Income that changes from month to month can make budgeting harder to plan.

One month may be comfortable, then the next month gets tight because a client pays late, shifts get cut, sales slow down, or gig work dries up. The bills still arrive on schedule, even when your income does not.

Budgeting with irregular income means building a plan that can handle both good months and slow months. Instead of basing your budget on your best paycheck, you start with the basics, protect your must-pay expenses, and decide what extra money should do before it disappears.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

Quick Overview: Budgeting With Irregular Income

- Start with a baseline income instead of your best month, so your budget is not built on money that may not arrive.

- Cover must-pay expenses first, including housing, utilities, groceries, transport, insurance, and minimum debt payments.

- Use separate buckets for bills, taxes, savings, spending, and slow months so each payment has a clear purpose.

- Save extra from high-income months before increasing everyday spending.

- A one-month income buffer can make uneven pay easier to manage because last month’s income helps cover this month’s bills.

What Is Irregular Income?

Irregular income means your pay changes from month to month instead of arriving as the same amount on a fixed schedule.

This can happen if you are a freelancer, gig worker, contractor, seasonal worker, commission-based employee, tipped worker, self-employed business owner, or someone whose hours change often.

The challenge is not only that your income changes. It is that your bills usually do not. Rent, utilities, insurance, groceries, debt payments, and other basic costs still need a plan, even when your income is higher one month and lower the next.

That is why budgeting with irregular income works best when you plan from a careful baseline instead of your highest month. It gives your budget a safer starting point and helps you avoid spending like every month will be a good month.

Why Budgeting Feels Harder With Irregular Income

Budgeting is harder with irregular income because your expenses often follow a schedule, but your income does not.

A regular monthly budget may assume the same paycheck arrives every week or every two weeks. With uneven pay, that can create problems. You may have enough money one month, then struggle the next because a payment is delayed, a project ends, or work slows down.

This is why budgeting from your best month can be risky. If you build your normal spending around a high-income month, a slower month can quickly create a gap.

You do not need to predict every payment perfectly. You need a budget that protects the basics first, gives extra income a clear purpose, and keeps slower months from turning into a panic.

Start With Your Baseline Income

When your income changes, your budget needs a safer starting point than your best month.

Your baseline income is the amount you can usually count on during a normal or slower month. It helps you build a budget around money that is more likely to arrive, instead of planning around a high-income month that may not repeat.

Use Your Lowest Realistic Monthly Income

If your income changes a lot, start with your lowest realistic monthly income from the past several months.

For example, if your income looked like this:

| Month | Income |

|---|---|

| January | $3,200 |

| February | $2,400 |

| March | $4,100 |

| April | $2,700 |

| May | $3,600 |

| June | $2,500 |

You might use $2,400 or $2,500 as your baseline instead of $3,000 or $4,100. That gives your budget a safer number to work with.

Use Your Average Income Only If It Is Stable Enough

Average income can work if your income changes slightly but not dramatically.

For example, if most months stay between $2,800 and $3,200, using an average may be reasonable. But if one month is $5,000 and the next is $1,800, the average can make your budget look more comfortable than it really is.

What If You Are New and Do Not Have 12 Months of Income?

If you are new to freelancing, gig work, commissions, or self-employment, you may not have enough income history yet.

In that case, start with your must-pay expenses instead. List the minimum amount you need for housing, utilities, groceries, transportation, insurance, debt payments, and basic needs. That number becomes your first safety target while you learn what your income pattern looks like.

Build a Bare-Minimum Budget First

A bare-minimum budget shows the lowest amount you need to cover your essentials during a slow month.

This is not your ideal budget. It is your safety version. It helps you see which expenses must be covered first when income is lower than usual.

Start with the basics:

| Category | Example |

|---|---|

| Housing | Rent or mortgage |

| Utilities | Electricity, water, gas, basic phone, internet |

| Food | Groceries and basic household needs |

| Transportation | Gas, public transit, insurance, essential car costs |

| Debt payments | Minimum payments only |

| Insurance | Health, auto, renters, homeowners, or other required coverage |

| Basic family needs | Childcare, school needs, pet essentials, or medical basics |

Once you know this number, you can compare it with your baseline income. If your bare-minimum budget is $2,300 and your baseline income is $2,500, you have a small cushion. If your bare-minimum budget is higher than your baseline income, you know the budget needs adjustment before a slow month arrives.

This section should stay focused on essentials. Your full budget can include eating out, entertainment, subscriptions, hobbies, and extra savings, but your bare-minimum budget helps you protect the bills that matter most first.

Separate Your Money Into Simple Buckets

When your income is irregular, one payment may need to cover several different jobs. A $2,000 client payment is not all spending money if part of it needs to cover taxes, rent, groceries, slow months, and savings.

Simple money buckets can help you separate each purpose before the money disappears into everyday spending.

| Money Bucket | What It Covers |

|---|---|

| Bills | Rent, utilities, insurance, debt payments, and other must-pay expenses |

| Taxes | Money set aside for taxes if they are not withheld automatically |

| Savings | Emergency fund, sinking funds, or future goals |

| Slow months | Money saved from better months to cover lower-income months |

| Spending | Groceries, gas, personal spending, eating out, and flexible categories |

You do not need a separate bank account for every bucket. You can use different savings accounts, subaccounts, budgeting app categories, a spreadsheet, or even a simple notes page.

The main point is to know how much of each payment is actually available to spend. Without that separation, a good income month can look better than it really is.

Save Extra From High-Income Months

High-income months can make your budget easier, but only if the extra money gets a job before regular spending grows around it.

When you earn more than your baseline income, decide where the extra money should go first. This can help you prepare for slow months instead of treating every good month like a permanent raise.

Here is a simple way to split extra income:

| Extra Income Use | Why It Helps |

|---|---|

| Taxes | Keeps tax money separate before it gets spent |

| Slow-month buffer | Helps cover bills when income drops |

| Emergency fund | Protects you from urgent, unexpected expenses |

| Sinking funds | Prepares for planned costs like annual bills or car repairs |

| Debt payoff | Helps reduce balances when you have room |

| Flexible spending | Lets you enjoy some extra money without using all of it |

You do not have to save every extra dollar. A balanced plan can still include some fun money. The important part is deciding that amount on purpose, instead of letting a strong month disappear without improving your next one.

Create a One-Month Income Buffer

A one-month income buffer means using money from last month to pay this month’s bills.

This can be especially helpful when your income arrives at different times or in uneven amounts. Instead of depending on this week’s payment to cover this week’s bills, you give your money more breathing room.

For example, let’s say your essential monthly expenses are $2,500. A one-month buffer means you eventually keep $2,500 set aside so the current month is already covered before new income arrives.

You do not have to build the full buffer quickly. Start with a smaller target, such as one week of expenses. Then build toward two weeks, then a full month.

| Buffer Stage | What It Means |

|---|---|

| 1 week of expenses | You have a small cushion before the next payment arrives |

| 2 weeks of expenses | You are less dependent on one paycheck or client payment |

| 1 month of expenses | This month’s basics can be covered with money already saved |

An income buffer is different from an emergency fund. Your emergency fund is for urgent, unexpected problems. Your income buffer is for smoothing out uneven cash flow, late payments, and slow months.

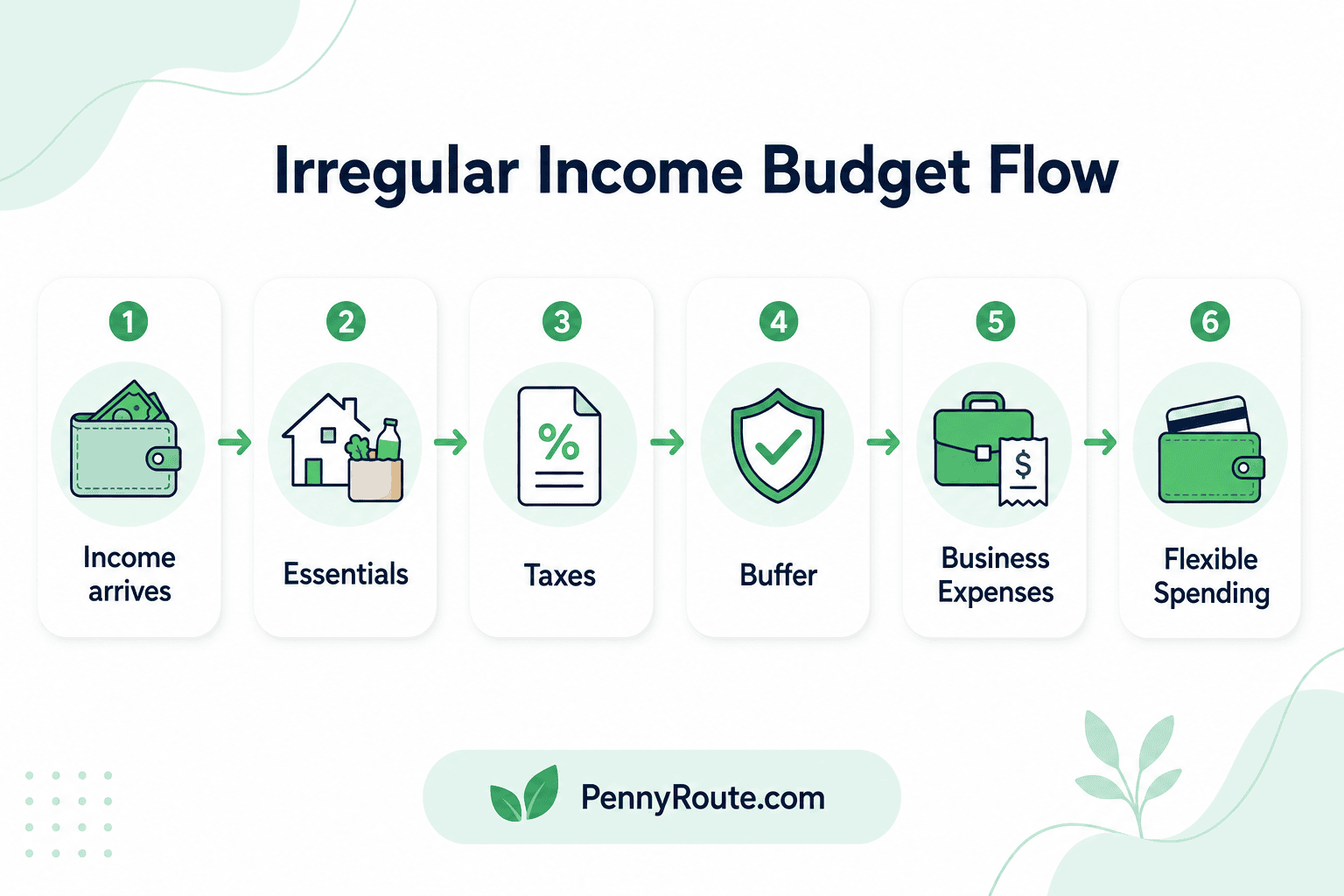

Set Aside Money for Taxes Before You Spend

If taxes are not automatically taken out of your income, set aside tax money before you treat a payment as spendable.

This matters for freelancers, gig workers, contractors, and self-employed workers because a large payment can look like more usable money than it really is. Part of that payment may need to go toward income tax, self-employment tax, or other required payments depending on where you live and how you earn.

A simple tax bucket can help.

When a payment arrives, move a percentage into a separate savings account or category before you use the rest for bills, spending, or savings goals.

The right percentage depends on your income, location, business expenses, and tax situation. If you are unsure, check official tax guidance or speak with a qualified tax professional. The important habit is separating tax money early so it does not get mixed into everyday spending.

For US readers, the IRS Self-Employed Individuals Tax Center explains federal tax basics for self-employed workers, including filing returns and estimated tax payments.

This one step can prevent a good income month from turning into stress later when a tax bill arrives.

Pay Yourself a Consistent Amount

When your income changes, paying yourself a steady amount can make your personal budget easier to manage.

Instead of spending directly from every payment that comes in, you can send income into one main account first. From there, transfer a set amount to yourself each week, every two weeks, or once a month.

For example, if your income changes between $2,500 and $4,000 per month, you might choose to pay yourself $2,500 for regular bills and spending. In higher-income months, the extra money can stay in your buffer, tax bucket, emergency fund, or savings.

| Monthly Income | Amount You Pay Yourself | What Happens to the Rest |

|---|---|---|

| $2,500 | $2,500 | Nothing extra this month |

| $3,200 | $2,500 | $700 goes to taxes, buffer, savings, or debt |

| $4,000 | $2,500 | $1,500 goes to taxes, buffer, savings, or debt |

This system can help turn uneven income into a more predictable routine. It also reduces the chance of spending more in good months and struggling when the next month is slower.

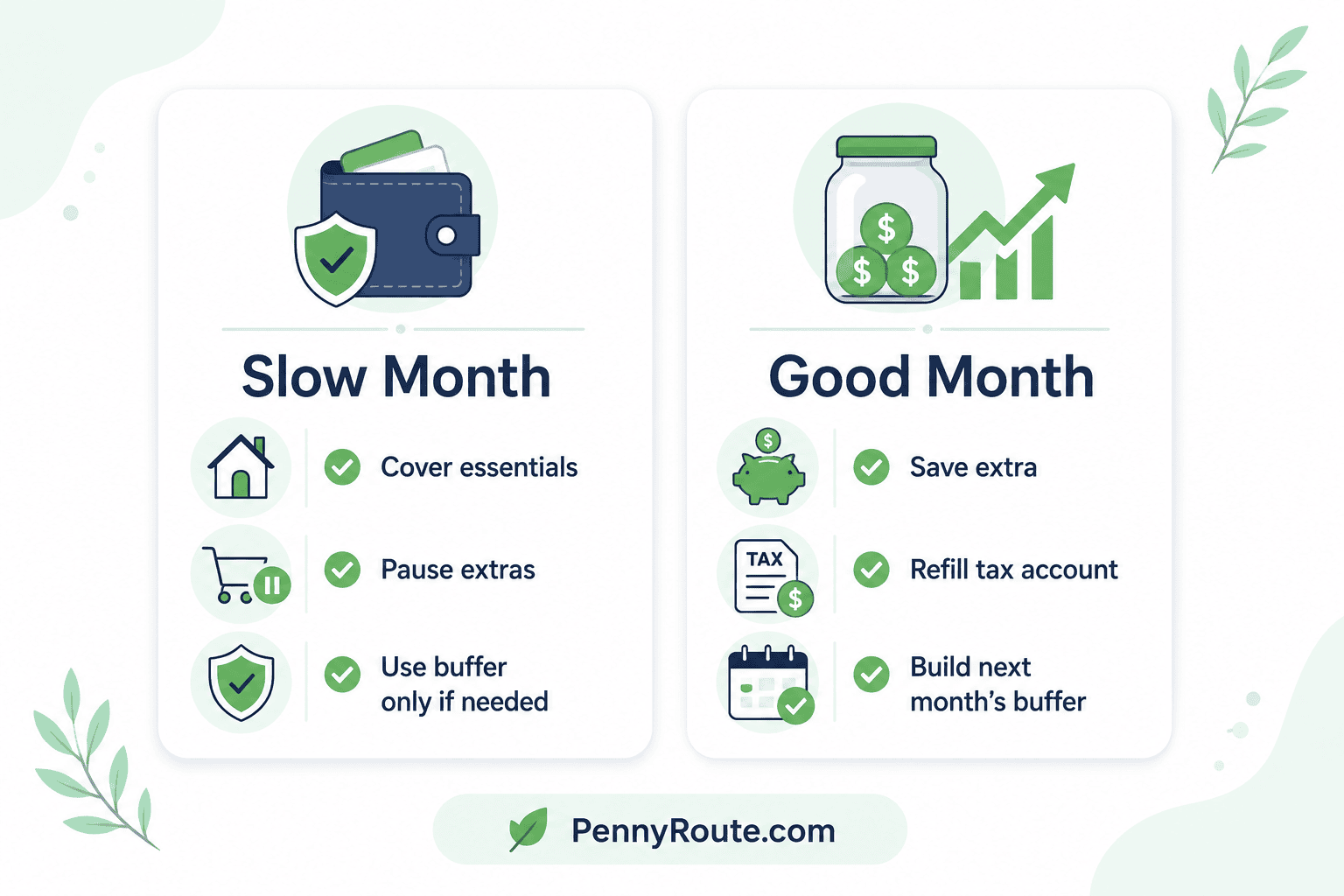

Use a Slow-Month and Good-Month Plan

Irregular income is easier to manage when you know what changes in a slow month and what happens in a good month.

A slow month plan helps you protect the essentials. A good month plan helps you use extra income before it quietly turns into extra spending.

| Month Type | What to Do First |

|---|---|

| Slow month | Cover housing, utilities, groceries, transport, insurance, and minimum debt payments |

| Normal month | Follow your baseline budget and keep regular savings habits going |

| Good month | Fill tax buckets, rebuild your buffer, add to savings, or pay down debt |

| Very strong month | Save for future slow months before increasing lifestyle spending |

In a slow month, reduce flexible categories first. That may mean less eating out, fewer extras, pausing non-essential subscriptions, or delaying a purchase.

In a good month, avoid treating the full increase as spending money. You can still enjoy part of it, but send money toward your buffer, emergency fund, sinking funds, or future bills before the month gets away from you.

This simple plan helps your budget respond to real income changes instead of starting over every time your pay goes up or down.

Best Budgeting Methods for Irregular Income

The best budgeting method for irregular income is the one that gives your money structure without making you rebuild your whole budget every week.

You do not need a complicated system. You need a method that helps you cover essentials first, manage slow months, and decide what to do when extra income comes in.

Zero-Based Budgeting

Zero-based budgeting can work well with irregular income because you assign money after it arrives.

Instead of guessing the perfect monthly income, you start with the money you actually have and give it a job. Bills, groceries, savings, taxes, debt payments, and spending categories all get planned before the money is used.

This method can be helpful if you want more control over each payment, but it may require more checking and adjusting during the month.

Bare-Minimum Budget

A bare-minimum budget is useful for slow months because it shows the lowest amount you need to keep your household running.

This method helps you protect essentials first, such as housing, utilities, groceries, transportation, insurance, and minimum debt payments. When income is low, this budget becomes your safety plan.

Percentage-Based Budget

A percentage-based budget can work when your income changes often because the amounts adjust with each payment.

For example, you might send a percentage of every payment to taxes, savings, bills, and spending. This can be useful for freelancers or gig workers who want a simple rule for each deposit.

50/30/20 Budget

The 50/30/20 budget can still work with irregular income, but it may need flexibility.

In a lower-income month, needs may take more than 50% of your income. In a higher-income month, you may be able to send more toward savings, debt payoff, or your income buffer. Think of the percentages as a guide, not a rule you have to follow perfectly.

If manual tracking is difficult to keep up with, app-based budgeting may help you organize categories and check balances more often.

Example: A Freelancer Budget With Irregular Income

Here is a simple example of how irregular income budgeting can work in real life.

Let’s say your income changes each month, but your bare-minimum budget is $2,400. That means you need at least $2,400 to cover housing, utilities, groceries, transportation, insurance, minimum debt payments, and other essentials.

| Month | Income | What Happens |

|---|---|---|

| January | $3,200 | $2,400 covers essentials, and $800 goes to taxes, savings, or buffer |

| February | $2,500 | $2,400 covers essentials, and $100 stays flexible |

| March | $4,000 | $2,400 covers essentials, and $1,600 goes to taxes, buffer, savings, or debt |

| April | $2,100 | Essentials are short by $300, so the buffer helps cover the gap |

This is why high-income months matter so much. They are not just “extra” months. They help protect the months when income drops.

If you earn more than your baseline, decide where the extra money should go before regular spending grows. If you earn less than your baseline, use your slow-month plan and cover essentials first.

A Simple Irregular Income Budget Plan to Start This Month

You do not need to organize your entire financial life at once. Start by creating a budget that protects your essentials first, then build more structure as your income pattern becomes clearer.

| Step | What to Do |

|---|---|

| 1 | List your must-pay expenses, such as housing, utilities, groceries, transport, insurance, and minimum debt payments. |

| 2 | Choose a baseline income using your lowest realistic month or your must-pay expense number. |

| 3 | Separate each payment into simple buckets for bills, taxes, savings, slow months, and spending. |

| 4 | Use high-income months to build your buffer before increasing flexible spending. |

| 5 | Set aside tax money first if taxes are not withheld automatically. |

| 6 | Review your budget after each payday or at least once a week. |

| 7 | Adjust your baseline as you learn your real income and expense patterns. |

The first month is mostly about getting a clearer picture. Once you know your baseline income, bare-minimum expenses, and slow-month plan, irregular income becomes easier to manage without guessing every time money arrives.

FAQs About Budgeting With Irregular Income

How do you budget with irregular income?

Budget with irregular income by using a realistic baseline income, covering essential expenses first, separating money into buckets, and saving extra from high-income months to help cover slower months.

What is the best budgeting method for irregular income?

The best budgeting method for irregular income is usually one that protects essentials first, such as a bare-minimum budget, zero-based budget, or percentage-based budget. The right choice depends on how much detail you want to track.

Should I budget with my lowest income or average income?

If your income changes a lot, using your lowest realistic monthly income is usually safer. If your income only changes slightly, an average income may work, but it should not depend on unusually high months.

How do I budget when my income changes every month?

Start with your must-pay expenses, then assign each payment to bills, taxes, savings, slow-month money, and spending. When you earn more, save part of the extra before increasing flexible spending.

How do I budget if I get paid different amounts each month?

If you get paid different amounts each month, build your budget around essential expenses first and use high-income months to prepare for lower-income months. A separate buffer can help smooth out the gaps.

How much should I save with irregular income?

Start by building a small emergency fund, then work toward a one-month income buffer if possible. If taxes are not withheld, set aside tax money from each payment before treating the rest as spendable.

How do freelancers budget for taxes?

Freelancers can budget for taxes by moving a percentage of each payment into a separate tax bucket or savings account before spending the rest. The right amount depends on income, location, expenses, and tax rules.

What is a one-month income buffer?

A one-month income buffer means using last month’s income to pay this month’s bills. It can make irregular income easier to manage because your current bills are not fully dependent on the next payment arriving on time.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.