Managing your money can get confusing when every dollar sits in one place. Bills, everyday spending, emergency savings, and short-term goals can all mix together, making it harder to know what is actually safe to spend.

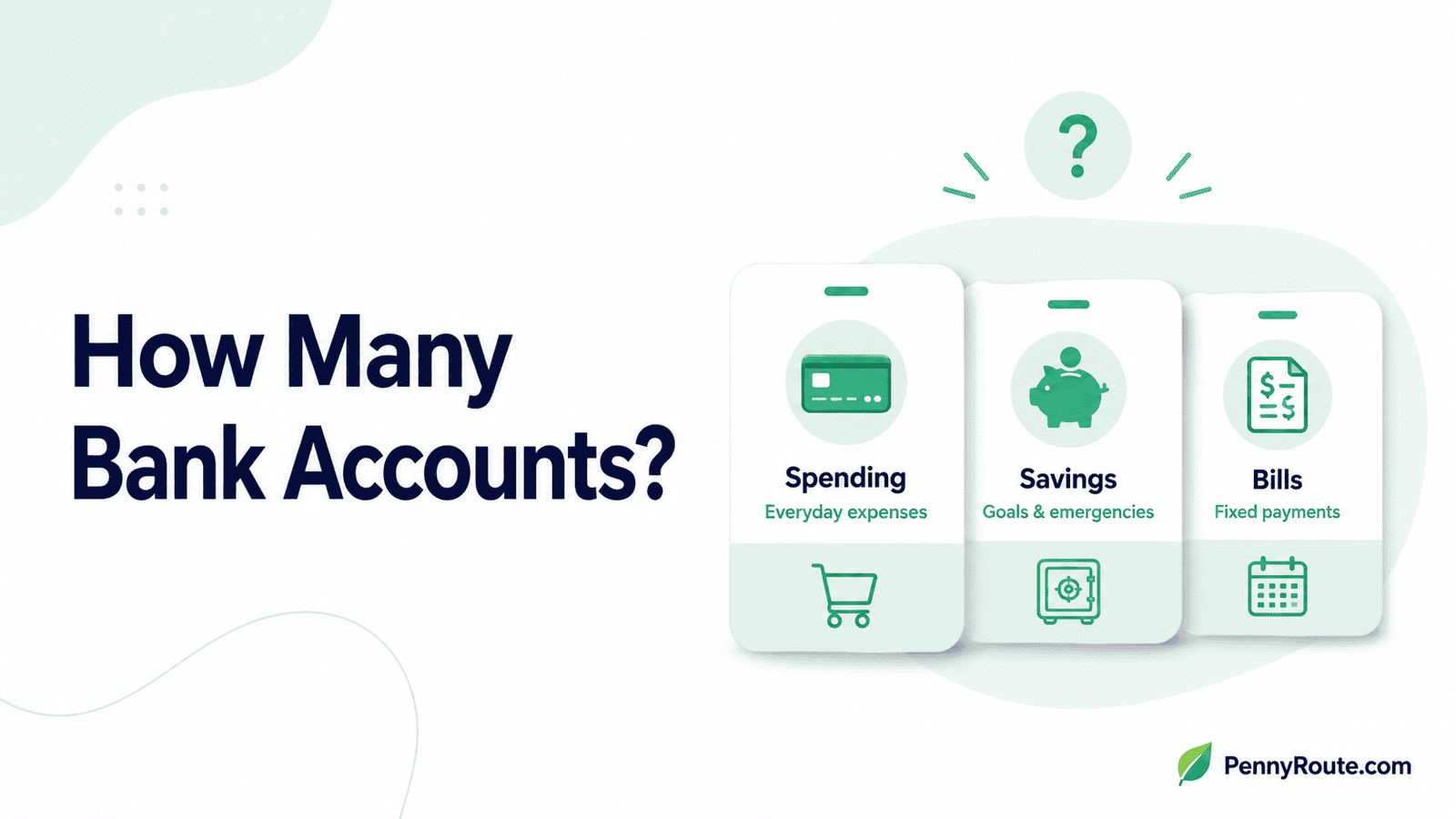

So, how many bank accounts should you have? For many people, a simple setup starts with two accounts: one checking account for daily money and one savings account for emergencies or goals. But the right number depends on how you manage bills, savings, shared expenses, and whether extra accounts make your money easier—or harder—to track.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

How Many Bank Accounts Should You Have?

For most people, a good starting point is two bank accounts: one checking account for everyday spending and bills, and one savings account for emergencies or short-term goals.

From there, you may add more accounts if they solve a clear problem. For example, a separate savings account can help you keep your emergency fund away from vacation money. A separate bills account can help you avoid spending money that is already needed for rent, utilities, or subscriptions.

The best number of bank accounts is not the highest number. It is the number that helps you stay organized without making your money harder to manage.

Simple Setup That Works for Most People

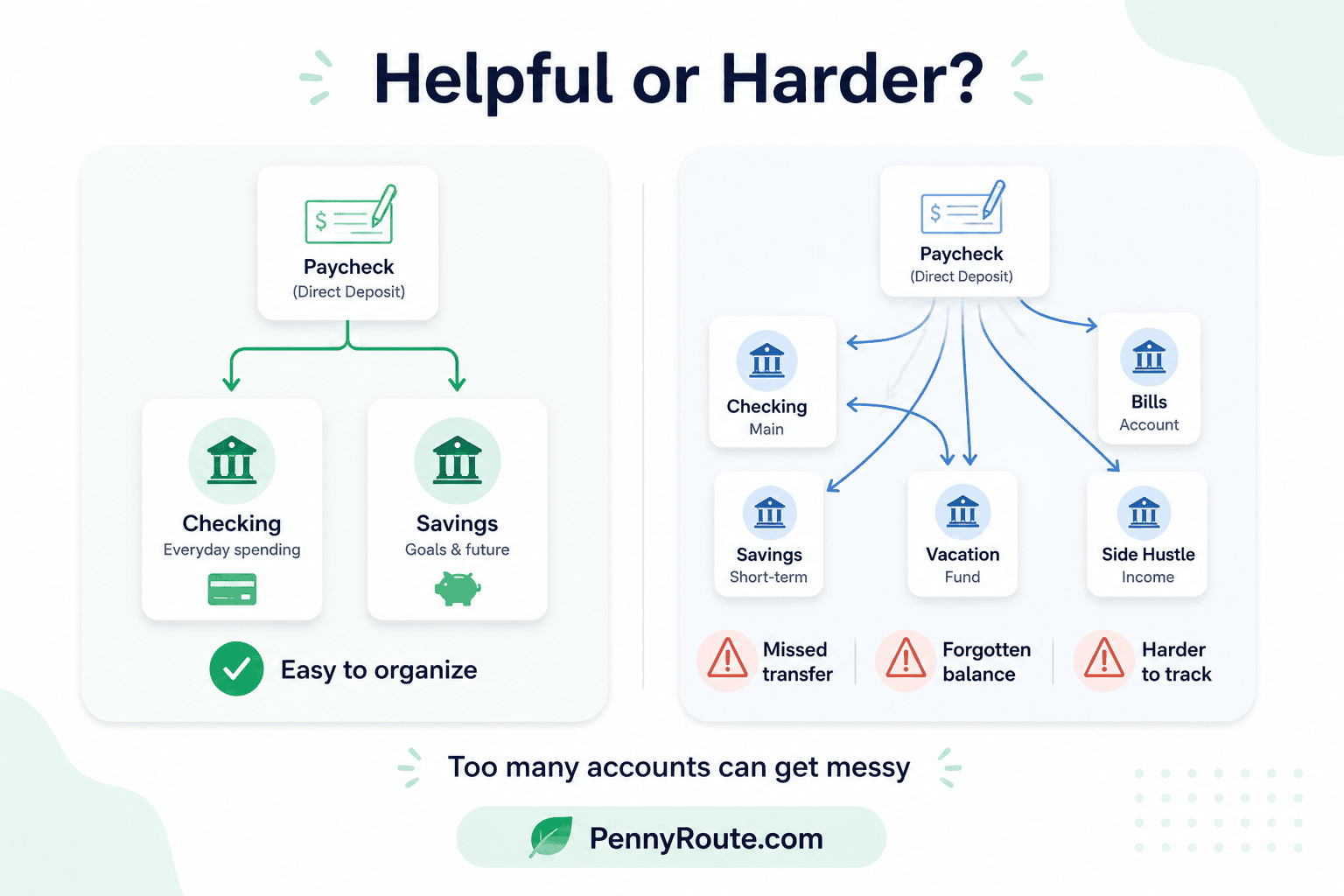

A basic setup with one checking account and one savings account works well for most situations. It keeps things easy to manage while giving your money a clear structure.

Your checking account is where your income goes. You use it to pay bills, cover everyday spending, and handle regular expenses.

Your savings account is where you set money aside. This can be for an emergency fund or short-term goals like a trip, a new device, or upcoming expenses.

Here’s how it might look in real life:

If you earn $3,000 a month, your paycheck goes into your checking account. From there, you pay your rent, groceries, and other bills. Then you move a portion, even $100 or $200, into your savings account.

This simple split helps you avoid spending everything in one place. It also makes your progress easier to see, even if you’re starting small.

When It Makes Sense to Have More Than Two Accounts

Adding more accounts can help, but only when each one has a clear purpose. The goal is to make your money easier to manage, not to create extra work.

To Separate Bills and Spending

Using two checking accounts can make day-to-day money decisions easier. One account is only for bills, and the other is for everyday spending.

For example, if your monthly bills are $1,800, you can keep that amount in one account. The rest stays in your spending account. This way, you don’t accidentally use bill money for something else.

To Save for Multiple Goals

One savings account works, but it can feel unclear when you’re saving for different things at the same time.

You might keep separate savings accounts for:

- Emergency fund

- Travel

- A large purchase

If you save $300 a month, you could split it into $150 for emergencies, $100 for travel, and $50 for a future purchase. Seeing each goal separately can make it easier to stay consistent.

If you share expenses with a partner or family member, a separate account can simplify things.

For example, both of you might contribute $500 each month into a shared account for rent, groceries, and utilities. This keeps shared spending separate from personal money.

To Handle Side Income or Freelancing

If your income changes month to month, having a separate account for it can help you stay organized.

For example, if you earn $800 from freelance work, you can keep it in a separate account and move a set amount into your main account each month. This creates more stability, even when income is uneven.

When each account has a clear role, managing your money starts to feel more predictable.

| Situation | Recommended Setup |

|---|---|

| Just starting out | 1 checking + 1 savings |

| Need better spending control | 2 checking + 1 savings |

| Irregular income | 1 income + 1 bills + 1 savings |

When More Bank Accounts Can Make Things Harder

More accounts can help with organization, but they can also create problems if things get too spread out.

One issue is fees or minimum balance requirements. Some accounts charge a monthly fee if your balance drops below a certain amount. If your money is divided across multiple accounts, it becomes easier to fall below those limits without noticing.

It can also get harder to keep track of where your money is. When you’re managing several balances, transfers, and due dates, small mistakes can happen. You might forget to move money before a bill is due or lose track of how much you actually have available to spend.

Another risk is overdrafts. If one account runs low while money is sitting in another, you could end up paying a fee even though you have enough money overall.

More accounts also mean more to manage. Extra logins, more alerts, and more decisions about where your money should go. If the setup feels confusing, it usually isn’t helping.

When your accounts start creating friction instead of clarity, it’s a sign that the setup may be more than you need.

More accounts can help, but only if each one has a clear purpose and you check in regularly.

It’s also worth knowing how deposit protection works. FDIC insurance covers up to $250,000 per person, per bank, based on how the account is owned. Opening multiple accounts at the same bank doesn’t increase that coverage.

How Many Bank Accounts You May Need by Situation

The right number of bank accounts depends on how simple or complicated your money setup is. A beginner may only need two accounts, while someone with shared bills, irregular income, or multiple savings goals may need a few more.

Here is a simple way to think about it:

| Your situation | Bank account setup that may work |

|---|---|

| You are just starting out | 1 checking account + 1 savings account |

| You live paycheck to paycheck | 1 checking account + 1 small emergency savings account |

| You want to separate bills from spending | 1 checking account for spending + 1 bills account + 1 savings account |

| You are saving for multiple goals | 1 checking account + separate savings accounts for each major goal |

| You are building an emergency fund | 1 checking account + 1 dedicated emergency savings account |

| You are part of a couple managing shared expenses | Personal accounts + 1 shared account for joint bills |

| You are self-employed or have side income | Personal checking + savings for taxes + emergency savings |

| You have several accounts already and feel confused | Fewer accounts may work better until your setup feels manageable |

Think of each account as having a job. One account may be for bills, another for savings, and another for daily spending. If an account does not have a clear purpose, it may add more confusion than help.

A good setup should make your money easier to understand at a glance. You should be able to see what is available to spend, what needs to stay untouched, and what is already set aside for future expenses.

Should Your Accounts Be at the Same Bank or Different Banks?

You can manage your accounts at the same bank or across different banks. Both approaches work. It depends on what feels easier for you.

Keeping everything at the same bank makes things simple. You can move money quickly between accounts, track everything in one place, and avoid delays when transferring funds. This setup works well if you want convenience and fewer steps.

Using different banks can give you more control in some cases. You might find better savings rates, or you may prefer keeping your savings separate so it’s not as easy to spend. For some people, that extra separation helps build consistency.

There’s no right or wrong choice here. What matters is choosing a setup that you can manage easily without missing transfers or losing track of your balance.

How Many Bank Accounts Is Too Many?

There isn’t a strict limit, but it becomes too many when your setup starts working against you.

If you’re having trouble remembering balances, missing transfers, or moving money around just to avoid fees, your system may be more complex than it needs to be.

For example, if you have four or five accounts but still feel unsure about how much you can spend, the extra accounts aren’t helping. They’re adding friction instead of clarity.

A good setup should feel easy to follow. You should know where your money is, what it’s for, and how much is available without checking multiple apps or doing mental math.

When things start to feel scattered, simplifying your accounts can make everything easier to manage.

Questions You Might Still Have

Is it bad to have multiple bank accounts?

No, having multiple bank accounts is not bad. It can actually help you stay organized if each account has a clear purpose.

Can you have multiple checking accounts?

Yes, you can have more than one checking account, even at the same bank. Many people use this setup to separate bills and everyday spending.

How many savings accounts should you have?

One savings account is enough to start. You can add more if you’re saving for different goals and want to keep them separate.

Is it better to keep checking and savings at the same bank?

Keeping both at the same bank is usually easier because transfers are faster and everything is in one place. Using different banks can help if you want better savings rates or more separation between spending and saving.

Can couples have separate bank accounts?

Yes, couples can have separate bank accounts, joint accounts, or a mix of both.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.