When your paycheck arrives, it can already feel divided before you touch it. Bills need to be paid, groceries need room, gas or transportation costs are waiting, and somehow you are still supposed to save something.

A common target is to save 10% to 20% of each paycheck, but that number does not fit every budget. For some people, saving $25 consistently is more useful than trying to save 20% once and moving it back two days later.

A better starting point is a paycheck savings amount that protects your future without putting this week’s bills at risk.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

Quick Overview: How Much Should You Save From Each Paycheck?

- A common target is to save 10% to 20% of each paycheck, but that range may not fit every budget.

- If percentages feel too high, start with a fixed amount such as $10, $25, or $50 per paycheck.

- Save after must-pay bills are accounted for, so savings does not create overdrafts or missed payments.

- A fixed amount can work better than a percentage if your income is tight or irregular.

- Weekly, biweekly, and monthly paychecks may need different savings timing.

- Your first paycheck savings target may be a small checking buffer or starter emergency fund.

How Much Should You Save From Each Paycheck?

A common starting point is to save 10% to 20% of each paycheck, but the right number depends on your bills, debt, income, and how much cash you need to keep your checking account stable.

Fidelity’s budgeting guideline uses 10% for near-term goals and emergency savings, while treating retirement savings as a separate long-term category.

If 20% works for your budget, it can help you build savings faster. If it does not, start lower. Saving 5%, 3%, or a fixed amount like $10 or $25 is still useful when you can repeat it without pulling the money back.

Here is what different savings percentages look like:

| Paycheck amount | 5% savings | 10% savings | 20% savings |

|---|---|---|---|

| $500 | $25 | $50 | $100 |

| $1,000 | $50 | $100 | $200 |

| $1,500 | $75 | $150 | $300 |

| $2,000 | $100 | $200 | $400 |

For example, saving $200 from a $1,000 paycheck may sound ideal, but it is not helpful if it leaves you short on rent, groceries, gas, or minimum debt payments. In that case, $50 or even $25 may be the better first step.

The amount you choose should be small enough to stay saved, but meaningful enough to move you forward. That balance matters more than matching a perfect percentage.

Percentage or Fixed Amount: Which Works Better?

Once you know the general savings range, the next decision is how to set the amount. You can save a percentage, a fixed dollar amount, or a flexible amount based on each paycheck.

Use a Percentage If Your Paycheck Is Steady

A percentage works well when your income is predictable. For example, if you decide to save 10% and your paycheck is usually $1,200, you would move about $120 each time you get paid.

This method adjusts naturally if your paycheck changes a little, but it still gives you a clear rule to follow.

Use a Fixed Amount If Your Budget Is Tight

A fixed amount may work better if your budget needs more control. Instead of saving 10% every time, you might save $10, $25, or $50 from each paycheck.

This can feel easier because you know exactly how much is leaving checking. It also reduces the chance of moving too much too soon.

Use a Flexible Amount If Your Income Changes

If your income changes from week to week, try setting a minimum amount and saving extra when the paycheck is larger.

For example, you might save $10 from every paycheck, then add more when you get overtime, tips, a bonus, a refund, or an extra shift.

This keeps the savings habit alive without forcing the same amount during a lower-pay period.

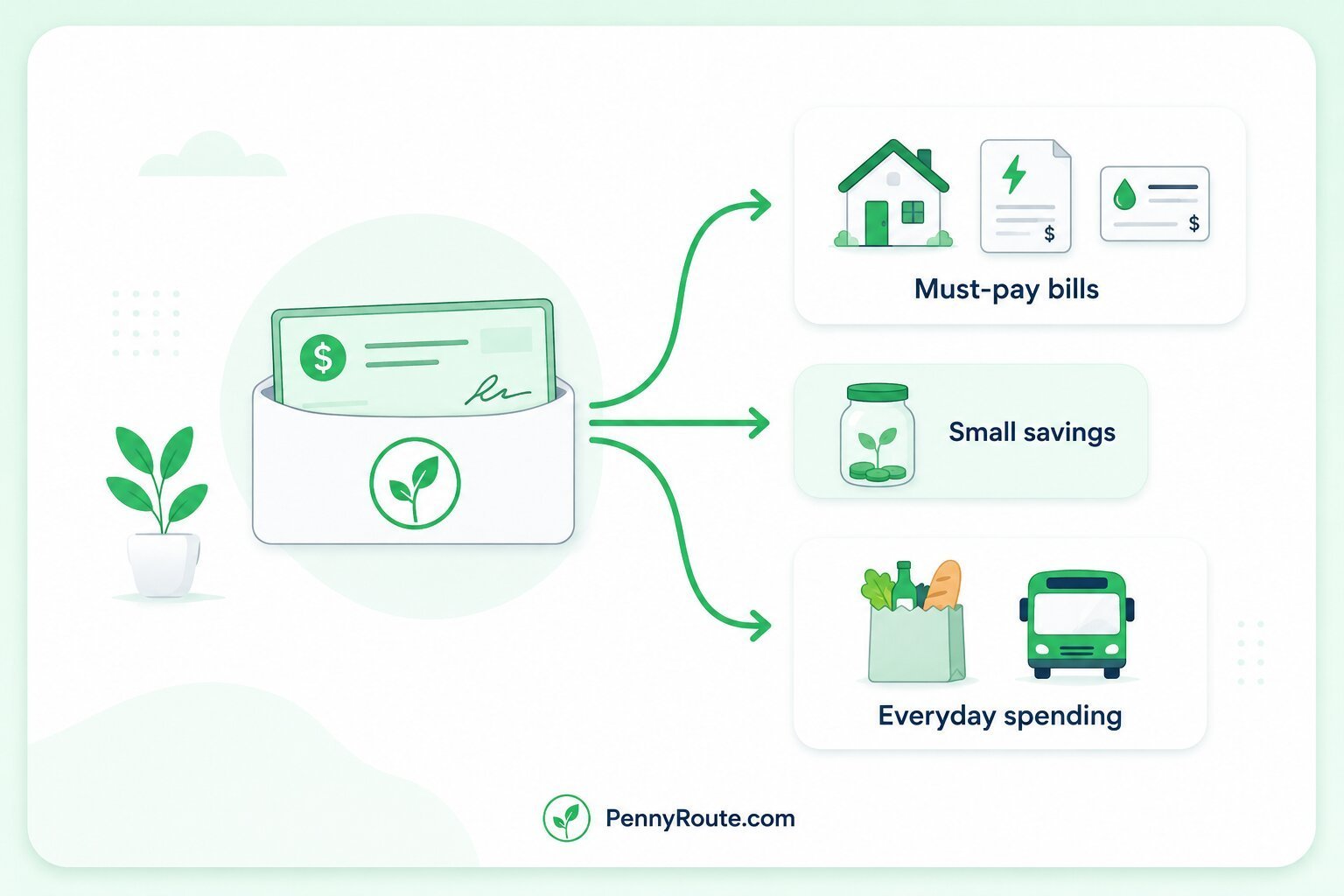

Save After Must-Pay Bills, Not After Random Spending

Paycheck savings works best when you know which bills need to be protected first. Otherwise, it is easy to move money into savings, feel productive for a day, and then pull it back when rent, groceries, or transportation costs hit.

Start by setting aside money for must-pay expenses, such as:

- Housing

- Utilities

- Groceries

- Transportation

- Insurance

- Minimum debt payments

- Childcare or caregiving costs

- Basic medical costs

After those essentials are accounted for, you can see what is actually available for savings, extra debt payments, short-term goals, and flexible spending.

This is where a simple beginner budget can help. It does not need to be complicated. You are just checking whether your paycheck can cover the bills that must be paid before you move money somewhere else.

It also helps to keep a small checking buffer, especially if bills come out a few days after payday. Deciding how much money to keep in checking can prevent a savings transfer from turning into an overdraft fee or a credit card charge.

Saving before random spending is helpful. Saving before necessary bills are covered can create new stress.

How to Save From Weekly, Biweekly, or Monthly Paychecks

How often you get paid changes how savings should fit into your cash flow. The right amount is not only about the paycheck size. It also depends on when your bills are due.

If You Get Paid Weekly

Weekly paychecks work well with small, repeatable savings amounts because you have more chances to save during the month.

For example, saving $10 each week adds up to about $520 in a year. Saving $25 each week adds up to about $1,300 in a year.

The main thing to watch is bill timing. If rent, insurance, or a large payment comes from one specific paycheck, that week may need a smaller savings transfer than the others.

If You Get Paid Biweekly

Biweekly paychecks usually mean 26 paychecks per year. If you save $50 from each paycheck, that adds up to $1,300 in a year. If you save $100 from each paycheck, that adds up to $2,600.

This schedule can work well because most months have two paychecks, but two months of the year may have three. Those extra-paycheck months can be useful for savings, annual bills, debt payments, or a starter emergency fund.

Just be careful not to base every monthly bill on a “two-paycheck” plan if your bills are uneven. Some paychecks may need to cover more than others.

If You Get Paid Monthly

Monthly paychecks need more planning because one deposit may need to cover several weeks of bills and spending.

Before moving money to savings, map out the bills that will come due before your next paycheck. Then choose a savings amount that leaves enough in checking for groceries, transportation, utilities, subscriptions, and any automatic payments.

A monthly paycheck can still support savings, but the transfer may need to happen after you know the month’s bill timing. For some people, splitting savings into two smaller transfers during the month feels safer than moving one larger amount right away.

What If You Can Only Save a Small Amount?

Saving a small amount from each paycheck is still worth doing if it helps you build consistency.

A $5, $10, or $25 transfer may not look impressive at first, but it gives your money a direction. It can help you build the first $100, avoid one overdraft fee, cover a small surprise expense, or start a starter emergency fund without putting too much pressure on your budget.

Small savings can also make the habit feel less intimidating. Once the amount becomes normal, you can raise it slowly when something changes, such as a bill dropping, a debt payment ending, income increasing, or a higher-cost habit becoming easier to reduce.

If your paycheck is already stretched, saving money on a low income may start with finding one small gap instead of forcing a percentage that does not fit. A repeatable amount is usually better than a larger transfer that keeps coming back out of savings.

Should You Automate Paycheck Savings?

Automatic savings can be helpful when your income and bills are predictable. It removes one decision from payday and makes saving happen before the money gets absorbed by everyday spending.

But automation is not always the safest choice for every budget.

If your checking balance often gets low, or if bills hit at different times each month, a fixed automatic transfer could create overdraft risk. In that case, manual transfers may work better until your cash flow feels steadier.

A safer approach is to start small and time the transfer carefully. For example, you might schedule $10 or $25 to move to savings the day after payday, once you know the paycheck arrived and your most urgent bills are covered.

You can also use automation for part of your savings and move extra money manually when the paycheck is larger than usual. That gives you structure without locking yourself into an amount that may not fit every pay period.

Automation should make saving easier, not create another bill your checking account has to survive.

Where Should Your Paycheck Savings Go First?

Once you decide how much to save from each paycheck, the next question is where that money should go. The answer depends on what your savings needs to protect first.

Start With a Checking Buffer

A checking buffer is extra money left in your checking account after bills and regular spending are planned. It helps cover timing issues, small mistakes, and automatic payments that hit earlier than expected.

This does not need to be large at first. Even $50 or $100 can help reduce the risk of overdraft fees or last-minute credit card use.

Build a Starter Emergency Fund

After your checking account has a little breathing room, a starter emergency fund is often the next useful target.

This is the money you keep for expenses that are urgent, unexpected, or hard to delay, such as a car repair, medical bill, home repair, or temporary income gap.

You might start with $100, then $250, then $500, then one month of essential expenses. The first milestone matters because it gives surprise expenses somewhere to land besides your credit card or checking account.

Separate Short-Term Goals

Some expenses are not emergencies, but they can still surprise your budget if you do not plan for them. Car maintenance, annual subscriptions, school costs, holidays, insurance deductibles, moving costs, and basic home repairs are good examples.

Paycheck savings can help you build small buckets for these costs over time. You do not need a separate account for every single category, but deciding how many bank accounts you need can make it easier to keep emergency money separate from planned expenses.

Keep Retirement Savings Separate

Retirement savings is usually different from paycheck cash savings. Money for emergencies, bills, and short-term goals should stay accessible. Retirement contributions are usually meant for long-term growth and may have rules, taxes, or penalties if withdrawn early.

If your employer offers retirement benefits, that may be part of your bigger savings picture. It should not replace a basic cash cushion for everyday life.

For a wider benchmark beyond payday savings, savings by age can help you compare cash savings, emergency savings, and long-term savings goals without mixing them into one number.

A Simple Paycheck Savings Plan

Once you know your paycheck amount, bill timing, and savings target, keep the plan simple enough to repeat.

Start with one amount you can safely move each payday. That might be 10%, 5%, $25, or $10. The right starting number is the one that can stay in savings without causing missed bills, overdrafts, or another transfer back to checking.

Next, choose where the money should go first. For many beginners, that may be a small checking buffer, a starter emergency fund, or one short-term savings goal like car repairs, annual bills, or moving costs.

After two or three paychecks, review what happened. If you kept pulling the money back, lower the amount or change the timing. If the transfer stayed put, consider increasing it slowly.

A paycheck savings plan does not need to be impressive. It needs to be repeatable. When the amount, timing, and purpose fit your real budget, saving becomes easier to keep going.

FAQs About Saving From Each Paycheck

How much of my paycheck should I save?

A common target is 10% to 20% of each paycheck, but the right amount depends on your bills, debt, income, and emergency fund. If that range feels too high, start with a smaller fixed amount you can repeat.

Is saving 10% of each paycheck enough?

Yes, saving 10% can be a strong starting point if it fits your budget. Consistently saving 10% is often more useful than trying to save 20% and needing to move the money back into checking.

Should I save 20% of every paycheck?

Saving 20% is a helpful target for some budgets, but it is not realistic for everyone. If 20% would cause missed bills, overdrafts, or credit card use for basics, start with a lower amount and increase it later.

How much should I save from a $1,000 paycheck?

From a $1,000 paycheck, 10% would be $100 and 20% would be $200. If that feels too high, a fixed amount like $25 or $50 may be a better starting point.

Should I save before or after paying bills?

Save after you know your must-pay bills are covered, but before random spending absorbs the rest. This keeps savings intentional without putting rent, groceries, utilities, or transportation at risk.

What if I cannot save from every paycheck?

Save when you safely can. You can also build progress by avoiding one fee, lowering one bill, saving extra from a larger paycheck, or restarting with a smaller amount next payday.

Is it better to save weekly or monthly?

The better schedule is the one that matches your pay cycle and bill timing. Weekly savings may work well for weekly paychecks, while monthly savings may need more planning so bills are covered first.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.