Budgeting as a couple is different from budgeting on your own. Now you are dealing with shared bills, different spending habits, separate priorities, and sometimes very different comfort levels with money.

That does not mean one person has to take control or that every dollar needs to be combined. A couple’s budget simply helps you decide how income, bills, savings, debt, and personal spending will be handled together.

When the plan is clear, money conversations usually feel less awkward. You both know what needs to be paid, what you are saving for, and how much room each person has for personal spending.

You can build that plan with joint accounts, separate accounts, or a mix of both. What matters most is that the budget feels fair, clear, and easy enough for both of you to follow.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

What Is Budgeting for Couples?

Budgeting for couples means deciding how shared money responsibilities will work in real life.

That plan can include income, bills, savings, debt payments, shared goals, and personal spending, just like a simple budget for beginners. It can be as simple as a spreadsheet, a notes app, or a monthly conversation at the kitchen table.

A couple’s budget does not mean you have to combine every dollar. Some couples use one joint account for everything. Others keep separate accounts and only split shared bills. Many use a mix of both.

What matters is that both people understand how money is coming in, where it needs to go, and what each person is responsible for.

For example, one couple might put both paychecks into one joint account and pay everything from there. Another couple might keep separate accounts but each transfer money into a shared account for rent, groceries, utilities, and savings.

Both can work. The right setup is the one that feels fair and simple enough to keep using.

What You Need to Know First

Before you start building a couple’s budget, it helps to agree on a few basics.

- You do not have to combine all your money to budget together.

- Shared bills should be clear before the month begins.

- Personal spending money can make the budget feel less restrictive.

- A fair split is not always a 50/50 split.

- Short money check-ins work better than waiting until something goes wrong.

Budgeting as a couple is not about tracking every small purchase or asking permission to spend money. It is about creating enough structure so both people know what is happening.

That structure can be simple. You might decide who pays which bills, how much each person adds to savings, and how much personal spending money each person gets.

How to Start Budgeting as a Couple

Once you understand the basics, the next step is to turn those ideas into a simple money plan.

You do not need to fix everything in one conversation. Start with the biggest pieces first: income, shared bills, savings, debt, and how each person wants to handle personal spending.

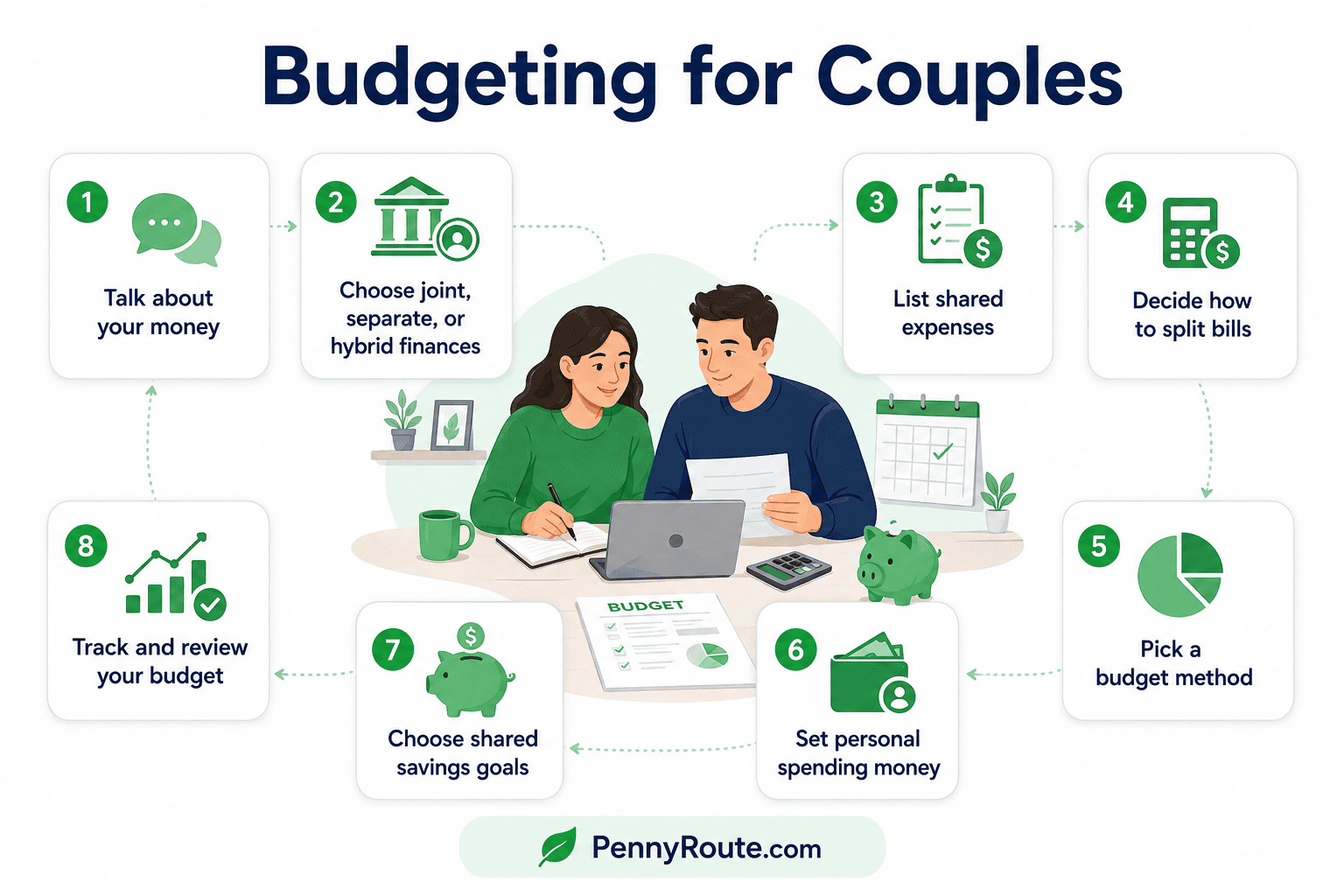

Here is how to build a couple’s budget step by step.

Step 1: Talk About Your Money Before Making the Budget

Before you choose categories or open a shared account, start with a simple money conversation.

This does not need to be formal or uncomfortable. You are just trying to understand what each person is bringing into the budget, what needs attention, and what you both want your money to do.

Talk about things like:

- Monthly income

- Rent, mortgage, utilities, and other regular bills

- Debt payments

- Savings

- Spending habits

- Upcoming expenses

- Money worries

- Short-term and long-term goals

The California Department of Financial Protection and Innovation also recommends that couples discuss income, review important financial documents, and understand each person’s financial picture before making shared money decisions.

This step matters because couples often budget from two different starting points. One person may be used to tracking every dollar, while the other may only check their balance when something feels off.

Start with facts, not blame. Look at the numbers together and agree on what needs to be handled first.

For example, if you have shared rent, credit card debt, and no emergency fund yet, those priorities should be clear before you decide how much to spend on dining out or weekend plans.

Step 2: Decide How Much Money You Want to Combine

Couples do not have to manage money the same way.

Some couples combine everything. Some keep everything separate. Others use a mix, where shared expenses come from one account, and personal spending stays separate. This is also where it helps to understand whether separate bank accounts make sense for your relationship.

The best setup depends on your relationship, income, comfort level, and how many expenses you share.

Option 1: Fully Joint Budget

With a fully joint budget, both incomes usually go into shared accounts. Bills, savings, debt payments, and everyday spending all come from the same budget.

This can work well for married couples or long-term partners who want full transparency and shared decision-making.

The downside is that it may feel too combined for couples who still want personal space with money. If you choose this setup, it is still helpful to include personal spending money for each person.

Option 2: Mostly Separate Budget

With a mostly separate budget, each person keeps their own income and accounts. You agree on how to split shared bills, but most personal spending stays separate.

This can work well for couples who are dating, newly living together, or not ready to fully combine finances.

The main challenge is making sure shared expenses are still clear. Without a system, one person may slowly end up paying more than they realize.

Option 3: Hybrid Budget

A hybrid budget gives you both teamwork and independence.

Each person keeps a personal account, but you also use a shared account or shared system for joint expenses like rent, utilities, groceries, savings goals, and household costs.

For many couples, this is the easiest place to start. It keeps shared money organized without making every purchase feel like a group decision.

For example, you might each transfer a set amount into a joint account every payday. That account covers shared bills, while personal accounts cover individual spending.

Once you know how much money you want to combine, list the expenses you both share.

These are the costs that support your household, relationship, or shared plans. Getting them out of your head and into one place makes it easier to see what each person is responsible for.

Common shared expenses may include:

- Rent or mortgage

- Utilities

- Groceries

- Internet

- Phone plans

- Insurance

- Transportation

- Childcare

- Pet costs

- Shared subscriptions

- Minimum debt payments, if the debt is shared

- Savings for shared goals

It also helps to separate shared expenses from personal expenses.

For example, groceries for the household may be shared. A personal clothing purchase, hobby, solo subscription, or coffee stop on the way to work may stay personal unless you both agree otherwise.

This does not have to be perfect from the first month. Start with the obvious shared bills, then adjust as you notice smaller expenses that should be included.

Step 4: Choose a Fair Way to Split Expenses

After you list your shared expenses, decide how each person will contribute.

This is where many couples get stuck, because “fair” does not always mean the same thing for everyone. For some couples, a 50/50 split works perfectly. For others, splitting bills based on income feels more realistic.

Here are three common ways to do it.

Split Expenses 50/50

With a 50/50 split, each person pays half of the shared expenses.

This can work well when both people earn similar incomes and have similar financial responsibilities.

For example, if your shared monthly expenses are $3,000, each person contributes $1,500.

The downside is that 50/50 can feel unfair if one person earns much more than the other or has heavier debt, childcare, or family responsibilities.

Split Expenses by Income

With an income-based split, each person contributes based on how much they earn.

For example, if one person earns 60% of the household income and the other earns 40%, you could split shared expenses 60/40.

If shared expenses are $3,000, one person contributes $1,800 and the other contributes $1,200.

This can feel fairer when incomes are different because both people are contributing in proportion to what they earn.

Split Expenses by Bill

With this method, each person takes responsibility for certain bills.

For example, one person might pay rent while the other covers groceries, utilities, and insurance.

This can be simple, but check the numbers carefully. If one person’s bills are much higher, the setup may look easy on paper but feel unfair in real life.

Whatever method you choose, write it down. A clear agreement, or one of the best apps to split bills, helps avoid the “I thought you were paying that” problem later.

Step 5: Pick a Budget Method That Works for Both of You

Once you know your shared expenses and how you will split them, choose a budget method to organize the numbers.

You do not need a complicated system. You just need a method both people understand and can keep using.

Here are a few simple options.

50/30/20 Budget

The 50/30/20 rule divides income into three broad groups: needs, wants, and savings or debt repayment.

For couples, this can be a helpful starting point because it keeps the budget flexible. You are not tracking dozens of tiny categories, but you still have a clear plan for the big areas.

This may work well if you want a simple budget without too much detail.

Zero-Based Budget

With zero-based budgeting, you give every dollar a job before the month begins.

That does not mean you spend every dollar. It means your income is assigned to bills, savings, debt, personal spending, or other categories until nothing is left unplanned.

This can work well for couples who want more control over where their money goes.

Envelope Budgeting

With envelope budgeting, you set spending limits for certain categories, such as groceries, dining out, entertainment, or personal spending.

You can use physical cash envelopes, separate bank accounts, or digital categories in a budgeting app.

This can work well if flexible spending is where your budget usually gets messy. Groceries and takeout have a talent for sneaking past the plan.

Step 6: Give Each Person Personal Spending Money

A couple’s budget should include shared responsibilities, but it should also leave room for personal choice.

Personal spending money is a set amount each person can use without needing to explain every small purchase. It can cover things like hobbies, coffee, clothes, gifts, books, games, or anything else that is just for one person.

This helps the budget feel less controlling.

For example, you might each get $200 per month for personal spending. One person may use it for lunches out, while the other saves it for a bigger purchase. As long as the amount fits the budget, both choices are fine.

This works especially well when one person is more detail-focused with money than the other. You still have shared rules for bills and savings, but not every personal purchase needs to become a budget meeting.

The amount does not have to be equal in every situation, but it should feel fair to both people. If one person’s personal spending is always protected while the other keeps cutting back, the budget will start to feel one-sided.

A couple’s budget is not just for paying bills. It should also help you plan for the things you both want or need later.

Start with the savings goals that protect your household first. For many couples, that means building an emergency fund before focusing too heavily on “nice-to-have” goals.

Shared savings goals may include:

- Emergency fund

- Vacation fund

- Car repair fund

- Home down payment

- Pet emergency fund

- Holiday spending

- Furniture or home upgrades

- Wedding costs

- Future childcare expenses

You do not need to fund every goal at once. Pick one or two priorities and add a realistic amount each month.

For example, you might decide to save $300 per month for emergencies and $100 per month for a vacation fund. You can track this in your budget or a money-saving app if that helps you both see your progress in one place.

That way, you are preparing for real life while still making room for something enjoyable.

Shared goals can also make budgeting feel more like teamwork. You are not only cutting back or tracking bills. You are building toward something together.

Step 8: Use a Simple System to Track the Budget

Once your budget is set, choose one place to track it.

This does not have to be fancy. The best system is the one both of you will actually check.

You could use:

- A shared spreadsheet

- A budgeting app

- A notes app

- A joint checking account for shared bills

- A calendar reminder for bill due dates

- A bill-splitting app for shared expenses

If one person loves spreadsheets and the other would rather fold laundry for fun, keep the system simple enough for both people. The budget should not depend on one person understanding everything while the other person stays confused.

For many couples, a hybrid system works well. You might use a joint account for shared bills, a spreadsheet for monthly planning, and an app to track smaller shared expenses.

The exact tool matters less than the habit. Pick a system, use it for a month, and adjust anything that feels too complicated.

How Often Should Couples Review Their Budget?

Most couples do not need to talk about money every day. That can make the budget feel heavier than it needs to be.

A short weekly check-in and one monthly review is enough for many couples.

The weekly check-in can be simple. Look at what has been paid, what is coming up, and whether any category is getting close to the limit.

Your monthly review can be a little bigger. Use it to check income, bills, savings goals, debt payments, and any changes coming next month.

Helpful questions to ask include:

- What went well this month?

- Did any category feel too tight?

- Are any bills changing next month?

- Did our expense split still feel fair?

- Do we need to adjust personal spending money?

- Which savings goal should we focus on next?

Keep these conversations short and practical. You are not trying to replay every purchase from the month. You are checking whether the budget still works for real life.

Example Couple Budget

Sometimes it is easier to understand a couple’s budget when you can see the numbers in one place.

Here is a simple example for a couple with a combined monthly take-home income of $5,000.

| Category | Monthly Amount |

|---|---|

| Rent | $1,500 |

| Utilities | $250 |

| Groceries | $600 |

| Transportation | $400 |

| Insurance | $250 |

| Minimum debt payments | $300 |

| Emergency fund | $300 |

| Vacation fund | $150 |

| Personal spending — Partner 1 | $250 |

| Personal spending — Partner 2 | $250 |

| Dining and entertainment | $250 |

| Miscellaneous buffer | $250 |

| Total | $5,000 |

In this example, every dollar has a place. The couple is covering bills, saving for emergencies, keeping personal spending in the budget, and leaving a small buffer for surprises.

Common Budgeting Mistakes Couples Should Avoid

Even a simple couple’s budget can get messy if the rules are unclear.

Here are a few common mistakes to watch for.

Letting One Person Handle Everything

It is fine if one person enjoys managing the spreadsheet, paying bills, or checking the app more often.

But both people should still understand the budget.

If only one person knows what is happening, the other person may feel left out, controlled, or surprised when money gets tight. A better setup is to let one person manage the details while both people review the bigger picture together.

Forgetting Personal Spending Money

A budget with no personal spending room can start to feel restrictive fast.

Even a small amount of personal spending money gives each person some freedom. It also helps avoid tiny purchases turning into bigger arguments.

You do not need to explain every coffee, book, hobby item, or lunch out if it fits within your personal spending amount.

Splitting Everything 50/50 Without Looking at Income

A 50/50 split may sound fair, but it does not work for every couple.

If one person earns much more, the lower-income partner may feel squeezed while the higher-income partner has plenty of room left over. In that case, an income-based split may be more realistic.

Fair should mean both people can cover shared expenses without one person carrying too much pressure.

Avoiding Money Conversations Until Something Goes Wrong

Money conversations are harder when they only happen after a missed payment, an overdraft, or a surprise credit card balance.

Short check-ins make budgeting less stressful because you are catching small issues early. A 15-minute conversation once a week can prevent a much bigger conversation later.

Budgeting for Newlyweds or Couples Moving in Together

If you are newly married or just starting to live together, keep the first version of your budget simple.

The first month is mostly about learning your real shared costs. Rent may be obvious, but groceries, household supplies, utilities, takeout, parking, subscriptions, and small home purchases can add up quickly.

Start by deciding:

- Which bills are shared

- Which expenses stay personal

- How much each person will contribute

- Where shared money will be kept

- How often you will review the budget

You do not have to combine everything right away. Some couples start with separate accounts and one shared account for household bills. Others combine more once they feel comfortable.

The early budget will probably need changes, and that is normal. You may realize groceries cost more than expected, one person pays more often for small items, or a bill was left out.

Treat the first few months as practice. A couple’s budget becomes easier when you give yourselves room to adjust instead of expecting the first version to be perfect.

Build a Budget You Can Both Live With

A couple’s budget does not have to be perfect from the first month.

It just needs to make shared bills clear, give both people some breathing room, and help you make money decisions before stress builds up.

Start with the expenses you already share, choose a split that feels realistic, and check in regularly. The best budget is the one both of you can understand, adjust, and actually keep using.

FAQs About Budgeting for Couples

How should couples start budgeting together?

Couples can start by listing their income, shared bills, debts, savings goals, and personal spending needs. After that, choose how you want to manage money together, such as using joint accounts, separate accounts, or a mix of both.

Should couples split bills 50/50?

A 50/50 split can work when both people earn similar incomes and have similar financial responsibilities. If one person earns much more, splitting bills by income percentage may feel fairer and more realistic.

What is the best budget method for couples?

The best budget method for couples is the one both people can understand and keep using. Many couples start with the 50/30/20 rule, zero-based budgeting, envelope budgeting, or a simple shared spreadsheet.

Should couples have joint or separate bank accounts?

Both options can work. Many couples use a hybrid setup: one shared account for bills and separate accounts for personal spending.

How often should couples talk about money?

Many couples do well with a short weekly check-in and one monthly budget review. The weekly check-in can cover upcoming bills and spending, while the monthly review can focus on savings, debt, and bigger changes.

What should be included in a couple budget?

A couple budget should include shared bills, savings goals, debt payments, personal spending money, irregular expenses, and a small buffer for surprises. It should also show how each person will contribute to shared costs.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.