your take-home income. Add your fixed bills, estimate your flexible expenses, include savings or debt payments, and leave a small buffer if you can. Then assign the remaining money before the month begins.

During the month, check your budget once or twice a week. If groceries, gas, or another category runs higher than expected, move money from a lower-priority category instead of giving up on the whole plan.

After the month ends, look at what worked and what felt unrealistic. Your next zero-based budget should be easier because it will be based on real spending, not guesses.

A good budget is not the one that looks perfect on paper. It is the one you can adjust, repeat, and actually use.

FAQs About Zero-Based Budgeting

What is zero-based budgeting?

Zero-based budgeting is a method where you assign all your income to bills, savings, debt payments, spending categories, and a buffer until no money is left unplanned on paper.

How does zero-based budgeting work?

Zero-based budgeting works by starting with your take-home income, listing your expenses and goals, and assigning every dollar to a category before the month begins.

What is a zero-based budget example?

A zero-based budget example is earning $3,000 in a month and assigning the full $3,000 across rent, groceries, utilities, savings, debt payments, personal spending, and a small buffer.

What is the zero-based budgeting formula?

The simple zero-based budgeting formula is: income minus expenses, savings, and debt payments equals zero on paper.

Does zero-based budgeting mean you spend all your money?

No. Zero-based budgeting does not mean spending all your money. Savings, emergency fund contributions, sinking funds, debt payments, and buffer money all count as assigned categories.

What are the disadvantages of zero-based budgeting?

The main disadvantages of zero-based budgeting are that it takes more tracking, can feel too detailed, and may become frustrating if you do not include a buffer for normal changes.

Is zero-based budgeting good for beginners?

Zero-based budgeting can be good for beginners who want a clear plan for their money, but it works best when you start with simple categories and adjust as you learn your real spending.

Is zero-based budgeting better than the 50/30/20 rule?

Zero-based budgeting is not always better than the 50/30/20 rule. Zero-based budgeting gives more detail, while the 50/30/20 rule is simpler and easier to maintain.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.