When money gets tight, a normal budget may not be enough. Maybe your income dropped, bills piled up, an emergency hit, or you need to free up cash quickly without guessing what to cut.

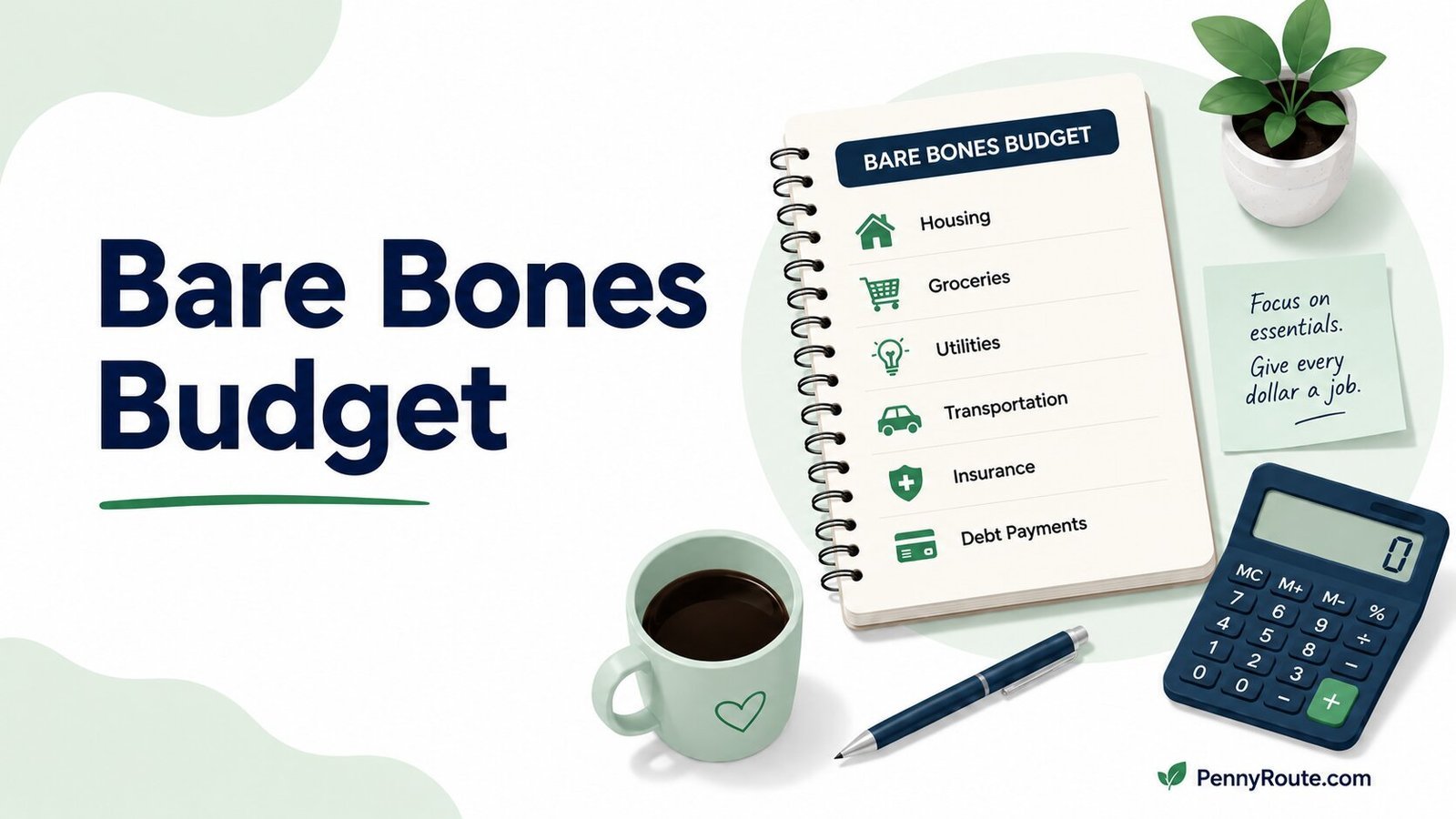

A bare bones budget helps you focus on the essentials first. Instead of trying to manage every normal spending category, you temporarily protect the basics like housing, food, utilities, transportation, insurance, and minimum debt payments.

This is not meant to be your forever budget. It is a short-term plan for getting through a tighter season with more clarity and less panic.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

Quick Overview: Bare Bones Budget

- A bare bones budget is a temporary budget that covers only your most important expenses.

- It can help during job loss, reduced hours, surprise bills, debt pressure, or any season when money is unusually tight.

- The main categories usually include housing, utilities, groceries, transportation, insurance, minimum debt payments, medical needs, and essential childcare.

- Non-essential spending like dining out, subscriptions, shopping, upgrades, and entertainment is paused or reduced for a short time.

- A bare bones budget helps you protect your essentials, free up cash, and return to a more balanced budget when things stabilize.

What Is a Bare Bones Budget?

A bare bones budget is a temporary budget that covers only your essential expenses. It is the version of your budget you use when money is tight and you need to protect the basics first.

This usually includes things like housing, groceries, utilities, transportation, insurance, minimum debt payments, and necessary medical costs. These are the expenses that help you keep your home, stay fed, get to work, protect your health, and avoid late fees or bigger money problems.

A bare bones budget is different from a regular monthly budget. A regular budget may include savings goals, fun money, dining out, subscriptions, clothing, hobbies, and other flexible spending. A bare bones budget strips the plan down for a short time so you can focus on what matters most right now.

That does not mean every non-essential expense is “bad.” It only means some spending may need to pause until your income, bills, or savings feel more stable.

When a Bare Bones Budget Makes Sense

A bare bones budget makes sense when your normal budget no longer fits your current situation. It is most useful when you need to free up cash quickly, cover the basics first, or get through a short-term financial squeeze.

You might use a bare bones budget if:

- Your income dropped because of job loss, reduced hours, or slower work.

- You are behind on bills and need a catch-up plan.

- A medical bill, car repair, or emergency expense changed your month.

- You are trying to stop relying on credit cards for basic expenses.

- You need to rebuild your emergency fund after using it.

- You want to make faster progress on urgent debt for a limited time.

This type of budget works best when it has a clear purpose. For example, you may use it for 30 days while catching up on bills, or for a few months while building a small savings cushion.

It should not feel like punishment. It is simply a short-term reset that helps you decide what needs your money first.

What to Include in a Bare Bones Budget

A bare bones budget should cover the expenses you truly need to keep your household stable. These are the costs that protect your home, health, work, basic food, and financial obligations.

Your exact list may look different from someone else’s. A parent with daycare costs, a renter with public transit, and a homeowner with required insurance may all have different essentials.

Here are the main budget categories to consider.

Housing

This includes rent or mortgage payments. If you are trying to avoid falling behind, housing usually needs to stay near the top of the list.

You may also need to include renter’s insurance, homeowners insurance, property taxes, or HOA fees if they apply to your situation.

Basic Utilities

Keep essential utilities in the budget, such as electricity, water, gas, trash service, and basic phone service.

Internet may also be essential if you need it for work, school, job applications, banking, or important communication.

Groceries

A bare bones grocery budget should focus on simple meals and basic household food needs. This does not mean eating badly. It means planning meals around affordable staples and reducing extras for a short time.

Dining out, takeout, delivery fees, and frequent coffee runs usually move out of the budget during this period.

Transportation

Include the cost of getting to work, school, medical appointments, or necessary errands. This may include gas, public transit, car insurance, parking, tolls, or required car maintenance.

If transportation helps you earn income or handle essential responsibilities, it belongs in the plan.

Insurance

Keep important insurance payments in view, especially health, auto, renters, homeowners, or life insurance if your family depends on it.

Canceling insurance too quickly can create bigger financial risk later, so this is one area to review carefully before making changes.

Minimum Debt Payments

If you have credit cards, loans, or other debts, include at least the minimum payments if possible. Missing payments can lead to fees, extra interest, collection calls, or credit damage.

If you cannot make minimum payments, contact the lender or servicer before the due date when possible. Some may offer hardship options.

Essential Medical Costs

Include prescriptions, medical co-pays, urgent care needs, therapy, medical supplies, or other health costs you cannot safely skip.

A bare bones budget should reduce pressure, not put your health at risk.

Childcare or Family Care

If childcare is needed so you can work, attend school, or keep important appointments, it belongs in your bare bones budget.

The same applies to essential elder care, child support, or family obligations that are necessary and ongoing.

Basic Personal and Household Items

Some personal and household items are still necessary, even during a tight season. This may include toiletries, cleaning supplies, diapers, laundry detergent, basic hygiene products, and school or work essentials.

These costs are easy to underestimate, so give them a small but realistic amount instead of leaving them out completely.

Bare Bones Budget Example

A bare bones budget is easier to understand when you can see what changes. The point is not to cut every dollar of joy from your life. It is to separate what must stay from what can pause for a short time.

Here is a simple example for someone earning $3,500 per month after taxes.

| Category | Regular Budget | Bare Bones Budget |

|---|---|---|

| Rent | $1,300 | $1,300 |

| Utilities | $250 | $250 |

| Groceries | $550 | $425 |

| Dining Out | $250 | $0 |

| Transportation | $300 | $275 |

| Insurance | $250 | $250 |

| Minimum Debt Payments | $300 | $300 |

| Subscriptions | $75 | $15 |

| Entertainment | $150 | $0 |

| Clothing | $100 | $25 |

| Personal and Household Items | $175 | $125 |

| Savings or Catch-Up Fund | $0 | $535 |

| Total | $3,700 | $3,500 |

In this example, the regular budget is not working because expenses are higher than income. The bare bones version cuts back on dining out, entertainment, subscriptions, clothing, and flexible grocery spending. That creates room to cover the basics without going further behind.

Your numbers will look different, but the idea is the same: protect the essentials first, pause what can wait, and give any freed-up money a clear job.

How to Create a Bare Bones Budget Step by Step

A bare bones budget works best when it is simple. You are not trying to build the perfect budget here. You are trying to get a clear picture of what must be paid first and what can wait.

1. Add Up Your Current Income

Start with the money you realistically expect to receive this month. Use your after-tax income, not your gross pay.

Include paychecks, freelance income you are confident will arrive, unemployment benefits, child support, side income, or any other money you can reasonably count on.

If your income is uncertain, use the lower estimate. It is better to build a cautious plan and have extra money later than to plan around income that may not arrive.

2. List Your True Essentials

Next, list the expenses that protect your basic needs and financial stability.

This usually includes housing, utilities, groceries, transportation, insurance, minimum debt payments, essential medical costs, childcare, and basic household items.

Be honest, but not harsh. A bare bones budget should remove extras, not ignore real needs.

3. Pause or Reduce Non-Essential Spending

Now look at the expenses that can pause for a short time.

This may include dining out, subscriptions, shopping, entertainment, travel, upgrades, hobbies, and non-urgent personal spending.

You do not have to cancel everything forever. In many cases, you are simply pressing pause until your money has more breathing room.

4. Lower Flexible Essentials Where You Can

Some essentials stay in the budget, but the amount may be adjustable.

Groceries are a good example. You still need food, but you may be able to reduce spending with meal planning, store brands, leftovers, and fewer convenience items.

Transportation, phone plans, insurance premiums, and household supplies may also have room for small adjustments. The point is not to make life miserable. It is to find realistic savings without cutting what keeps you stable.

5. Decide Where the Freed-Up Money Goes

A bare bones budget should have a clear purpose. Any money you free up should go toward the problem you are trying to solve.

That might mean catching up on rent, paying an overdue utility bill, covering a medical bill, rebuilding a small emergency fund, or stopping new credit card debt.

Without a clear destination, the saved money can disappear into random spending. Give it a job before the month starts.

6. Review Weekly While Money Is Tight

A bare bones budget needs more frequent check-ins than a normal budget because there is less room for mistakes.

Once a week, compare your spending with your plan. Check what has been paid, what is still due, and whether any new expense has appeared.

This does not need to take long. A 10-minute review can help you catch small problems before they turn into another stressful month.

What Not to Cut Too Quickly

A bare bones budget is about cutting back, but not every cut is safe or helpful. Some expenses protect you from bigger problems later, so review them carefully before removing them.

Health Insurance and Medical Needs

Canceling health insurance, skipping prescriptions, or delaying necessary care can create serious risk. If medical costs are too high, look for lower-cost options, payment plans, discount programs, or community clinics before cutting care completely.

Car Insurance

If you drive, car insurance is usually not optional. Letting coverage lapse can lead to legal problems, higher future premiums, and major financial risk if an accident happens.

You may be able to shop for a lower rate, adjust coverage, or ask about discounts, but avoid canceling required coverage without understanding the consequences.

Minimum Debt Payments

Minimum payments may feel frustrating, especially during a tight season. But missing them can lead to late fees, extra interest, collection calls, or credit damage.

If you cannot afford the minimum payment, contact the lender before the due date when possible. A hardship plan may be better than simply missing the payment.

The CFPB also recommends contacting your credit card company right away if you cannot pay your bill, since many card companies may work with you during a financial emergency.

Basic Food and Household Needs

A bare bones budget should reduce grocery waste and convenience spending, not leave you without enough food or basic household items.

Keep room for simple meals, toiletries, laundry supplies, diapers, cleaning products, and other basics your household needs to function.

Childcare and Transportation Needed for Work

If childcare or transportation helps you keep earning income, treat it carefully. Cutting these costs too quickly may make it harder to work, attend interviews, or handle essential responsibilities.

Look for ways to reduce the cost first, but do not remove something that helps you stay employed or keep your household stable.

When to Stop Using a Bare Bones Budget

A bare bones budget is meant to help you through a tight season. It should not become your permanent money plan unless your situation truly requires it.

You may be ready to ease back when your income feels steady again, your most urgent bills are caught up, and you are no longer relying on credit cards for basic expenses.

Another sign is that you have some breathing room in savings. It does not have to be a full emergency fund right away. Even a small cushion can make it easier to move from survival mode back to a more balanced budget.

When things improve, add spending back slowly. Start with the categories that support your real life, such as a realistic grocery amount, basic personal care, small fun money, or savings for irregular expenses.

Try not to swing from strict cutting to full spending all at once. That can undo the progress you made. A better approach is to rebuild your regular budget one category at a time.

FAQs About Bare Bones Budgets

What is a bare bones budget?

A bare bones budget is a temporary budget that covers only your most essential expenses. It usually includes housing, utilities, groceries, transportation, insurance, minimum debt payments, essential medical costs, childcare if needed, and basic household items.

What should be included in a bare bones budget?

Include expenses that protect your home, health, income, basic food, transportation, and financial obligations. Common bare bones budget categories include rent or mortgage, utilities, groceries, gas or public transit, insurance, minimum debt payments, prescriptions, childcare, and necessary household supplies.

How long should you use a bare bones budget?

Use a bare bones budget only as long as you need it. Some people use it for one month to catch up on bills, while others may use it for a few months during job loss, reduced income, or debt pressure. Once your income and bills feel more stable, you can slowly return to a more balanced budget.

Is a bare bones budget the same as a low-income budget?

Not exactly. A low-income budget may be a long-term plan for managing money on a smaller income. A bare bones budget is usually a short-term plan for cutting back to essentials during a tight season, emergency, or short-term financial setback.

What expenses should you not cut from a bare bones budget?

Be careful before cutting health insurance, prescriptions, basic groceries, required car insurance, minimum debt payments, childcare needed for work, and transportation that helps you earn income. These expenses may be frustrating, but cutting them too quickly can create bigger problems later.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.