Unexpected expenses have a way of showing up at the worst possible time.

Your car needs a repair. A medical bill lands in your inbox. Your hours get cut at work. Suddenly, money you planned to use for rent, groceries, or bills has to stretch even further.

That is where an emergency fund helps.

An emergency fund is money you set aside for real, urgent surprises. It gives you a small financial cushion so one bad week does not turn into months of stress or credit card debt.

And no, you do not need to save thousands of dollars overnight. Even a small emergency fund can make life feel a little less shaky.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

Quick Takeaways

- An emergency fund is money set aside for unexpected, necessary, and urgent expenses.

- A good long-term goal is 3 to 6 months of essential expenses, but you can start with $500 or $1,000.

- Base your emergency fund on your must-pay expenses, not your full income.

- Keep the money in a separate, easy-to-access savings account.

- Use it for real emergencies like job loss, urgent car repairs, medical bills, or essential home repairs.

- If you use your emergency fund, rebuild it as soon as you can.

What Is an Emergency Fund?

An emergency fund is money you keep aside for unexpected, necessary expenses.

It is not for regular bills, planned purchases, or “I deserve a treat” spending. It is for moments when life throws an expense at you that cannot safely wait.

For example, an emergency fund can help cover:

- A sudden car repair you need to get to work

- An urgent medical or dental bill

- Rent or groceries after a job loss

- A necessary home repair

- Emergency travel for a family situation

- A temporary drop in income

Think of it as a financial buffer between you and panic mode.

Without an emergency fund, even a $400 surprise can turn into credit card debt, missed bills, or borrowing money you would rather not borrow. With one, you may still be annoyed by the expense, but at least you have a plan.

Small cushion, big sigh of relief.

Why an Emergency Fund Matters

An emergency fund gives you options when life gets expensive without warning.

Without savings, a surprise expense can quickly turn into a bigger money problem. You may have to use a credit card, take out a loan, delay an important bill, or borrow from someone else.

That can make one emergency cost even more over time.

For example, a $600 car repair is stressful enough. But if you put it on a high-interest credit card and can only make small payments, that repair may end up costing much more than $600.

An emergency fund helps you avoid that cycle.

It can also make your budget feel less fragile. When you know you have money set aside, you do not have to treat every unexpected bill like a full financial crisis.

The goal is not to remove every money problem. That would be lovely, but sadly, bills did not get that memo.

The goal is to give yourself a cushion so one surprise does not knock your whole budget off track.

How Much Should You Have in an Emergency Fund?

A common emergency fund goal is 3 to 6 months of essential expenses.

That does not mean 3 to 6 months of your full income. It means the basic expenses you would need to cover if something went wrong, such as rent, groceries, utilities, insurance, minimum debt payments, and transportation.

For many beginners, that number can feel too big at first.

So instead of starting with the full goal, build your emergency fund in stages:

| Stage | Goal | Best For |

|---|---|---|

| Starter emergency fund | $500 to $1,000 | Your first cushion for small emergencies |

| One-month emergency fund | 1 month of essentials | More breathing room if income drops |

| Full emergency fund | 3 to 6 months of essentials | Stronger protection for job loss or major surprises |

| Larger emergency fund | 6 to 12 months of essentials | Self-employed workers, irregular income, or single-income households |

If saving 3 months of expenses feels impossible right now, start with $500. If that feels hard, start with $100.

The first goal is not perfection. It is distance between you and zero.

A small emergency fund is still progress. It can help cover a minor car repair, a surprise bill, or part of an urgent expense without throwing your entire budget into chaos.

Emergency Fund Formula

The easiest way to estimate your emergency fund goal is to focus on your essential monthly expenses.

Use this simple formula:

Monthly essential expenses × number of months = emergency fund goal

For example, if your basic monthly expenses are $3,000, then:

| Emergency Fund Goal | Calculation | Amount |

|---|---|---|

| 1 month | $3,000 × 1 | $3,000 |

| 3 months | $3,000 × 3 | $9,000 |

| 6 months | $3,000 × 6 | $18,000 |

Your essential expenses usually include the things you would still need to pay for during a job loss, medical issue, or temporary income drop.

That means your emergency fund should be based on your real-life needs, not a random number someone online says you “must” have.

A $1,000 starter fund may be enough for smaller emergencies, but it may not cover a full month of rent, bills, and groceries. That is why it helps to build in stages instead of stopping at one number forever.

Start with a small cushion. Then keep going until your fund can protect your actual monthly life.

What Expenses Should Your Emergency Fund Cover?

Your emergency fund should cover the bills you would still need to pay if your income suddenly dropped or a major expense showed up.

Think of it as your “keep life running” money.

Usually, this includes:

- Rent or mortgage

- Utilities

- Groceries

- Insurance

- Minimum debt payments

- Transportation

- Phone and internet

- Basic medical costs

- Childcare or essential pet care

It does not need to include every normal monthly expense.

For example, if you usually spend money on restaurants, subscriptions, shopping, entertainment, or extra debt payments, those may not need to be part of your emergency fund number. In a real emergency, you would likely pause or reduce those costs.

Here is a simple way to separate them:

| Include in Emergency Fund | Usually Do Not Include |

|---|---|

| Rent or mortgage | Vacation savings |

| Groceries | Shopping |

| Utilities | Entertainment |

| Insurance | Dining out |

| Minimum debt payments | Extra debt payments |

| Transportation | Non-essential subscriptions |

| Childcare | Home decor or upgrades |

This keeps your emergency fund goal more realistic.

If your normal monthly spending is $4,000, but your true essentials are $2,800, you can build your emergency fund around the $2,800 number first.

That makes the goal less scary and much easier to start.

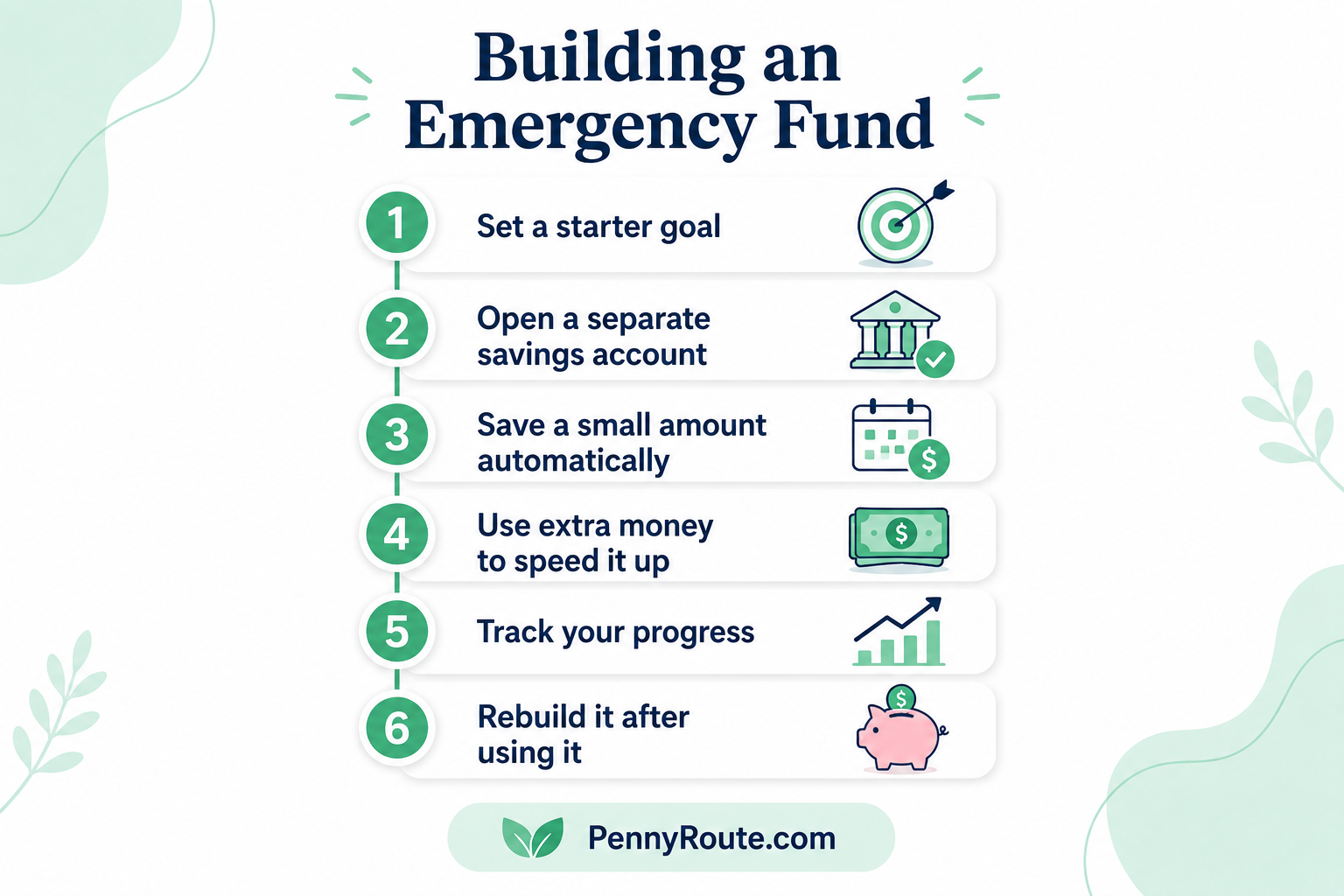

How to Build an Emergency Fund Step by Step

Building an emergency fund is easier when you stop looking at the full number first.

Yes, saving 3 to 6 months of expenses is a great long-term goal. But if you are starting from zero, your first job is much simpler: build a small cushion and make saving a habit.

Set a Starter Goal

Start with a goal that feels possible.

For many people, that might be $500 or $1,000. If that still feels too much right now, start with $100 or $250.

The point is to get your emergency fund moving. Once you reach your first goal, you can raise it.

Small goals are not “less serious.” They are how serious progress begins.

Open a Separate Savings Account

Try to keep your emergency fund separate from your everyday spending money.

If it sits in your checking account, it may slowly disappear into groceries, takeout, small purchases, and those “I’ll replace it next week” moments.

A separate savings account creates a little distance. Not so much that you cannot access the money, but enough that you do not spend it by accident.

Save a Small Amount Automatically

Pick an amount you can save regularly, even if it is small.

That could be:

- $10 per week

- $25 per paycheck

- $50 per month

- 5% of any extra income

Automatic transfers work well because you do not have to remember every time. The money moves before you can talk yourself out of it.

Use Extra Money to Speed It Up

When extra money comes in, send some of it to your emergency fund.

This could include:

- Tax refunds

- Work bonuses

- Cashback rewards

- Side hustle income

- Gift money

- Money from selling unused items

You do not have to put every extra dollar into savings. But using a portion can help your emergency fund grow much faster.

Track Your Progress

Check your emergency fund once a month.

You do not need a fancy system. A simple note, spreadsheet, or savings tracker is enough.

For example:

| Goal | Current Amount | Left to Save |

|---|---|---|

| $500 starter fund | $175 | $325 |

| $1,000 starter fund | $175 | $825 |

| 1 month of essentials | $175 | $2,325 |

Tracking progress keeps the goal visible. And honestly, watching the number grow can be oddly satisfying in the best way.

Rebuild It After You Use It

Using your emergency fund is not failure. That is what it is there for.

If you need to use part of it for a real emergency, pause and rebuild it afterward. Go back to your automatic transfers, add extra money when possible, and work your way back to your target amount.

An emergency fund is not a one-time project. It is a money habit that protects you again and again.

Where Should You Keep Your Emergency Fund?

Your emergency fund should be easy to access, but not too easy to spend.

The best place is usually a separate savings account, ideally one that earns some interest and lets you withdraw money when you need it.

Good options include:

- A high-yield savings account

- A regular savings account

- A money market account

- A separate account at your bank or credit union

The key is to keep the money safe, separate, and available.

You do not want your emergency fund tied up in something risky or difficult to access. If your car breaks down or your income suddenly drops, you should not have to wait days, sell investments at a loss, or pay a penalty just to use your own money.

Try to avoid keeping your emergency fund in:

- Stocks

- Crypto

- Long-term investment accounts

- Certificates of deposit with withdrawal penalties

- Your everyday checking account

- Cash at home as your full emergency fund

Keeping a small amount of cash at home can be useful for short-term emergencies, but it is usually not the best place for your entire fund.

A good setup might look like this:

| Emergency Fund Location | Best For |

|---|---|

| Checking account | A very small buffer for immediate expenses |

| High-yield savings account | Main emergency fund |

| Cash at home | Small short-term backup |

| Investment account | Not ideal for emergency savings |

Your emergency fund should not be working hard to grow like an investment. Its main job is to be there when you need it.

Think boring, safe, and accessible. Not exciting, risky, and “let’s hope the market is having a good week.”

The FDIC specifically recommends considering a separate FDIC-insured savings account for emergency savings so it is less tempting to use the money for everyday expenses.

When Should You Use Your Emergency Fund?

Use your emergency fund for expenses that are unexpected, necessary, and urgent.

A simple way to decide is to ask three questions:

- Is it unexpected?

- Is it necessary?

- Is it urgent?

If the answer is yes to all three, it may be a real emergency.

For example, a car repair may count if you need your car to get to work. A medical bill may count if it cannot wait. Rent or groceries may count if you lose income and need help covering essentials.

But a last-minute vacation deal, a new phone upgrade, or a holiday sale usually does not count.

Here is a simple guide:

| Use Your Emergency Fund For | Do Not Use It For |

|---|---|

| Job loss or income drop | Vacation |

| Urgent car repair | Shopping |

| Medical or dental emergency | Dining out |

| Essential home repair | Entertainment |

| Emergency travel | Planned upgrades |

| Groceries during income loss | Non-urgent purchases |

The point of an emergency fund is not to make every hard choice disappear. It is to protect you from the expenses that could seriously disrupt your life or push you into debt.

And if you do need to use it, do not feel guilty.

That money did its job. Your next step is simply to rebuild it.

Emergency Fund vs. Rainy Day Fund vs. Sinking Fund

Emergency funds, rainy day funds, and sinking funds all help you save money, but they are not exactly the same.

The difference comes down to size, purpose, and timing.

| Type of Fund | What It Is For | Example |

|---|---|---|

| Emergency fund | Larger unexpected expenses that could disrupt your finances | Job loss, major car repair, urgent medical bill |

| Rainy day fund | Smaller unexpected expenses | Minor repair, surprise bill, replacing a broken appliance |

| Sinking fund | Planned future expenses | Holiday gifts, car insurance, annual subscriptions, vacation |

An emergency fund is your bigger safety net. It helps protect your essential expenses if something serious happens.

A rainy day fund is usually smaller. It can help with annoying surprises that are not huge emergencies, but still need money soon.

A sinking fund is different because the expense is expected. You know it is coming, so you save for it little by little.

For example, if your car suddenly breaks down, that may be an emergency fund expense. But if you know your car insurance is due every six months, that should be a sinking fund.

This separation helps you avoid using your emergency fund for things that are not true emergencies.

Your emergency fund is for “Uh-oh, I need money now.”

Your sinking fund is for “I know this bill is coming, so let’s not act surprised again.”

Should You Build an Emergency Fund or Pay Off Debt First?

If you have debt, it can be tempting to put every extra dollar toward paying it off.

That makes sense, especially if the debt has a high interest rate. But before you throw all your money at debt, it usually helps to build a small emergency fund first.

Why?

Because without any savings, one surprise expense can send you right back into debt.

For example, let’s say you put an extra $500 toward your credit card. That feels great. But then your car needs a $500 repair and you have no savings, so the repair goes back on the credit card.

Now you are back where you started, just more frustrated. Very fair. Very annoying.

A better beginner-friendly approach is:

- Build a small starter emergency fund.

- Keep making minimum debt payments.

- Focus extra money on high-interest debt.

- Continue saving small amounts when possible.

- Increase your emergency fund once the debt is more manageable.

A starter fund of $500 to $1,000 can give you some breathing room while you work on debt. It may not cover every emergency, but it can stop smaller surprises from becoming new debt.

If your income is unstable, your job feels uncertain, or you have dependents, you may want a slightly larger cushion before aggressively paying down debt.

The goal is balance. You want to reduce debt, but you also want enough savings to avoid depending on that same debt every time life gets messy.

How to Build an Emergency Fund on a Low Income

Building an emergency fund can feel harder when your income is already stretched.

If most of your money goes toward rent, groceries, bills, transportation, and debt payments, saving may not feel simple. And honestly, it may not be simple.

But it can still be possible if you start small and keep the goal realistic.

Instead of aiming for 3 to 6 months right away, focus on your first $100. Then $250. Then $500.

Small amounts count because your first emergency fund is not about becoming fully protected overnight. It is about creating a little space between you and the next surprise expense.

Here are a few ways to start:

- Save $5 or $10 each week

- Round up purchases and move the difference to savings

- Put cashback rewards into your emergency fund

- Save part of any tax refund, bonus, or gift money

- Pause one small non-essential expense temporarily

- Sell unused items and save the money

- Use a separate account so the money does not blend into daily spending

For example, saving $10 a week gives you about $520 in one year. That may not sound huge, but it can cover a small emergency without using a credit card.

If saving every week is not realistic, save when you can. Some months may be better than others.

The key is to avoid all-or-nothing thinking. You are not failing because you can only save a small amount. You are building a habit under real-life conditions, and that deserves credit.

How Often Should You Review Your Emergency Fund?

Review your emergency fund at least once or twice a year, or whenever your life changes in a big way.

Your emergency fund number is not fixed forever. It should grow or adjust as your expenses change.

You may need to review it if:

- Your rent or mortgage changes

- Your income increases or drops

- You change jobs

- You move to a new city

- You have a child

- You become self-employed

- You buy a home

- Your monthly bills increase

- You pay off a major debt

For example, if your essential expenses were $2,500 per month last year but are now $3,000, your emergency fund goal should reflect the new number.

A 3-month emergency fund would change from $7,500 to $9,000.

You do not need to recalculate it every week. That would be a bit much, and your savings account does not need that kind of pressure.

Just check in occasionally and ask:

“Would this amount still protect me if something happened?”

If the answer is no, raise your goal slowly. Add a little more each month until your emergency fund matches your current life.

Common Emergency Fund Mistakes to Avoid

Building an emergency fund is simple in theory, but a few small mistakes can make it harder to keep the money there when you need it.

Here are the common ones to watch for.

Waiting Until You Can Save a Big Amount

You do not need to save hundreds of dollars at once to start an emergency fund.

Waiting for the “perfect” month can keep you stuck at zero. Start with what you can manage, even if it is $5 or $10 at a time.

The habit matters first. The bigger balance comes later.

Keeping It Mixed With Spending Money

If your emergency fund sits in the same account you use for bills, groceries, and everyday purchases, it becomes much easier to spend without noticing.

A separate savings account helps protect it from normal spending.

Not because you have no self-control, but because money in checking tends to develop legs. Tiny little debit-card legs.

Using It for Non-Emergencies

Your emergency fund should not become a backup shopping account.

A sale, vacation, new gadget, or planned annual bill is not usually an emergency. Those are better handled with sinking funds or regular savings.

Before using the money, ask: Is this unexpected, necessary, and urgent?

Investing Your Emergency Fund

Your emergency fund should be safe and easy to access.

Investing it in stocks, crypto, or other risky assets can put the money at risk right when you need it. If the value drops during an emergency, you may have to sell at a loss.

Emergency savings are not meant to be exciting. They are meant to be available.

Not Rebuilding It After Using It

If you use your emergency fund for a real emergency, that is not a mistake.

The mistake is not refilling it afterward.

Once the emergency passes, restart your savings plan. Even small automatic transfers can help you rebuild the cushion over time.

Setting the Goal Based on Income Instead of Expenses

Your emergency fund should be based on your essential expenses, not your full income.

For example, if you earn $4,500 per month but your basic expenses are $3,000, your 3-month emergency fund goal would be closer to $9,000, not $13,500.

That makes the goal more realistic and more useful.

Emergency Fund Example for a Beginner

Let’s say your essential monthly expenses are $2,500.

That includes your rent, groceries, utilities, insurance, minimum debt payments, transportation, and basic phone bill.

A full emergency fund may look like this:

| Goal | Amount |

|---|---|

| Starter emergency fund | $500 to $1,000 |

| 1 month of essentials | $2,500 |

| 3 months of essentials | $7,500 |

| 6 months of essentials | $15,000 |

Seeing $15,000 as the final goal might feel overwhelming at first. That is normal.

So do not start there.

Start with the first milestone: $500.

If you save $25 per week, you would have about $100 in one month and $500 in about five months. If you add extra money from a tax refund, bonus, side hustle, or cashback rewards, you may reach it faster.

Once you hit $500, aim for $1,000. After that, work toward one month of essential expenses.

This gives you a clear path instead of one giant savings goal staring at you like a mountain with bills attached.

The important thing is to keep moving from one stage to the next. Your emergency fund does not have to be finished before it becomes useful. Even the first few hundred dollars can protect you from small surprises and give your budget more breathing room.

Emergency Fund FAQs

How much should I have in an emergency fund?

A good long-term goal is 3 to 6 months of essential expenses. If that feels too high right now, start smaller. Aim for $500, then $1,000, then one month of essentials. The best emergency fund is the one you actually start building.

Is $1,000 enough for an emergency fund?

$1,000 can be a helpful starter emergency fund, especially if you are starting from zero. But for many people, it will not cover a full month of rent, bills, groceries, and transportation. Once you reach $1,000, keep building toward at least one month of essential expenses.

Should I keep my emergency fund in checking or savings?

A savings account is usually better. Your emergency fund should be easy to access, but separate from your everyday spending money. If it sits in checking, it may be too easy to spend on regular purchases.

Can I invest my emergency fund?

It is usually better not to invest your emergency fund.

Emergency savings should be safe and available when you need them. Investments can lose value, and you may be forced to sell at the wrong time during an emergency.

Should I build an emergency fund before paying off debt?

In most cases, it helps to build a small starter emergency fund first. Even $500 to $1,000 can stop small surprises from going back onto a credit card. After that, you can focus more heavily on high-interest debt while still saving small amounts when possible.

What counts as an emergency?

A true emergency is usually unexpected, necessary, and urgent. Examples include job loss, urgent car repairs, medical bills, essential home repairs, or covering basic expenses during an income drop.

Is an emergency fund the same as a rainy day fund?

Not exactly. A rainy day fund is usually for smaller surprise costs, like a minor repair or unexpected bill. An emergency fund is larger and meant for bigger financial disruptions, such as job loss or a major expense.

How often should I update my emergency fund goal?

Review it once or twice a year, or after a major life change.

If your rent, income, bills, family size, or job situation changes, your emergency fund goal may need to change too.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.