A budget is much easier to use when it is not just one long list of expenses.

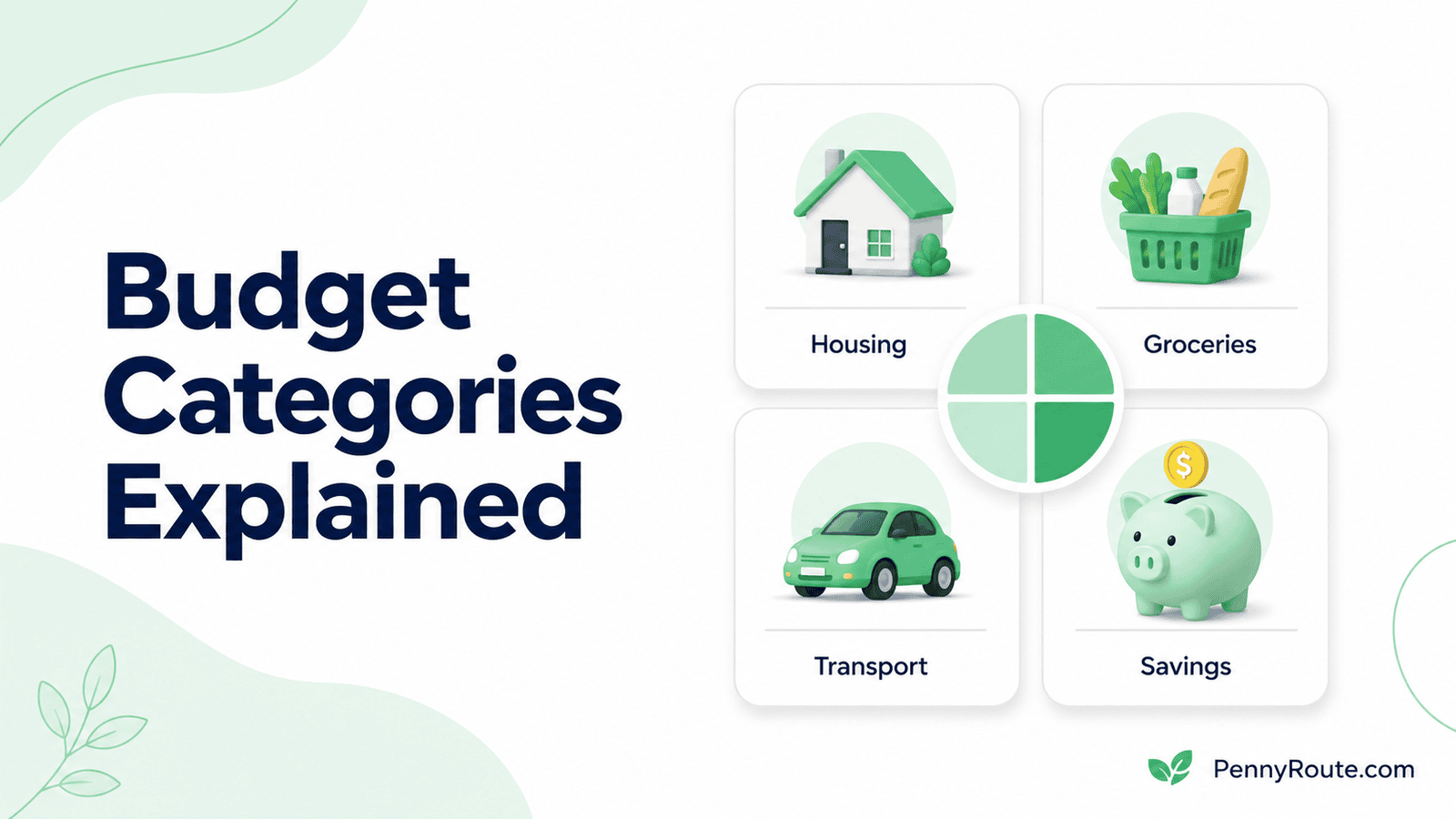

Budget categories give your money a simple structure. They separate your spending into clear groups like housing, food, transportation, savings, debt payments, and personal spending. That way, you can quickly see where your money is going instead of sorting through every purchase one by one.

This is especially helpful when you are new to budgeting. You do not have to guess whether you are overspending on groceries, subscriptions, or eating out. Your categories show you what is happening.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

What Are Budget Categories?

Budget categories are simple groups that organize your spending. They show where your money is meant to go, instead of leaving everything mixed together.

You can think of them as basic sections in your budget. Each category holds a type of expense, such as housing, food, or transportation. This makes it easier to see how your income is being used.

Here is a simple way to picture it. If your monthly income is $3,000, categories help you decide how much is set aside for rent, how much is used for groceries, and how much is available for other spending. Without categories, those decisions still happen, but they are harder to track and manage.

Budget categories do not need to be detailed or complex. A few clear groups are enough to get started. The goal is to create structure, not perfection.

When your money is organized into categories, your budget becomes easier to understand and adjust. You can quickly see what is working and what needs attention, without feeling overwhelmed.

Why Budget Categories Matter

When your spending is not organized, it is easy for money to feel unclear. You may know how much you earn, but not exactly where it goes. That gap is what makes budgeting confusing.

Budget categories bring structure to your money and make everyday decisions easier.

They help you:

- See where your money is actually going

- Make spending decisions without guessing

- Adjust one area without affecting your entire budget

- Notice patterns in your spending over time

When your money is grouped in a clear way, your budget becomes easier to follow and less stressful to maintain.

Essential Budget Categories (Needs)

Essential categories cover the expenses that keep your daily life running. These are the costs you usually need to pay each month before anything else.

They are often more fixed or less flexible in the short term, which is why they are planned first in any budget.

Common essential categories include:

- Housing, such as rent or mortgage

- Utilities, including electricity, water, and internet

- Groceries for basic food needs

- Transportation, such as fuel or public transit

- Insurance, like health, car, or home coverage

- Minimum debt payments

These expenses may not be exactly the same every month, but they tend to stay within a predictable range. Covering them first helps your budget stay stable.

It is also important to remember that essentials can look different for each person. What is necessary for one household may not be the same for another. The goal is not to follow a fixed list, but to understand what your own must-have expenses are.

Once these categories are planned, it becomes easier to decide how to use the rest of your income.

Flexible Budget Categories (Wants)

Flexible categories cover the expenses you can adjust when needed. These are the areas where you have more choice in how much you spend each month.

They include the parts of your budget that make life more comfortable or enjoyable, but are not required for basic needs.

Common flexible categories include:

- Dining out

- Entertainment

- Shopping

- Subscriptions

- Hobbies

These expenses are not a problem. They only become difficult when they grow without limits or take priority over essentials.

Having clear limits for these categories makes spending seem easier. You can enjoy them without worrying about bills or savings being affected later.

If your budget is tight, these are usually the first areas to adjust. Small changes here can create space for more important expenses or savings goals without restricting your entire budget.

Keeping flexible categories in your budget is important. A plan that allows for real life is much easier to follow over time.

Savings and Financial Goal Categories

Savings categories help you plan for the future while staying stable in the present. Instead of saving only what is left at the end of the month, you set aside money with a clear purpose.

This can include:

- Emergency savings for unexpected expenses

- Short term goals, such as travel or a large purchase

- Long term savings, like retirement

- Extra payments toward debt

You do not need large amounts to start. Setting aside a small amount each month builds consistency and reduces pressure over time.

Savings categories also make your budget more balanced. You are not only covering today’s expenses, but also preparing for what comes next. This helps avoid situations where unexpected costs turn into financial stress.

Keeping savings as a separate category makes it easier to track progress. Even small contributions add up and make your budget more stable over time.

Simple Budget Categories Example (Beginner-Friendly)

Seeing categories with real numbers can make things clearer. This example shows how a simple set of categories might look in a typical month.

Let’s say your monthly take-home income is $3,000.

Here is one way to organize that income using basic categories:

| Category | Monthly Amount |

|---|---|

| Housing | $1,200 |

| Utilities | $200 |

| Groceries | $350 |

| Transportation | $250 |

| Insurance | $150 |

| Flexible spending | $300 |

| Savings | $300 |

| Buffer for irregular costs | $250 |

| Total | $3,000 |

This example keeps categories simple and easy to manage. It covers essential expenses first, then allows room for flexible spending and savings.

A buffer category is included to handle expenses that do not happen every month, such as repairs, gifts, or unexpected costs. This helps protect the rest of the budget from small disruptions.

Your numbers may look different, and that is completely normal. The goal is not to match this example, but to understand how categories work together in a clear and organized way.

How Many Budget Categories Do You Really Need?

It is easy to think that more categories will give you better control. In reality, too many categories can make budgeting harder to manage.

A simple setup is usually more effective. Most beginners do well with around 6 to 12 categories. This is enough to cover essential expenses, flexible spending, and savings without feeling overwhelming.

When there are too many categories, a few things tend to happen:

- Tracking becomes time-consuming

- Small differences between categories create confusion

- The budget becomes harder to maintain

Instead of trying to organize every detail, focus on grouping similar expenses together. For example, you can combine small personal expenses into one category instead of splitting them into multiple sections.

You can always refine your categories later. As you get more comfortable, you may choose to split or adjust them based on your needs.

Common Budget Category Mistakes to Avoid

Creating Too Many Categories

It can be helpful to break everything into smaller sections, but too many categories make your budget harder to manage. Tracking becomes time-consuming, and small differences between categories can create confusion. Keeping categories broad and simple makes budgeting easier to follow.

Forgetting Irregular Expenses

Some costs do not show up every month, but they still affect your budget. Things like car repairs, gifts, or annual subscriptions can throw off your plan if they are not included. Adding a buffer or a small category for these expenses helps avoid surprises.

Setting Unrealistic Limits

It is common to set lower spending limits than what you actually need. This can make your budget restrictive and difficult to stick with. Starting with realistic numbers based on your current spending makes your budget more workable.

Not Updating Categories Over Time

Your spending can change as your situation changes. If your categories stay the same, your budget may stop reflecting real life. Reviewing and adjusting your categories regularly helps keep your budget relevant and useful.

If You Are Setting Budget Categories for the First Time

Start with a few simple categories and build from there. You do not need a perfect setup on your first attempt. A small number of clear categories is enough to understand how your money is being used.

Focus on covering your essential expenses first. Then add one or two flexible categories and a savings category. This creates a balanced structure without making things complicated.

As you use your budget, you will notice what feels easy and what needs adjusting. Some categories may need more room. Others may not be necessary. These changes are part of the process.

Keeping your setup simple makes it easier to stay consistent. Once you are comfortable, you can refine your categories based on your spending habits.

If you want a step-by-step way to turn these categories into a full plan, you can read our guide on how to make a budget for beginners and build your first monthly budget.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, expense tracking, cashback apps, side income, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.