Can you have two checking accounts at the same bank? In most cases, yes. Many banks let customers open more than one checking account, especially when each account has a different purpose.

A second checking account can help you separate money for bills, spending, side income, subscriptions, or backup access. But opening another account is not automatically better. You still need to check the rules, fees, and setup so the extra account actually makes your money easier to manage.

Used well, two checking accounts can make everyday banking simpler. Used without a plan, they can create more balances, more transactions, and more chances to miss something.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

Quick Overview: Two Checking Accounts at the Same Bank

- You can usually have two checking accounts at the same bank, but approval depends on the bank’s rules.

- There is no federal rule limiting you to one checking account.

- A second account can help organize bills, spending, side income, subscriptions, or backup money.

- Check monthly fees, minimum balance rules, debit card access, and overdraft settings before opening one.

- Two checking accounts at the same bank do not usually double FDIC insurance coverage.

Can You Have Two Checking Accounts at the Same Bank?

Yes, you can usually have two checking accounts at the same bank. There is no federal rule that says you can only have one checking account.

The Consumer Financial Protection Bureau explains that there are no restrictions on how many checking or savings accounts you can open, or how many banks and credit unions you can use. That means the legal side is usually not the issue. Your bank’s account policies matter more.

A bank may still ask you to apply for the second account, choose from its available checking products, and meet any account requirements. Some accounts may also have monthly fees, opening deposit rules, or balance requirements.

So the practical answer is simple: two checking accounts are usually allowed, but the second account should be worth the extra setup.

How Two Checking Accounts at the Same Bank Work

When you open a second checking account at the same bank, it usually works as a separate account under your existing online banking profile.

Each checking account may have its own account number, balance, transaction history, monthly fee rules, and debit card access. Depending on the bank, you may be able to see both accounts in the same app and move money between them quickly.

For example, your paycheck could go into your main checking account first. Then you could transfer a set amount to a second checking account for weekly spending, subscriptions, or another specific purpose.

The important part is that the accounts are separate. Money sitting in one checking account may not automatically cover payments coming out of the other unless you have overdraft transfers or linked-account protection set up.

That is why a second checking account works best when each account has a clear job. If both accounts are used for everything, the setup can become confusing instead of helpful.

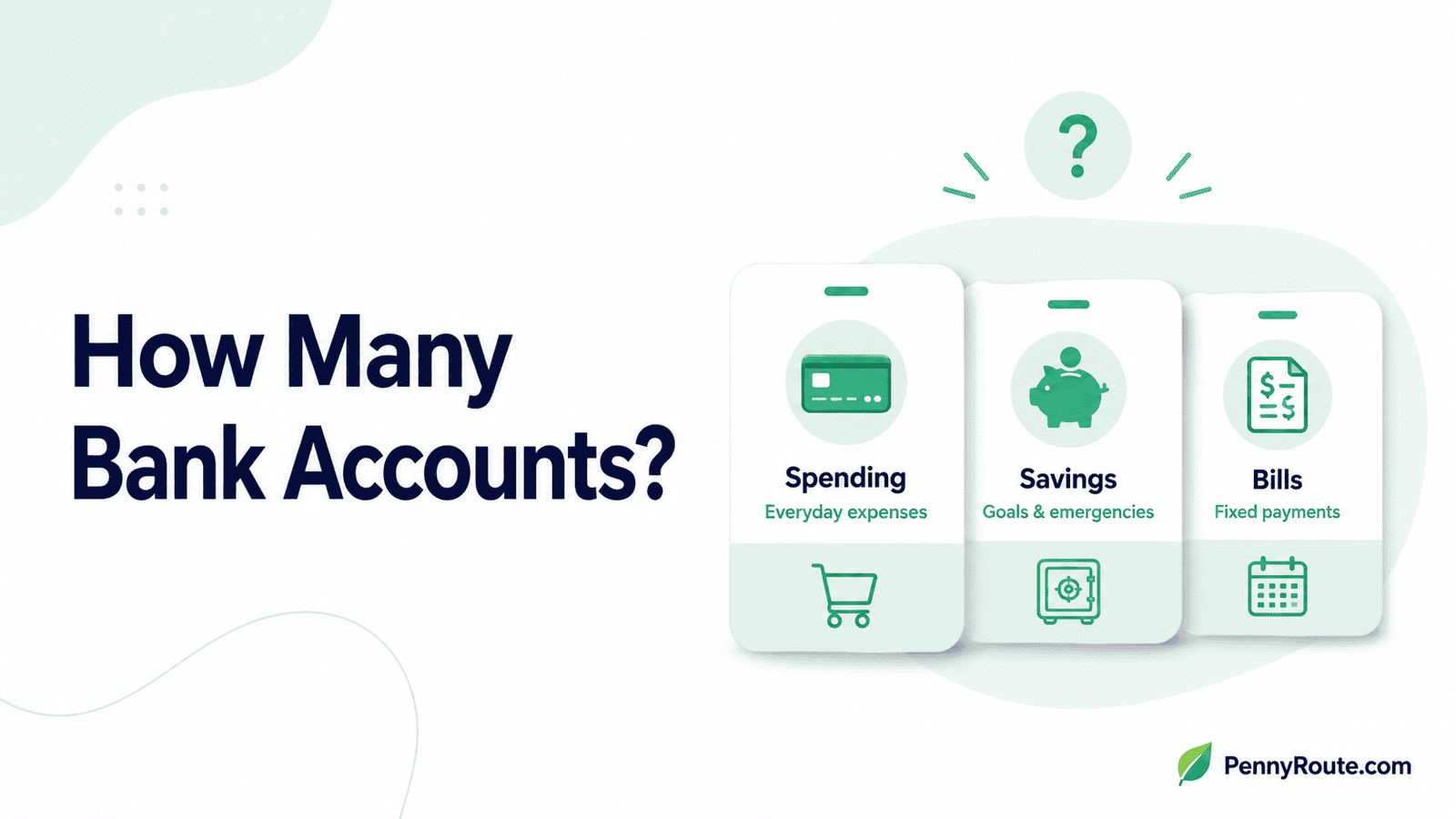

Common Reasons to Open a Second Checking Account

A second checking account can be useful when your current account is handling too many jobs at once. The most useful setups usually solve one everyday banking problem.

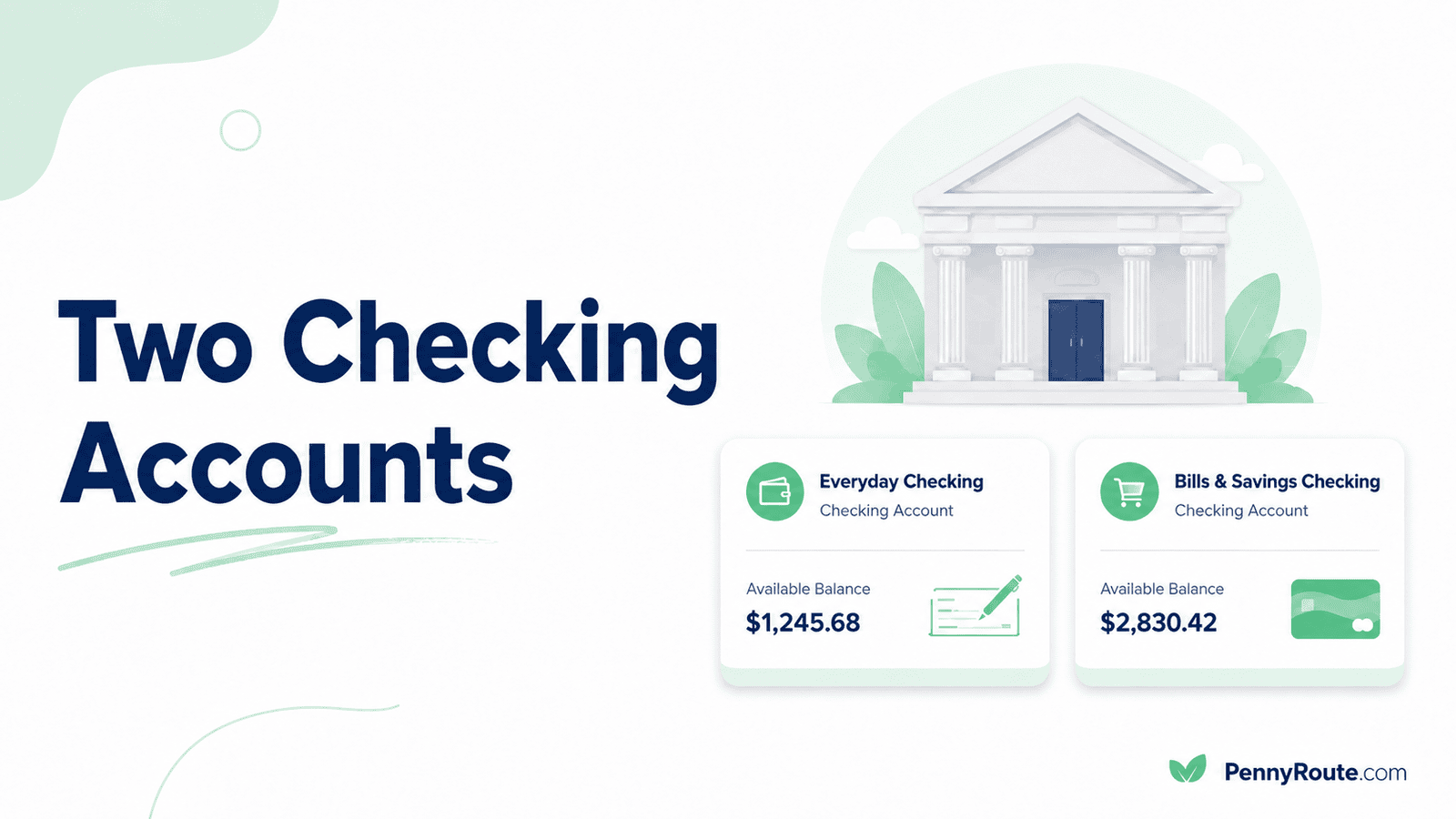

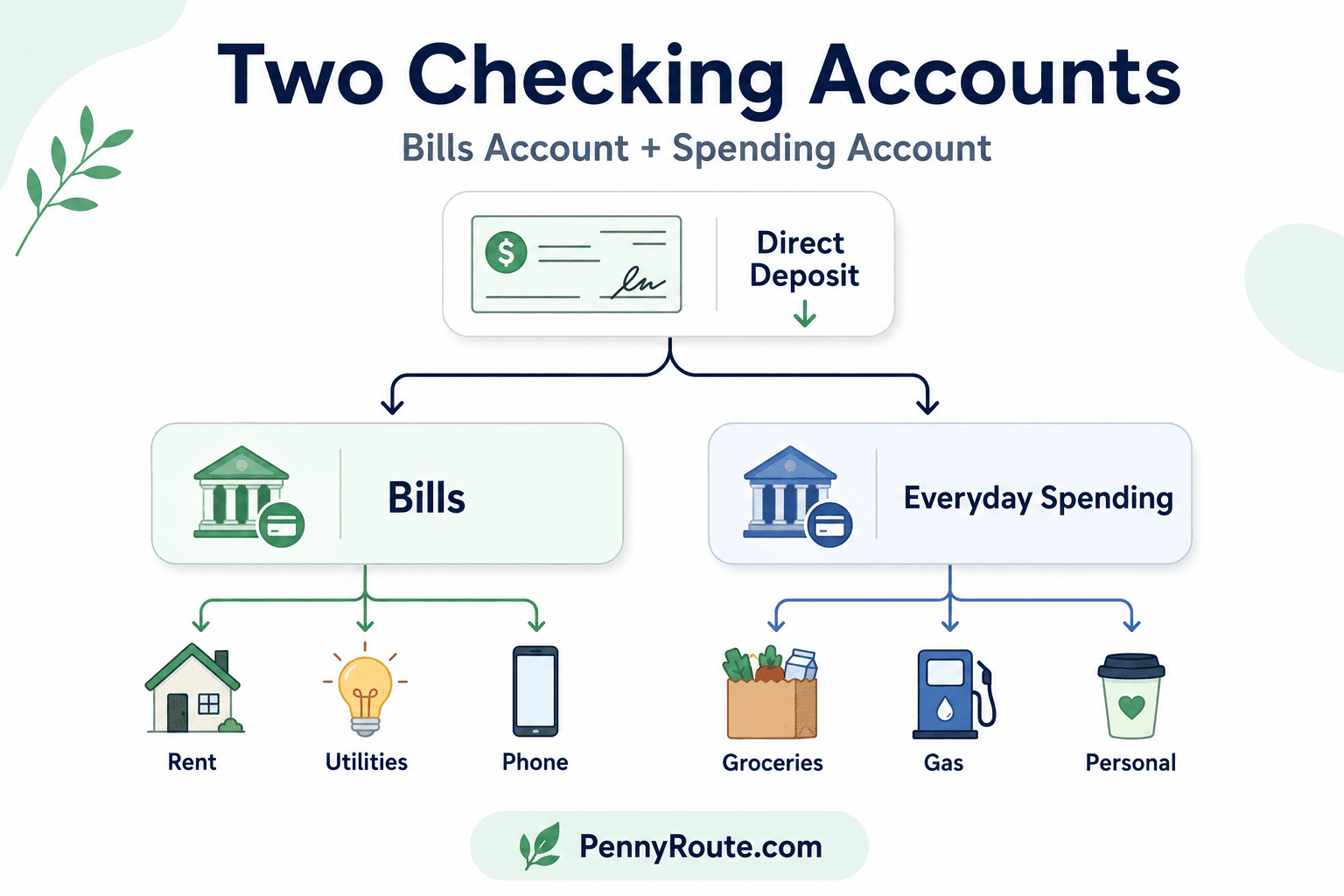

Bills and Everyday Spending

One common setup is to use one checking account for bills and another for everyday spending.

For example, your main account could cover rent, utilities, insurance, loan payments, and phone bills. Your second account could hold money for groceries, gas, eating out, and personal purchases.

This can help you see what is actually available to spend without accidentally using money needed for upcoming bills.

Side Income or Freelance Payments

If you earn money from freelance work, gig apps, online selling, or a side hustle, a second checking account can help keep that income separate from your personal spending.

This may make it easier to track payments, business-related expenses, and money you may need to set aside for taxes. Depending on your situation, you may still need a proper business bank account, but a separate account can be a cleaner starting point than mixing everything together.

A second checking account can also help with shared expenses.

For example, couples, roommates, or family members may use one account for rent, utilities, groceries, or other shared bills. This can make household costs easier to track, especially when more than one person contributes money.

Before using a shared account, make sure everyone understands who can deposit, withdraw, and manage the money.

Backup Debit Card Access

A second checking account can give you another way to access money if your main debit card is lost, your account is temporarily locked, or a transaction is flagged.

This works best when the second account has its own debit card and a small cushion. If backup access is your main reason, a different bank may be worth considering, which we’ll compare later.

Subscriptions and Recurring Payments

Some people use a second checking account only for subscriptions and recurring payments.

This can make it easier to see what is being charged each month. It may also help you catch forgotten subscriptions, price increases, or services you no longer use.

A separate account will not cancel subscriptions for you, but it can make recurring charges easier to notice.

What to Check Before Opening a Second Checking Account

Before you open another checking account, look beyond the “open account” button. The small rules matter, especially if you want the account to stay free and easy to use.

Monthly Fees

Start with the monthly fee, especially if you are trying to avoid bank fees on everyday accounts.

Check whether the second account has a monthly maintenance fee.

Some checking accounts are free only if you meet certain conditions, such as keeping a minimum balance, receiving direct deposit, or making a set number of debit card transactions. If those rules apply to each account separately, your second account may be harder to keep free.

Minimum Balance Rules

Some banks require you to keep a certain amount in the account to avoid fees.

This matters more with a second checking account because your money may be split between two balances. An account that looks free at first may cost money if you cannot meet the balance requirement every month.

Debit Card Setup

Find out whether the second account comes with its own debit card.

Some banks issue a separate card for each checking account. Others may connect one card to a main account or let you choose which account the card pulls from. This matters because using the wrong card or account can create avoidable mistakes.

Overdraft Settings

Having money in one checking account does not always protect the other account from overdrafting.

If your bill payment comes out of one account while your money is sitting in another, you could still face a failed payment or overdraft fee. Some banks offer overdraft transfers between linked accounts, but the rules and fees can vary.

Autopay and Direct Deposit

Check where your paycheck, transfers, and automatic payments will go.

If you plan to use one account for bills, make sure your automatic payments are connected to the correct account. A second checking account can make money easier to organize, but only if your deposits and payments are set up clearly.

Whether Checking Is the Right Account Type

A second checking account is not always the best tool.

If the money is for an emergency fund or a short-term savings goal, a savings account may be a better fit. A second checking account usually works better for money that needs regular payments, debit card access, or frequent movement.

Does Having Two Checking Accounts Affect Your Credit Score?

Having two checking accounts does not directly affect your credit score.

Checking accounts are deposit accounts, not credit accounts. They usually are not reported to the major credit bureaus the way credit cards, loans, or mortgages are.

So opening a second checking account generally will not:

- Lower your credit score

- Raise your credit score

- Change your credit utilization

- Show up as a regular credit account

That said, banks may review your banking history when you apply for a new account. This is different from your regular credit score. A bank may look at past account closures, unpaid negative balances, overdraft problems, or other banking records.

The bigger risk comes later if an account is mismanaged. If you leave unpaid fees, overdrafts, or a negative balance long enough, the bank may eventually send the debt to collections. That could affect your credit indirectly.

A second checking account will not hurt your credit score by itself, but unpaid account problems can create issues later.

Does FDIC Insurance Cover Each Checking Account Separately?

Not exactly. FDIC insurance is not based only on the number of accounts you open.

The standard FDIC insurance limit is generally $250,000 per depositor, per FDIC-insured bank, per ownership category. That means two individual checking accounts at the same bank are usually combined under the same ownership category.

For example, if you have $4,000 in one individual checking account and $2,000 in another individual checking account at the same FDIC-insured bank, both accounts are usually counted together for coverage purposes.

For normal everyday balances, this usually is not a major concern. But if you keep larger amounts in one bank, it is important to understand that opening a second checking account at the same bank does not automatically double your FDIC coverage.

A second checking account can help with organization, spending, bills, or backup access. It should not be used as a shortcut for extra deposit insurance.

Should Your Second Account Be Checking or Savings?

Before opening a second checking account, think about how often you’ll need to use the money.

A checking account usually works best for money that moves often. That includes bill payments, debit card purchases, transfers, subscriptions, and everyday spending.

A savings account usually works better for money you want to set aside and not touch as often. That might include an emergency fund, a vacation fund, a car repair fund, or money for an upcoming annual bill.

Here is a simple way to decide:

| Money Purpose | Better Account Type |

|---|---|

| Paying rent, utilities, or regular bills | Checking |

| Everyday debit card spending | Checking |

| Subscriptions and recurring payments | Checking |

| Side hustle income and expenses | Checking |

| Emergency fund | Savings |

| Short-term savings goals | Savings |

| Money you do not want to spend easily | Savings |

| Backup debit card access | Checking |

A second checking account can be helpful when you need easier access to the money. But if the real goal is to protect the money from everyday spending, a savings account may be the cleaner choice.

For example, if you want a separate place for groceries or subscriptions, checking makes sense. If you want to build an emergency fund, savings is usually a better fit because it creates more separation from daily spending.

Same Bank vs. Different Banks: Which Is Better?

You can open a second checking account at the same bank, but that is not always the best choice. It depends on what you want the second account to do.

If your main goal is easier organization, using the same bank may be simpler. You can usually see both accounts in one app, transfer money quickly, and manage everything from one login.

If your main goal is backup access, using a different bank may be stronger. If one bank has an app outage, freezes a card, flags a transaction, or has a temporary account issue, money at another bank may still be available.

Here is a simple comparison:

| Option | Best For | Watch Out For |

|---|---|---|

| Two checking accounts at the same bank | Simple transfers, one app, easier tracking | Same bank fees, same online banking outage, no automatic extra FDIC coverage |

| Checking accounts at different banks | Backup access, more account options, possible fee savings | More logins, slower transfers, more accounts to monitor |

For most beginners, two accounts at the same bank may be easier if the goal is budgeting or separating spending. But if you want access that is less dependent on one bank, using a second bank may give you more flexibility.

The best choice is the one that solves your actual problem without making your money harder to manage.

How to Manage Two Checking Accounts Without Getting Confused

Two checking accounts work best when the setup is simple. The more jobs you give each account, the easier it is to move money from the wrong place or miss a payment.

Decide What Each Account Pays For

Decide what each account is for before you start using it.

For example:

- Account 1: Bills and fixed expenses

- Account 2: Everyday spending

Or:

- Account 1: Personal spending

- Account 2: Side income

The labels matter less than the routine. You should be able to look at each account and know what that money is meant to cover.

Rename the Accounts in Your Banking App

Many banks let you add nicknames to your accounts.

Instead of seeing two similar checking accounts, you can label them:

- “Bills”

- “Spending”

- “Side Income”

- “Subscriptions”

- “Backup”

This small step can prevent mistakes, especially if both accounts are at the same bank and look almost identical in the app.

Keep Most Bills Connected to One Account

If possible, connect your regular bills to one main checking account.

That might include rent, utilities, insurance, phone bills, loan payments, and subscriptions. This keeps your bill system easier to track because you know where payments are supposed to come from.

If your paycheck goes into a different account, set a clear transfer routine so your bill account is funded before due dates, especially if you already use a simple monthly budget.

Turn On Account Alerts

Alerts can help you catch problems before they turn into fees.

Useful alerts include:

- Low balance alerts

- Large withdrawal alerts

- Direct deposit alerts

- Debit card purchase alerts

- Overdraft alerts

You do not need every notification your bank offers. Choose the ones that help you spot missing money, unexpected charges, or low balances quickly.

Review Both Accounts Once a Week

A second checking account should not require daily attention, but it should not be ignored either.

Once a week, check:

- Which bills have cleared

- Whether your spending account is still on track

- Whether any subscription charged the wrong account

- Whether you need to transfer money before upcoming payments

This quick check-in helps keep the system useful instead of turning it into another thing you have to untangle later.

Should You Open a Second Checking Account?

A second checking account can be helpful, but it should have a clear purpose. Opening another account just because it sounds organized may create more work without solving the real problem.

You may benefit from a second checking account if:

- You want to separate bills from everyday spending

- You keep spending money that was meant for upcoming payments

- You earn side income and want cleaner tracking

- You want a separate account for subscriptions or shared expenses

- You want backup debit card access

- You can avoid extra monthly fees and balance requirements

You may not need a second checking account if:

- Your current account system already works well

- You rarely check your account activity

- Your bank charges fees you cannot easily avoid

- Splitting money across accounts would make you more confused

- You are opening one without knowing what job it will have

A simple rule can help: open a second checking account only if it solves a specific problem.

For example, “I want one account for bills and one for weekly spending” is a clear reason. “Maybe another account will make me better with money” is not enough by itself.

The account will not fix your budget for you. But with a simple setup, it can make your money easier to separate, track, and use on purpose.

FAQs About Having Two Checking Accounts

Can I have two debit cards from the same bank?

Yes, you may be able to have two debit cards from the same bank, but it depends on the bank’s rules. Some banks issue a separate debit card for each checking account, while others may connect one debit card to a primary account or let you choose which account the card uses. Before opening a second checking account, ask how debit card access works so you do not accidentally spend from the wrong account.

Can I open two checking accounts online?

In many cases, yes. Some banks let existing customers open another checking account online or through the mobile app. You may still need to choose an account type, confirm your personal information, agree to the account terms, and meet any opening deposit or eligibility requirements. If the bank cannot approve the account online, it may ask you to visit a branch or provide more information.

Can my bank deny me a second checking account?

Yes, a bank can deny a second checking account. Even though there is no federal rule limiting you to one checking account, banks can still set their own approval requirements. They may review your identity, existing account history, unpaid negative balances, overdraft problems, or past account closures before approving another account.

Is it better to have two checking accounts or one checking and one savings account?

It depends on what the second account is for. Two checking accounts may work better if you need debit card access, bill payments, subscriptions, or frequent transfers. One checking account and one savings account may be better if you want to separate money for emergencies, short-term goals, or expenses you do not need to touch often. A checking account is usually better for money that moves often; a savings account is usually better for money you want to keep set aside.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.