Not everyone wants to track twenty categories, update a spreadsheet every weekend, or label every coffee purchase like it is evidence in a financial investigation.

That is where the no-budget budget can help.

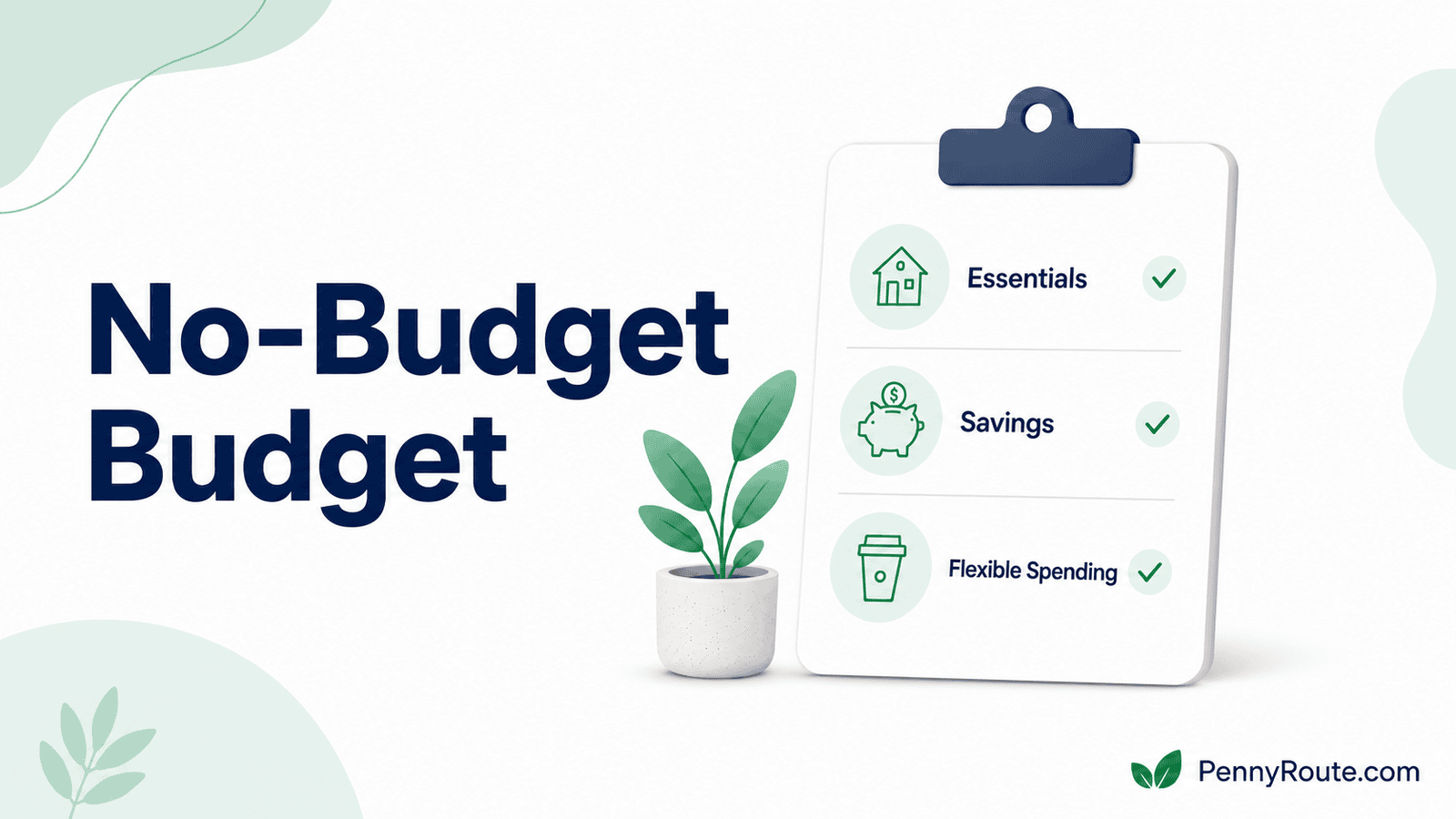

A no-budget budget is not about ignoring your money. It is a simple system where you cover the important things first, then manage one flexible spending number instead of tracking every small category.

You still plan for bills. You still save. You still keep an eye on spending.

You just skip the part where budgeting turns into a second job.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

What Is a No-Budget Budget?

A no-budget budget is a simple money system where you cover fixed bills, set aside money for savings or debt goals, and use one flexible spending amount for the rest.

So no, it does not mean “spend freely and hope your bank account survives.”

It means you create a basic structure without tracking every purchase in detailed categories.

Instead of budgeting separately for groceries, eating out, shopping, entertainment, household items, and small extras, you may group them into one flexible spending number.

For example, after your bills and savings are covered, you might have $700 left for flexible spending. That $700 becomes the number you watch.

This method works best when you want a lighter way to manage money, but still want your bills, savings, and everyday spending to have clear limits.

How the No-Budget Budget Works

The no-budget budget works by separating your money into three simple parts:

- Fixed bills and required payments

- Savings or debt goals

- Flexible spending money

The basic formula looks like this:

Take-home pay − fixed bills − savings/debt goals = flexible spending money

For example:

| Money Step | Amount |

|---|---|

| Monthly take-home pay | $3,200 |

| Fixed bills and required payments | −$1,900 |

| Savings or extra debt payments | −$500 |

| Flexible spending money | $800 |

That $800 is what you use for everyday spending, such as groceries, eating out, household items, personal spending, and small extras.

This is the part you watch. Not twenty categories. Not every tiny purchase. Just one clear number that tells you how much room you have after the important money is handled.

What Counts as Fixed Bills and Flexible Spending?

The no-budget budget works best when you separate predictable expenses from everyday spending.

Fixed bills are the expenses you need to pay or set aside for before you start using your flexible spending money.

Common fixed bills and required payments include:

- Rent or mortgage

- Utilities

- Insurance

- Minimum debt payments

- Phone and internet

- Childcare

- Basic transportation costs

- Subscriptions you truly plan to keep

- Automatic savings or extra debt payments

Flexible spending is the money you use for everyday choices and variable expenses.

This can include:

- Groceries

- Eating out

- Coffee and snacks

- Shopping

- Entertainment

- Personal spending

- Household items

- Small gifts

- Random extras

Groceries are technically a need, but in a no-budget budget, they may still sit inside flexible spending if you want one simple number to manage.

If one category keeps causing problems, you can separate it later. For example, you might keep groceries outside your flexible spending number and use the rest for eating out, shopping, and fun money.

No-Budget Budget Example

Let’s put the method into a simple monthly example.

Say your monthly take-home pay is $3,200. Before you think about flexible spending, you cover your fixed bills and savings goals first.

| Money Item | Amount |

|---|---|

| Monthly take-home pay | $3,200 |

| Rent | −$1,200 |

| Utilities | −$180 |

| Insurance | −$150 |

| Phone and internet | −$120 |

| Minimum debt payments | −$250 |

| Automatic savings | −$300 |

| Extra debt payment | −$200 |

| Flexible spending left | $800 |

In this example, the $800 is the number you manage for the rest of the month.

That money could cover groceries, eating out, shopping, entertainment, household items, and small extras. You are not tracking each of those categories separately. You are simply making sure your flexible spending stays within the amount left after bills and goals are handled.

This keeps the system simple while still giving your money a clear plan.

How to Start a No-Budget Budget

Start by setting up the big pieces first. The no-budget budget only works if your bills, savings, and flexible spending are clearly separated.

Here’s a simple way to begin:

- Find your monthly take-home pay.

Use the money that actually reaches your bank account after taxes and deductions. - List your fixed bills and required payments.

Include rent, utilities, insurance, minimum debt payments, childcare, phone, internet, and any other must-pay expenses. - Choose one savings or debt goal.

Start with one priority, such as an emergency fund, sinking fund, or extra debt payment. - Automate what you can.

Set up automatic bill payments, savings transfers, or debt payments so the important money moves happen first. - Find your flexible spending number.

Subtract fixed bills and savings or debt goals from your take-home pay. The amount left is what you manage for everyday spending. - Keep flexible spending separate if possible.

You can use a separate checking account, prepaid card, or budgeting app category so the number is easier to track. - Check in once or twice a week.

You do not need a full budget meeting. Just look at how much flexible spending money is left and adjust before it gets too low.

Use a Weekly Spending Number

A monthly flexible spending number can still disappear too quickly if you are not careful.

For example, $800 for the month may sound like plenty. But if you spend $450 in the first week, the rest of the month gets tight fast.

A simple fix is to turn your monthly flexible spending into a weekly number.

| Flexible Spending | Weekly Guide |

|---|---|

| $800 per month | $200 per week |

| $600 per month | $150 per week |

| $400 per month | $100 per week |

This gives you a smaller number to watch without creating a detailed category budget.

If your weekly number is $200, you do not need to track every tiny purchase by category. You just need to know whether your everyday spending is staying near that weekly limit.

This is where the no-budget budget becomes easier to use in real life. It gives you a guardrail without turning your money into a homework assignment.

When the No-Budget Budget Works Well

The no-budget budget works best when you want a simple system and your money is already somewhat stable.

It may be a good fit if you:

- Hate detailed tracking: You do not want to sort every purchase into a category.

- Have fairly steady income: Your monthly income is predictable enough to plan around.

- Pay bills on time already: The main problem is flexible spending, not missed bills.

- Want more automation: Bills, savings, and debt payments can happen in the background.

- Need one clear spending limit: You prefer watching one flexible number instead of several categories.

- Get overwhelmed by traditional budgets: A lighter system is easier for you to keep using.

This method is especially helpful if your main issue is not “I have no idea where anything goes,” but more like, “I need a simple way to avoid spending too much after the important stuff is covered.”

When It May Not Be Enough

The no-budget budget is simple, but it may be too loose if your money needs more structure.

It may not be the best fit if you:

- Regularly overdraft: You may need a more detailed plan until your cash flow feels steadier.

- Use credit cards to cover monthly gaps: A single flexible spending number may not be enough to stop the cycle.

- Have irregular income: If your income changes often, you may need a budget built around your lower-income months.

- Do not know where your money is going: A short spending review may help before switching to a lighter system.

- Overspend in one category often: If groceries, takeout, or shopping keeps causing problems, envelope budgeting may work better.

- Need a detailed debt payoff plan: Zero-based budgeting can give debt payments a clearer place in the monthly plan.

This does not mean the no-budget budget is bad. It just means it works best when your basics are already somewhat steady and you need a simpler way to manage the money left over.

No-Budget Budget vs. Other Budgeting Methods

The no-budget budget is one of the simplest budgeting methods, but it is not the only option. It helps to compare it with other methods so you can see where it fits.

| Budgeting Method | How It Works | Best For |

|---|---|---|

| No-budget budget | Covers bills and savings first, then manages one flexible spending number | People who hate detailed tracking |

| 50/30/20 budget | Splits income into needs, wants, and savings/debt payoff | Beginners who want a simple percentage guide |

| Zero-based budgeting | Gives every dollar a specific job before the month begins | People who want detailed control |

| Envelope budgeting | Sets spending limits for specific categories | People who overspend in certain areas |

The no-budget budget is less detailed than zero-based budgeting and less structured than the 50/30/20 method. That can be a good thing if detailed budgets make you quit.

But if one spending category keeps causing trouble, envelope budgeting may help more. If your whole budget feels unclear, zero-based budgeting may be a better starting point.

The best method is the one that solves your current problem without making the system harder than you will actually use.

Common Mistakes to Avoid

The no-budget budget is simple, but it still needs a few guardrails.

Here are the biggest mistakes to avoid:

- Treating “no-budget” like no plan:

Bills, savings, debt payments, and flexible spending still need clear limits. - Forgetting irregular expenses:

Car repairs, annual subscriptions, gifts, school costs, and insurance renewals can throw off your flexible spending if you do not plan for them. - Keeping everything in one account:

If bill money, savings, and spending money are mixed together, it is easier to spend money that already had a job. - Making the flexible number too high:

If you leave too much for flexible spending and too little for savings or debt goals, the system may feel easy but not very helpful. - Never checking in:

You do not need to track every purchase, but you still need to check your flexible spending once or twice a week. - Using credit cards to stretch the number:

If the flexible spending money runs out, credit cards can make it look like the system is working when it is really creating next month’s problem.

Keep Your Budget Simple, Not Invisible

The no-budget budget works because it removes the parts of budgeting that make many people quit.

You are not tracking every small purchase or sorting your life into twenty categories. But simple does not mean invisible.

Your bills still need a plan, your savings or debt goals still need a place, and your flexible spending still needs a number you can check.

If traditional budgeting has never worked for you, start here: cover the important money first, use one flexible spending number, and check in lightly before things get too close to zero.

FAQs About the No-Budget Budget

What is a no-budget budget?

A no-budget budget is where you cover fixed bills, set aside money for savings or debt goals, and use one flexible spending number for everyday expenses. It is called “no-budget” because you are not tracking every small category, but you still have a basic plan.

Does a no-budget budget mean I do not track anything?

No. You still need to track the most important number: your flexible spending. You do not have to sort every purchase into detailed categories, but you should check your remaining spending money once or twice a week.

Who is the no-budget budget best for?

The no-budget budget works best for people who dislike detailed budgeting but still want some structure. It can be a good fit if your income is fairly steady, your bills are mostly under control, and you want a simpler way to manage everyday spending.

What should I do if my flexible spending runs out?

If your flexible spending runs out, pause non-essential spending until the next budget period if possible. If this happens often, your flexible spending number may be too low, your fixed bills may be too high, or you may need a more detailed method like envelope budgeting.

Can I use a no-budget budget with irregular income?

You can, but it may need extra caution. If your income changes often, build your no-budget budget around a lower-income month instead of a good month. You may also need a bigger buffer so slow months do not throw off your bills.

Is the no-budget budget better than zero-based budgeting?

It depends on what you need. The no-budget budget is simpler and requires less tracking. Zero-based budgeting gives you more control because every dollar gets assigned a job. If your money feels messy or tight, zero-based budgeting may work better.

How often should I check my no-budget budget?

Check it once or twice a week. That is usually enough to see whether your flexible spending is on track without turning the system into a full, detailed budget.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.