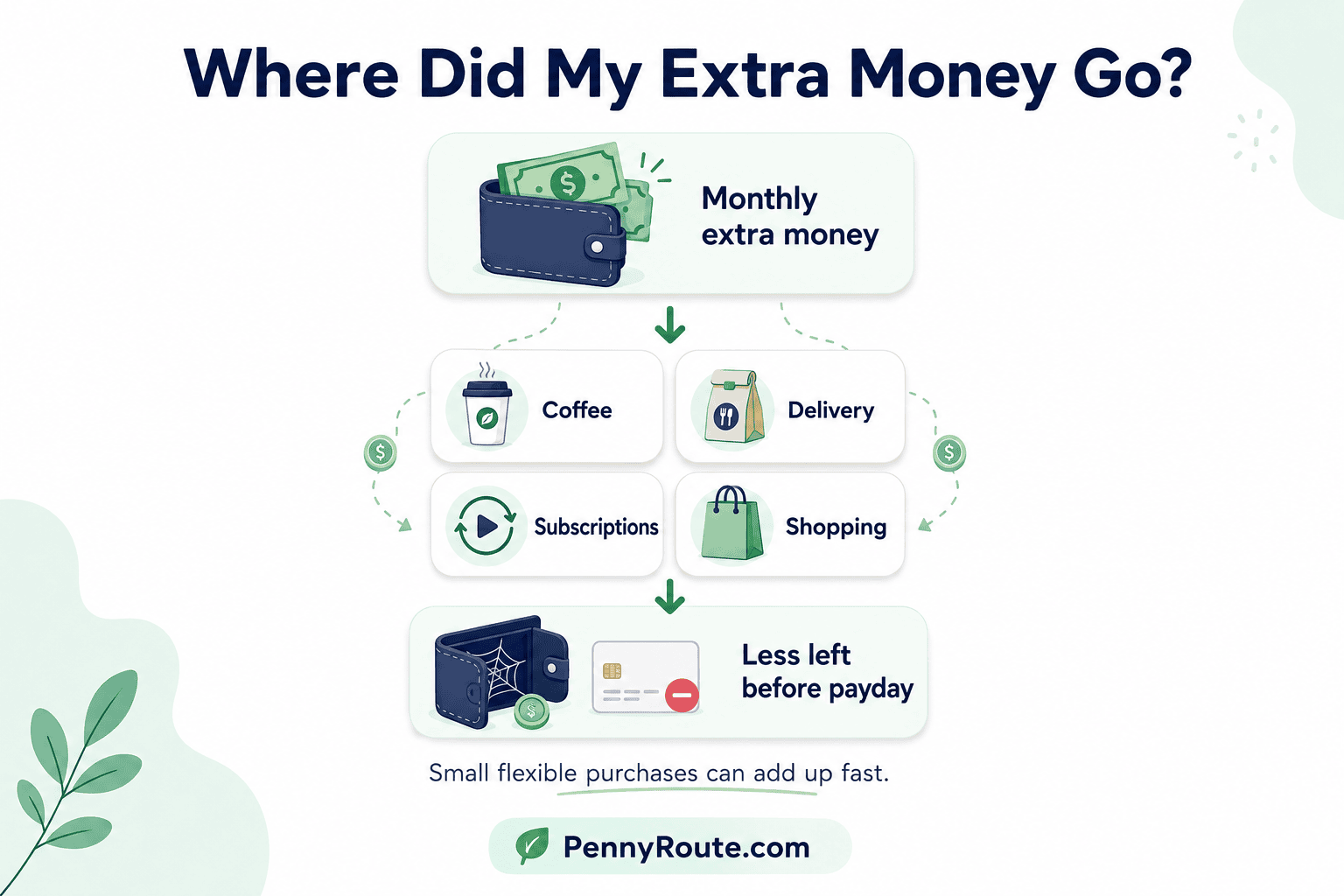

You get paid, cover the important bills, buy a few small things, and somehow your money still disappears faster than expected. It is not always one big purchase causing the problem. Often, it is the flexible spending that slips through quietly.

Discretionary spending includes the non-essential purchases you can reduce, delay, or skip when your budget needs more room. That does not mean these expenses are bad. It simply means they are adjustable.

Once you know what counts as discretionary spending, it becomes easier to set limits, protect your savings goals, and spend on the things you actually enjoy without guessing where your money went.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

Quick Overview: Discretionary Spending

- Discretionary spending is money spent on non-essential purchases you can reduce, delay, pause, or skip.

- Common examples include dining out, subscriptions, entertainment, shopping, hobbies, travel, and impulse buys.

- In a personal budget, discretionary spending usually falls under “wants,” not basic needs.

- A common starting point is to keep wants around 30% of take-home pay, but your real limit depends on your income, bills, debt, savings goals, and cost of living.

- The easiest way to control discretionary spending is to track it, set a monthly limit, and cut unused or low-value expenses first.

What Is Discretionary Spending?

Discretionary spending is the part of your spending that is optional or flexible. These are expenses you choose based on your lifestyle, preferences, habits, convenience, or comfort.

You may enjoy them. You may even value them. But if money gets tight, you usually have some control over how much you spend in these areas.

For example, rent is usually not discretionary because you need housing. But ordering takeout three times a week is discretionary because you could reduce it, cook more often, or choose cheaper meals.

Discretionary spending is not the same as “wasteful spending.” A gym membership, hobby, streaming service, or weekend dinner can be worth keeping if it fits your budget and supports your life.

The problem starts when flexible spending grows without a plan. That is when small choices begin pushing out savings, debt payoff, or bills.

When you make a budget, discretionary expenses help you see where you have room to adjust without touching your basic needs first.

Discretionary Spending Examples

Discretionary spending looks different for every household, but it usually includes purchases that make life more enjoyable, convenient, or comfortable.

Common discretionary spending examples include:

- Dining out

- Coffee shop drinks

- Food delivery fees

- Streaming services

- Subscription boxes

- Concerts, movies, and events

- Hobbies and crafts

- Gaming purchases

- Extra clothing and accessories

- Beauty treatments

- Home decor

- Vacations and weekend trips

- Gym memberships

- Apps and digital subscriptions

- Impulse buys

- Upgraded versions of things you already own

Some of these expenses may be perfectly reasonable. A $15 streaming service may bring more value than several random $15 purchases you barely remember. The point is not to remove every want from your life. The point is to choose them on purpose.

What Counts as Discretionary Spending?

Some expenses are easy to label. A concert ticket is usually discretionary. Rent usually is not.

Other expenses sit in the middle. Groceries are essential, but premium snacks, fancy drinks, and last-minute convenience items may be flexible. Transportation to work may be essential, but frequent rideshares for convenience may be discretionary if cheaper options are available.

Use this table as a practical starting point.

| Expense | Usually Discretionary? | Why |

|---|---|---|

| Restaurant meals | Yes | You can usually reduce, delay, or replace them with lower-cost meals. |

| Basic groceries | No | Food is essential, even if the exact grocery choices can vary. |

| Premium snacks and drinks | Sometimes | Basic food is necessary, but extras may be flexible. |

| Rent or mortgage | No | Housing is usually a required living cost. |

| Streaming subscriptions | Yes | They can usually be paused, canceled, or reduced. |

| Health insurance | No | It protects against major medical and financial risk. |

| Extra clothing | Usually | Basic clothing may be necessary, but extra outfits are flexible. |

| Childcare needed for work | Usually no | It may be essential if it allows you to earn income. |

| Weekend trips | Yes | Travel for fun can usually be delayed or reduced. |

| Rideshare trips | Sometimes | It depends on safety, location, schedule, and available alternatives. |

| Minimum debt payments | No | These are required payments that protect your credit and avoid fees. |

| Extra debt payments | Sometimes | They are planned financial choices, not everyday discretionary spending. |

A helpful test is simple:

Can I reduce, delay, pause, or skip this expense without losing a basic need?

If the answer is yes, it is probably discretionary.

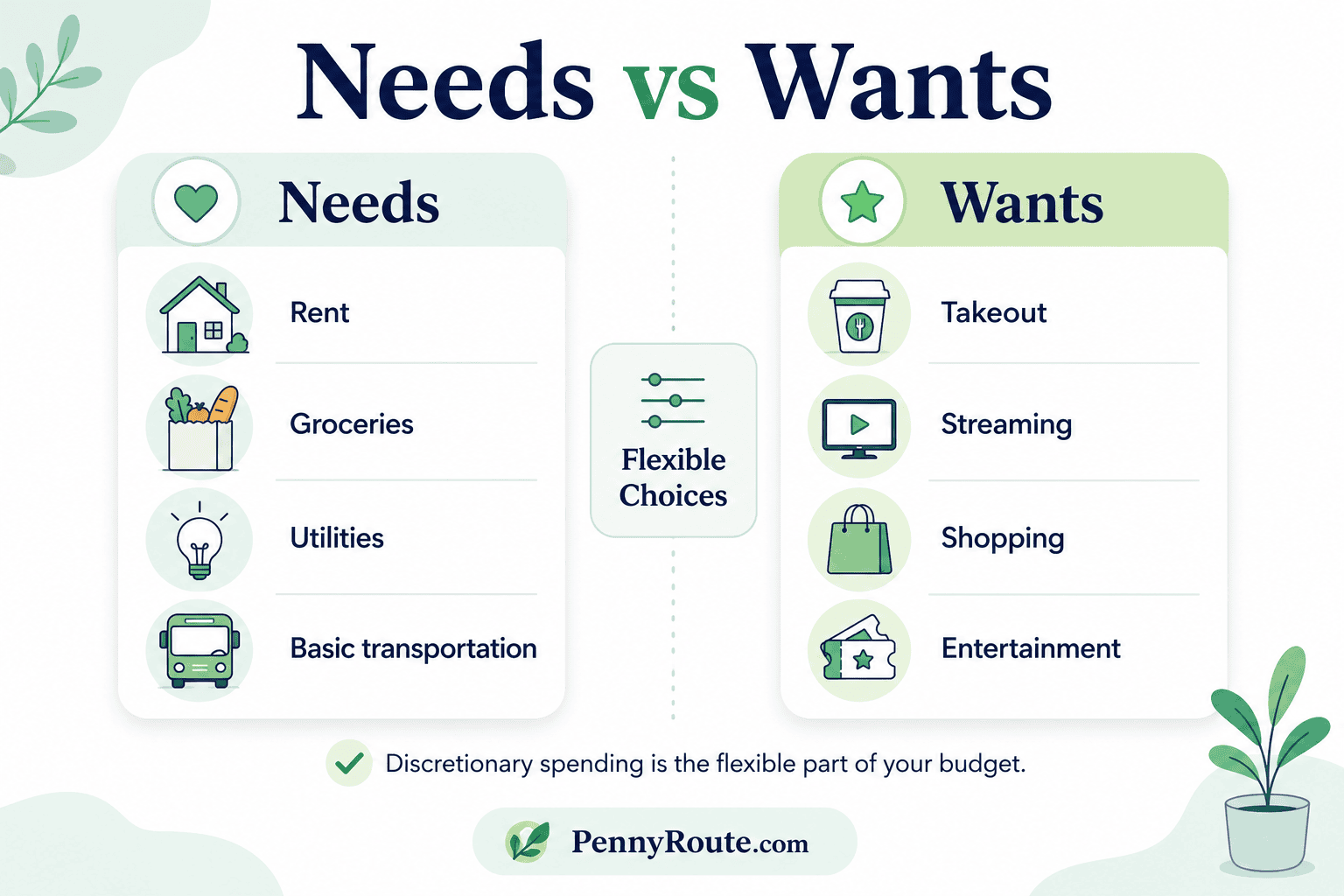

Discretionary vs Non-Discretionary Spending

The difference between discretionary and non-discretionary spending comes down to flexibility.

Non-discretionary spending covers basic needs and required obligations. These are expenses you usually need to pay to live safely, keep income coming in, protect your health, or avoid serious financial trouble.

The CFPB also explains budgeting through needs and wants, which is a helpful way to separate required expenses from flexible spending. In simple terms, needs are the expenses you must cover first, while wants are the purchases you can adjust when your budget needs more room.

Examples include:

- Rent or mortgage

- Basic groceries

- Utilities

- Health insurance

- Car insurance

- Transportation to work

- Minimum debt payments

- Childcare needed for work

- Prescription medicine

- Basic phone service

Discretionary spending covers wants, upgrades, extras, and lifestyle choices. These expenses may matter to you, but they usually have more room for adjustment.

Examples include:

- Dining out

- Entertainment

- Subscriptions

- Vacations

- Hobbies

- Decor

- Food delivery

- Extra shopping

- Premium upgrades

This distinction helps when you are reviewing your monthly budget categories. If money is tight, you usually want to review discretionary expenses before cutting essentials.

That does not mean essential bills are impossible to lower. You may be able to shop for cheaper insurance, reduce utility usage, or move to a more affordable phone plan. But discretionary spending is often the fastest place to find immediate savings.

Discretionary Spending vs Discretionary Income

Discretionary spending and discretionary income sound similar, but they are not the same.

Discretionary income is the money left after necessary expenses are paid. In simple budgeting terms, it is the money you have available after essentials like housing, food, utilities, insurance, transportation, and required payments.

Discretionary spending is how much of that leftover money you actually spend on non-essential purchases.

For example:

- Take-home pay: $4,000

- Essential expenses: $2,800

- Money left after essentials: $1,200

- Discretionary spending: $650

- Remaining money for savings, extra debt payments, or other goals: $550

In this example, the person has $1,200 available after essentials, but they spend $650 of it on flexible expenses.

That difference matters because having discretionary income does not automatically mean you are saving. If all of it goes to dining out, subscriptions, shopping, and convenience spending, your budget may still feel tight.

How to Calculate Your Discretionary Spending

You do not need a complicated spreadsheet to calculate discretionary spending. Start with one month of real numbers.

Use this simple process:

- Add up your take-home pay.

- Add up essential expenses.

- Add up non-essential expenses.

- Divide your discretionary spending by your take-home pay.

- Multiply by 100 to get your percentage.

Here is the basic formula:

discretionary spending ÷ take-home pay × 100 = discretionary spending percentage

Formula

Example:

- Take-home pay: $3,500

- Discretionary spending: $700

- Formula: $700 ÷ $3,500 × 100

- Result: 20%

That means 20% of take-home pay is going toward discretionary expenses.

This number is not automatically good or bad. A person with no debt, a strong emergency fund, and low fixed costs may have more room for flexible spending. Someone with credit card debt, high rent, or little savings may need a smaller discretionary spending limit for a while.

If you are new to budgeting, track the last 30 days first. Your bank and credit card statements will usually show the truth faster than memory will.

Signs Your Discretionary Spending Needs a Reset

You do not have to cut every fun expense just because you spend money on wants. But a reset may help if your flexible spending is making the rest of your budget harder.

Common signs include:

- Your bank balance surprises you before the next paycheck.

- You keep missing savings goals even when your income seems enough.

- You use credit cards for normal purchases because cash runs out.

- You regret purchases soon after making them.

- You are paying for subscriptions you rarely use.

- You avoid checking your transactions.

- You do not know where your money went at the end of the month.

- You keep saying, “It was only a few dollars,” but the total is not small.

A reset does not need to be dramatic. Sometimes the best fix is simply choosing a monthly limit and deciding which flexible expenses deserve a place in your budget.

Why Flexible Spending Gets Hard to Control

Discretionary spending often gets out of control because it feels harmless in the moment.

A $6 coffee, a $12 lunch upgrade, a $9 app charge, and a $28 delivery order may not seem like a big deal by themselves. But repeated small expenses can quietly take over money you planned to save.

A few common reasons flexible spending grows include:

Convenience spending adds up quickly

Food delivery, rideshare trips, last-minute purchases, and quick online orders save time. The problem is that convenience often carries extra fees, tips, markups, or repeat charges.

You do not need to remove convenience completely. It just needs a limit.

Subscriptions are easy to forget

Streaming services, apps, memberships, cloud storage, and subscription boxes can continue long after you stop using them regularly.

A forgotten $9.99 charge may not hurt once. But five or six forgotten charges every month can become real money.

Social spending can stretch your budget

Birthdays, dinners, trips, events, and group plans can make spending feel harder to control. Saying yes once may be fine. Saying yes to everything can slowly push your budget off track.

A simple monthly “social spending” limit can make this easier without making you feel like you have to disappear from everyone’s life.

Lifestyle creep feels normal

As income rises, wants often rise too. You upgrade your phone, eat out more, buy nicer things, or book bigger trips. Some upgrades may be worth it, but automatic upgrades can absorb raises before they improve your financial life.

This is why tracking your flexible spending matters even when your income goes up.

How Much Should You Spend on Discretionary Expenses?

There is no perfect number for discretionary spending, but the 50/30/20 rule gives a simple starting point.

Under the 50/30/20 rule, your take-home pay is divided into three broad groups:

- 50% for needs

- 30% for wants

- 20% for savings and extra debt payments

In that method, discretionary spending usually fits into the “wants” category.

For example, if your monthly take-home pay is $4,000, the 30% wants category would be $1,200.

But that does not mean you should automatically spend $1,200 on wants. Your best number depends on your real situation.

You may need a lower discretionary spending limit if:

- Your rent or mortgage takes up a large part of your income.

- You have high-interest credit card debt.

- You do not have an emergency fund.

- Your income changes from month to month.

- You are behind on bills.

- You are saving for an important goal.

You may have more room for discretionary spending if:

- Your essentials are affordable.

- You have no high-interest debt.

- You are saving consistently.

- Your emergency fund is in good shape.

- Your spending is planned instead of random.

A budget rule is a starting point, not a command. The right discretionary spending amount should help you enjoy some of your money while still making progress.

How to Control Discretionary Spending

Controlling discretionary spending does not mean becoming strict with every dollar. It means giving your flexible spending a clear boundary.

Here are practical ways to do that.

Track your flexible spending for 30 days

Before you cut anything, track your spending and find out what is actually happening.

Review your bank and credit card statements. Highlight anything that is not essential. Include dining out, entertainment, shopping, subscriptions, hobbies, food delivery, and small impulse buys.

Then add the total.

This number may be uncomfortable, but it is useful. You cannot fix a pattern you cannot see.

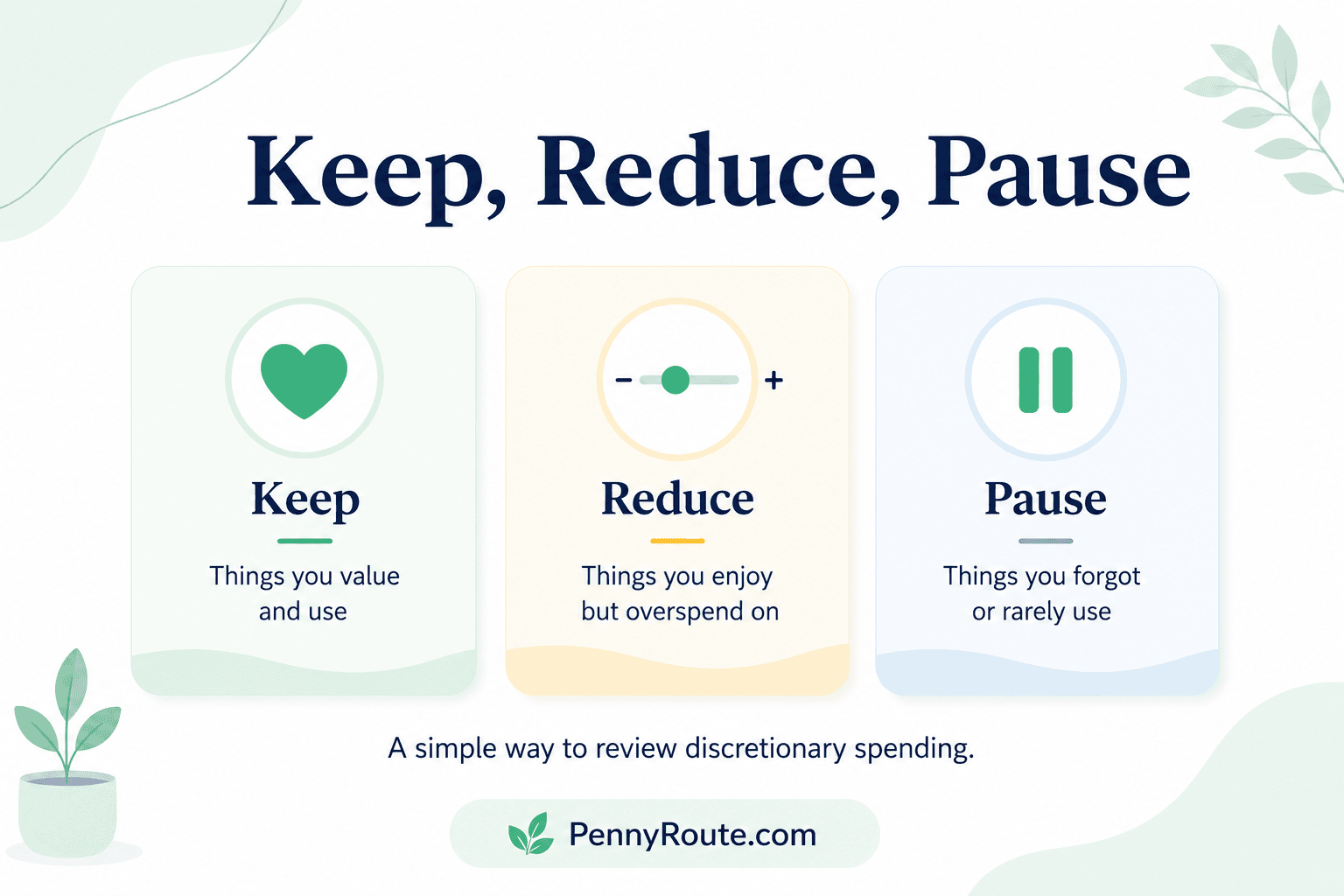

Sort expenses into keep, reduce, and pause

Do not treat every discretionary expense the same.

Use three simple groups:

Keep: Expenses you truly value and can afford.

Reduce: Expenses you enjoy but spend too much on.

Pause: Expenses you barely use, forgot about, or do not care about right now.

For example, you may keep one streaming service, reduce takeout from four times a week to once, and pause a subscription box you stopped enjoying.

That is more realistic than cutting everything at once.

Set a monthly fun money limit

A fun money limit gives you permission and structure at the same time.

You might set one limit for all discretionary spending, or you may break it into smaller categories:

- $150 for dining out

- $60 for subscriptions

- $100 for shopping

- $75 for entertainment

- $50 for hobbies

Use whatever categories match your life. The important part is that the limit is visible before you spend, not discovered after the month is over.

Use a waiting rule for impulse purchases

Impulse spending is one of the easiest ways to lose track of money.

Try a waiting rule:

- Wait 24 hours for small wants.

- Wait 7 days for medium purchases.

- Wait 30 days for larger non-essential purchases.

If you still want the item after the waiting period and it fits your budget, you can buy it without guilt.

This works because many urges fade once the moment passes.

Cancel or rotate subscriptions

You do not need five entertainment subscriptions active at the same time if you only use one or two.

Try rotating them. Keep one or two for a month, cancel the rest, and switch later if you want something different.

This keeps entertainment in your budget without letting subscriptions quietly multiply.

Move saved money immediately

When you reduce a discretionary expense, move the saved money right away.

For example, if you cancel a $20 subscription, move $20 to savings or debt payoff the same day. If you reduce takeout by $80 this month, send that $80 to your goal.

This step matters because money left sitting in checking often gets spent somewhere else.

If you are building your first safety net, moving small amounts into an emergency fund can make your progress easier to see.

Do not cut the spending that actually helps you

Some discretionary spending supports your health, relationships, or motivation.

A low-cost hobby may help you relax. A gym membership you actually use may support your routine. A monthly dinner with friends may matter to your social life.

Cutting every enjoyable expense can backfire. It may make your budget feel punishing, which often leads to overspending later.

Start with spending that is forgotten, random, unused, or out of proportion. Keep a few affordable wants that make your life better.

Simple Discretionary Spending Plan Example

Here is how a simple discretionary spending plan might look for someone earning $3,800 per month in take-home pay.

| Category | Monthly Limit |

|---|---|

| Dining out and coffee | $250 |

| Streaming and subscriptions | $60 |

| Shopping and personal items | $150 |

| Entertainment and events | $120 |

| Hobbies | $75 |

| Miscellaneous wants | $95 |

| Total discretionary spending | $750 |

In this example, discretionary spending is about 20% of take-home pay.

That leaves more room for essentials, savings, and debt payoff. It also avoids the “no fun allowed” budget that many people quit after two weeks.

Your numbers may be higher or lower. The goal is to set a limit that fits your real income and priorities.

If you struggle with unplanned purchases, a deeper look at how to stop overspending can help you build better spending rules without relying on willpower alone.

What to Do If Your Discretionary Spending Is Too High

If your number is higher than expected, do not panic. Start with the easiest wins first.

Begin with expenses that are:

- Unused

- Forgotten

- Repeated too often

- More expensive than you realized

- Not connected to real enjoyment

- Easy to replace with a cheaper option

For example, canceling two unused subscriptions is easier than cutting every restaurant meal. Reducing delivery fees may be easier than giving up all social plans. Setting a shopping limit may work better than promising to “stop buying things.”

Small changes count when they repeat every month.

If you lower discretionary spending by $150 per month, that is $1,800 per year. That money could help build savings, pay down credit card debt, or cover irregular expenses that usually catch you off guard.

Final Thoughts

Discretionary spending is not the enemy. It is simply the flexible part of your budget.

Once you know what counts, you can make better decisions with less guesswork. You can keep the things that matter, reduce the spending that does not, and give your money a clearer job.

A good budget should cover your needs, support your goals, and still leave room for some enjoyment. The balance will not look the same for everyone, and that is okay.

Start by tracking one month. Find your flexible spending number. Then choose one or two changes you can actually stick with.

FAQs About Discretionary Spending

What are 5 examples of discretionary spending?

Five common examples of discretionary spending are dining out, streaming subscriptions, entertainment, shopping, and travel. These expenses are usually considered flexible because you can reduce, delay, pause, or skip them when needed.

Is groceries discretionary spending?

Basic groceries are usually not discretionary because food is essential. However, some grocery purchases may be flexible, such as premium snacks, specialty drinks, expensive convenience foods, or extra items that are not needed.

Is discretionary spending the same as wants?

Discretionary spending is closely related to wants. In a personal budget, wants usually include non-essential expenses like restaurants, entertainment, hobbies, subscriptions, shopping, and travel.

What is a good amount for discretionary spending?

A common starting point is around 30% of take-home pay for wants under the 50/30/20 rule. However, your best number may be lower if you have high bills, debt, irregular income, or limited savings.

How do I lower discretionary spending without cutting everything?

Start by cutting unused subscriptions, reducing repeat convenience spending, setting a monthly fun money limit, and using a waiting rule for impulse purchases. Keep a few affordable expenses you truly value so your budget still feels realistic.

What is the difference between discretionary spending and discretionary income?

Discretionary income is the money left after essential expenses are paid. Discretionary spending is the amount you spend from that money on non-essential purchases.

Are credit card payments discretionary spending?

Minimum credit card payments are not discretionary because they are required obligations. Extra payments above the minimum may be part of your debt payoff plan, but they are not the same as everyday discretionary spending.

Can discretionary spending be good?

Yes. Discretionary spending can be good when it fits your budget and supports your life. Spending on hobbies, relationships, rest, or fun is not automatically a problem. It becomes a problem when it crowds out bills, savings, or debt payments.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.