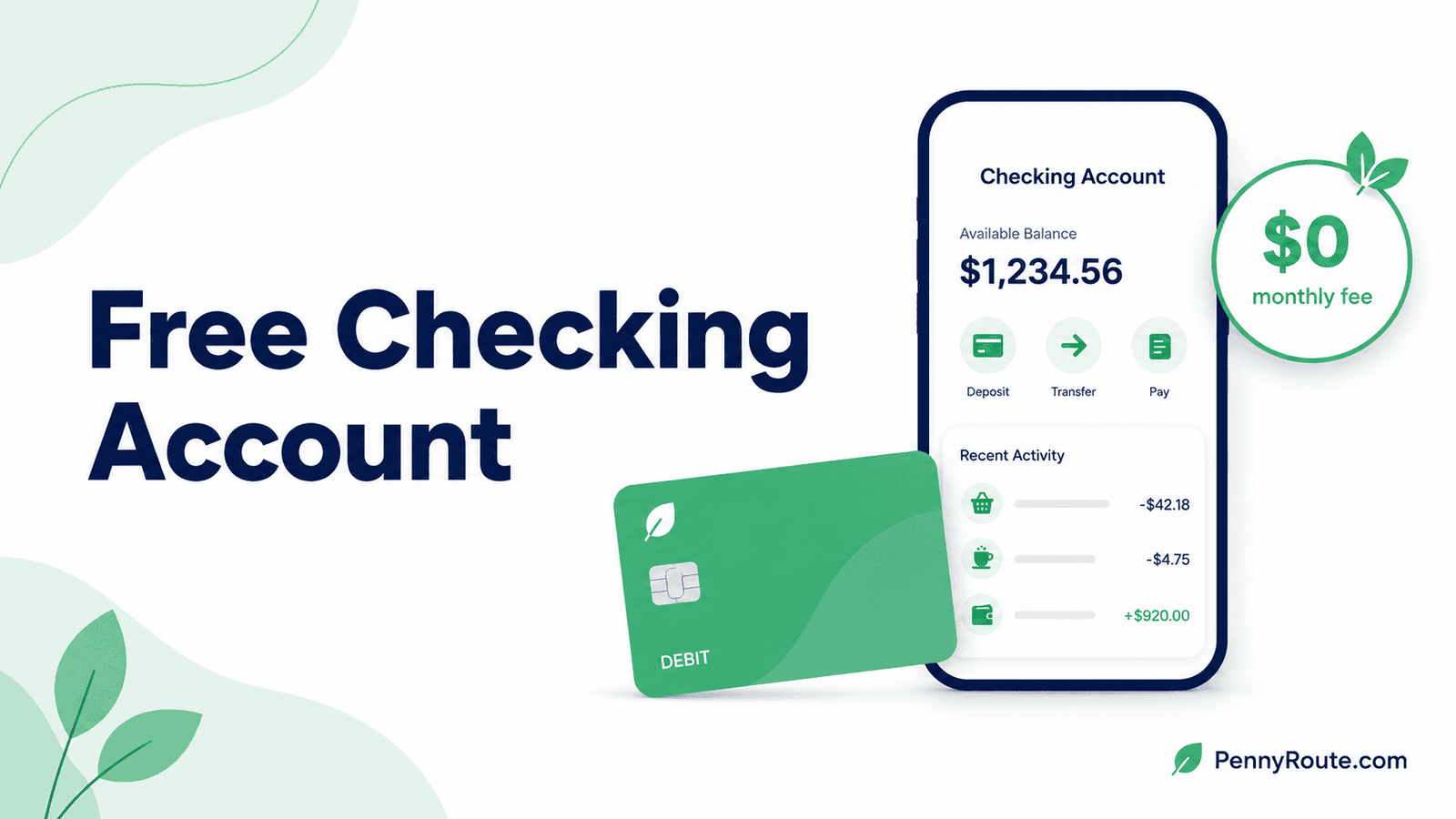

A free checking account sounds simple: you open the account, use it for everyday money, and avoid the monthly fee.

But “free” can mean different things depending on the bank or credit union. Some accounts are simple and low-cost. Others remove one fee but still charge for certain services. That is why it helps to look past the label and understand how the account works in real life.

A good free checking account should help you receive income, pay bills, use your debit card, access cash, and manage everyday money without making basic banking more expensive than it needs to be.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

What Is a Free Checking Account?

A free checking account is usually one with no monthly maintenance fee or a fee that is easy to avoid.

You can use it like a regular checking account for everyday money tasks, such as receiving direct deposit, paying bills, using a debit card, withdrawing cash, sending transfers, and managing spending through online or mobile banking.

The important part is understanding what “free” applies to. In most cases, it means you are not paying a monthly fee just to keep the account open.

It does not always mean the account has no fees at all. A free checking account may still charge for certain transactions, account services, or optional features.

What Does “Free Checking” Really Mean?

Free checking usually means the account does not charge a monthly maintenance fee.

That monthly fee is the regular charge some banks apply just for keeping a checking account open. If an account has no monthly maintenance fee, you are not paying the bank every month simply to use the account.

Some accounts are free with no extra steps. Others may only stay free if you meet certain conditions, such as setting up direct deposit, keeping a small minimum balance, choosing electronic statements, or meeting student or age requirements.

You may also see terms like “no monthly fee checking,” “no-fee checking,” or “no maintenance fee checking.” These sound similar, but banks may use them differently.

The account name matters less than the details. Before opening one, check whether the account is truly free every month or only free if you follow certain requirements.

What Fees Can Still Apply to a Free Checking Account?

A free checking account can remove the monthly maintenance fee, but other fees may still apply.

This is where many people get caught off guard. The account may be free to keep open, but not free for every transaction, mistake, or extra service.

Here are common fees to check before opening one.

Out-of-network ATM fees

If you use an ATM outside your bank’s network, you may pay a fee.

Sometimes the ATM owner charges a fee, and your own bank may charge another fee on top of that. If you use cash often, make sure there are free ATMs near your home, work, school, or regular errands.

Overdraft fees

An overdraft can happen when more money leaves your checking account than you have available.

Depending on the account and your settings, the bank may decline the transaction, cover it and charge a fee, or pull money from a linked account. Even with free checking, overdraft fees can be expensive if you are not careful.

Non-sufficient funds fees

A non-sufficient funds fee, sometimes called an NSF fee, can happen when a payment is returned because there is not enough money in your account.

For example, if an automatic bill payment tries to go through and your account cannot cover it, the bank may return the payment and charge a fee.

Paper statement fees

Some banks charge a fee if you choose mailed paper statements instead of electronic statements.

This may be easy to avoid if you are comfortable using online banking, but it is still worth checking.

Wire transfer fees

Wire transfers are often used to send money quickly, especially for larger or more formal payments.

A free checking account may still charge for incoming or outgoing wire transfers, and international wires can cost more.

Stop payment fees

A stop payment fee may apply if you ask the bank to block a check or certain payment before it goes through.

This can be useful in specific situations, but it is usually not free.

Replacement debit card fees

Some banks replace a debit card for free, while others may charge for replacement cards or rushed delivery.

This matters if your card is lost, damaged, or stolen and you need a new one quickly.

Foreign transaction fees

Foreign transaction fees can apply when you use your debit card outside your home country or buy from certain international merchants.

If you travel or shop from global websites, check this fee before choosing the account.

Free Checking vs Regular Checking

A free checking account is still a regular checking account in the sense that you can use it for everyday banking. The main difference is usually the monthly fee.

A regular checking account may charge a monthly maintenance fee unless you meet certain waiver rules. A free checking account usually removes that fee or makes it easier to avoid.

| Feature | Free Checking Account | Regular Checking Account |

|---|---|---|

| Monthly maintenance fee | Usually none | May apply |

| Fee waiver rules | Often not needed, or easier to meet | May require direct deposit, minimum balance, or activity |

| Everyday banking | Usually included | Usually included |

| Debit card access | Usually included | Usually included |

| Best for | Avoiding regular monthly fees | People who need certain features or branch benefits |

| Watch for | Other service fees | Monthly fees, balance rules, and service fees |

A free checking account can be a good fit if you want simple, low-cost everyday banking. A regular checking account may still make sense if it offers features you actually use and the monthly fee is easy for you to avoid.

Who Is a Free Checking Account Best For?

A free checking account can be a good fit if you want a simple way to manage everyday money without paying a monthly maintenance fee.

It may work well for:

- Beginners opening one of their first checking accounts

- Students or young adults managing basic expenses

- People who want to avoid monthly account fees

- Anyone with a lower or changing checking balance

- People who mainly need debit card access, direct deposit, bill pay, and transfers

- Someone who does not want to keep extra money in checking just to avoid a fee

For example, if your balance changes a lot during the month after rent, groceries, bills, and savings transfers, a free checking account with no minimum balance requirement may feel easier to manage.

It can be especially helpful if your balance changes during the month and you do not want to keep extra money in checking just to avoid a fee.

When a Free Checking Account May Not Be Enough

A free checking account can be helpful, but it is not automatically the best choice for every situation.

It may not be enough if the account saves you from a monthly fee but makes other parts of banking harder.

For example, a free checking account may not be the best fit if:

- You deposit cash often, but the bank has limited cash deposit options

- You need regular in-person branch support

- Free ATMs are not easy to access near you

- The mobile app is hard to use or unreliable

- Customer support is limited

- Overdraft rules are unclear

- You need extra services, such as frequent wire transfers or cashier’s checks

- The account has limits that do not match how you use money

Free checking is useful when it removes costs without adding friction elsewhere. If avoiding a monthly fee means dealing with poor access, confusing rules, or services you cannot easily use, another checking account may be a better fit.

Questions to Ask Before Choosing a Free Checking Account

Before opening a free checking account, look beyond the “free” label and check how the account works in real life.

Ask these questions first:

- Is there truly no monthly maintenance fee?

- Do I need direct deposit to keep the account free?

- Is there a minimum balance requirement?

- Are free ATMs easy to access near me?

- Can I deposit cash if I need to?

- What happens if I overdraft?

- Are low-balance alerts available?

- Are paper statements free, or do I need e-statements?

- Does the account support direct deposit, bill pay, transfers, and debit card use?

- Can I reach customer support easily?

- Are there account closing fees or other less obvious charges?

This quick check can help you separate a truly useful free checking account from one that only looks good at first glance.

Is a Free Checking Account Safe?

A free checking account can be safe if it is offered by a properly insured bank or credit union.

In the U.S., checking accounts at FDIC-insured banks are generally protected by FDIC deposit insurance. Federally insured credit unions are protected by NCUA insurance. This protection matters if the bank or credit union fails.

The word “free” does not make an account unsafe by itself. A free checking account can be just as safe as a regular checking account if the institution is legitimate, insured, and transparent about its terms.

Before opening one, check:

- Whether the bank is FDIC-insured

- Whether the credit union is NCUA-insured

- Whether a financial app clearly states which insured bank holds your money

- Whether the account terms, fees, and limits are easy to find

- Whether the app or website uses secure login options

A free checking account should save you money on monthly fees, but it should still be held at a bank or credit union you can verify and trust.

The Simple Way to Think About Free Checking

A free checking account can be a smart choice when it lowers your regular banking costs without making everyday money harder to manage.

Before choosing one, look past the word “free” and check the details that affect you most: ATM access, overdraft rules, cash deposits, mobile banking, and customer support.

If the account is easy to use, properly insured, and does not charge for the things you normally need, it may be a good fit. The best free checking account is not the one with the biggest promise. It is the one that stays simple after you open it.

FAQs About Free Checking Accounts

Is a free checking account really free?

A free checking account usually means there is no monthly maintenance fee. Other fees may still apply, such as overdraft fees, out-of-network ATM fees, wire transfer fees, paper statement fees, or foreign transaction fees.

What is the difference between free checking and no-fee checking?

The terms are often used loosely. Free checking usually means no monthly fee, while no-fee checking may suggest fewer fees overall. Either way, the fee schedule matters more than the name.

Can a free checking account charge overdraft fees?

Yes. A free checking account can still charge overdraft fees unless the account specifically does not offer overdraft fees or declines transactions that would overdraw the account.

Do free checking accounts require a minimum balance?

Some do, but many do not. Check whether the account requires a minimum opening deposit, minimum daily balance, or average monthly balance to avoid fees or keep certain benefits.

Is free checking good for beginners?

Yes, it can be. A free checking account can be a good beginner option if it has no monthly fee, simple mobile banking, easy ATM access, clear overdraft settings, and basic features like direct deposit and bill pay.

Is free online checking safe?

Free online checking can be safe when the account is offered by an insured bank or credit union and you protect your login details. Always check where your money is held, especially when using a newer financial app.

Can I get direct deposit with a free checking account?

Usually, yes. Many free checking accounts support direct deposit, but features can vary by bank or credit union.

Can I pay bills with a free checking account?

Usually, yes. Many free checking accounts support bill pay, debit card payments, automatic payments, and transfers. Check the account details before opening one so you know which payment features are included.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.