An emergency expense can turn a normal month upside down fast.

A car repair you need for work, a sudden medical bill, reduced hours, or an urgent home repair can put pressure on your budget before you have time to adjust. Without money set aside, even one surprise cost can lead to credit card debt, missed bills, or pulling from savings meant for something else.

An emergency fund gives you a financial cushion for those moments. It helps you handle urgent, unexpected costs without starting from zero every time life gets expensive.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

Quick Overview: Emergency Fund

- An emergency fund is money set aside for urgent, unexpected expenses.

- A starter emergency fund of $500 to $1,000 can help you handle smaller surprises without relying on credit cards.

- A fuller emergency fund often covers three to six months of essential expenses, depending on your income, household needs, and risk level.

- Your emergency fund should be kept separate from everyday spending money, but still easy to access when you truly need it.

- Planned expenses, such as annual bills, holidays, and routine maintenance, usually belong in sinking funds instead of your emergency fund.

What Is an Emergency Fund?

An emergency fund is money you set aside for urgent, unexpected expenses that could disrupt your basic needs or financial stability.

This money is not for regular bills, planned purchases, or everyday overspending. It is there for situations that need quick attention, such as a sudden loss of income, an urgent medical cost, a necessary car repair, or an essential home repair.

For example, replacing worn tires is usually something to plan for with a car repair fund. But if your car breaks down unexpectedly and you need it to get to work, your emergency fund may help you handle the repair without immediately turning to a credit card.

The key difference is urgency. An emergency fund is meant for costs that are unexpected, important, and hard to delay.

Why an Emergency Fund Matters

An emergency fund gives you options when something urgent happens.

Without one, a surprise expense can quickly turn into a bigger problem. You may have to use a credit card, delay another bill, borrow money, or drain savings that were meant for a planned goal.

Even a small emergency fund can reduce that pressure. It may not solve every financial problem, but it can help you handle the first hit without completely throwing off your month.

The Consumer Financial Protection Bureau notes that emergency savings can help people prepare for unexpected events and reduce the need to borrow when a financial shock happens. That is why an emergency fund is less about reaching a perfect number right away and more about building a cushion you can actually use when life gets expensive.

How Much Should You Have in an Emergency Fund?

The right emergency fund amount depends on your monthly expenses, income stability, family needs, and how much risk you want to cover.

A good way to build it is in stages instead of aiming for the full amount on day one.

| Emergency Fund Stage | What It Covers | Best For |

|---|---|---|

| $500 to $1,000 starter fund | Smaller urgent expenses | Beginners, tight budgets, or anyone starting from zero |

| 1 month of essential expenses | One month of basic bills | A stronger first cushion |

| 3 to 6 months of essential expenses | Bigger emergencies or income loss | Most households over time |

| 6 to 12 months of essential expenses | Longer income gaps or higher-risk situations | Irregular income, single-income households, self-employment, or unstable work |

If saving three to six months sounds overwhelming, start with the first stage. A $500 emergency fund may not cover every problem, but it can still help with a minor car repair, urgent bill, or small medical cost.

After that, you can build toward one month of essential expenses. Once that feels stable, you can work toward three to six months based on your situation.

The amount should be based on what you truly need to keep your household running, not the version of your budget that includes every extra purchase.

Emergency Fund Formula: How to Calculate Your Number

Once you know your basic monthly expenses, you can calculate a more personal emergency fund target.

Use this simple formula:

Monthly essential expenses × number of months = emergency fund goal

Formula

For example, if your essential expenses are $2,500 per month, your emergency fund targets could look like this:

| Emergency Fund Goal | Calculation | Amount |

|---|---|---|

| 1 month of expenses | $2,500 × 1 | $2,500 |

| 3 months of expenses | $2,500 × 3 | $7,500 |

| 6 months of expenses | $2,500 × 6 | $15,000 |

This does not mean you need $15,000 before your emergency fund “counts.” It simply gives you a long-term number to work toward.

If your current budget is tight, use the formula to understand the target, then start with a smaller milestone. Reaching $500, then $1,000, then one month of expenses can make the process feel more realistic.

Spending Shock vs. Income Shock: Why Your Goal May Be Different

Not every emergency fund needs to cover the same type of problem.

Some emergencies are spending shocks. These are sudden costs that hit your budget once, such as an urgent car repair, a medical bill, or a home repair that cannot wait. A starter emergency fund can help with these smaller shocks while you build a larger cushion.

Other emergencies are income shocks. These happen when your income drops or stops for a period of time. Job loss, reduced hours, delayed freelance payments, or a slow business month can all create a bigger gap because your regular bills keep coming even when income is lower.

This is why one person may feel more secure with $1,000, while another may need several months of essential expenses. A stable two-income household may have a different target than a single-income household, freelancer, or someone with irregular income.

Start by asking what kind of risk would hurt your budget most. If one surprise bill is your biggest concern, a starter fund may be the first milestone. If income loss would create the biggest stress, building toward several months of essentials matters more.

What Expenses Should Your Emergency Fund Cover?

Your emergency fund target should be based on essential expenses, not every part of your normal spending.

Essential expenses are the costs you would still need to cover during a serious financial setback, such as a job loss, reduced income, or urgent situation. These are usually the bills and basic needs that keep your household stable.

Common expenses to include are:

| Essential Expense | Why It Matters |

|---|---|

| Housing | Rent or mortgage payments help keep your home secure. |

| Utilities | Electricity, water, gas, and basic services still need to be paid. |

| Groceries | Your fund should cover basic food needs, not full restaurant spending. |

| Transportation | Gas, public transit, or necessary car costs may be needed for work and daily life. |

| Insurance | Health, auto, renters, homeowners, or other essential coverage may need to continue. |

| Minimum debt payments | Keeping minimum payments current can help avoid late fees and credit damage. |

| Basic medical costs | Prescriptions, co-pays, or urgent care costs may need a place in the estimate. |

| Childcare or essential family costs | If these are required for work or basic care, include them in your number. |

You do not have to include every flexible category. Dining out, entertainment, shopping, subscriptions you could pause, and extra personal spending usually do not need to be part of your emergency fund calculation.

A simple list of your regular budget categories can help you separate true essentials from expenses you could reduce during a difficult month.

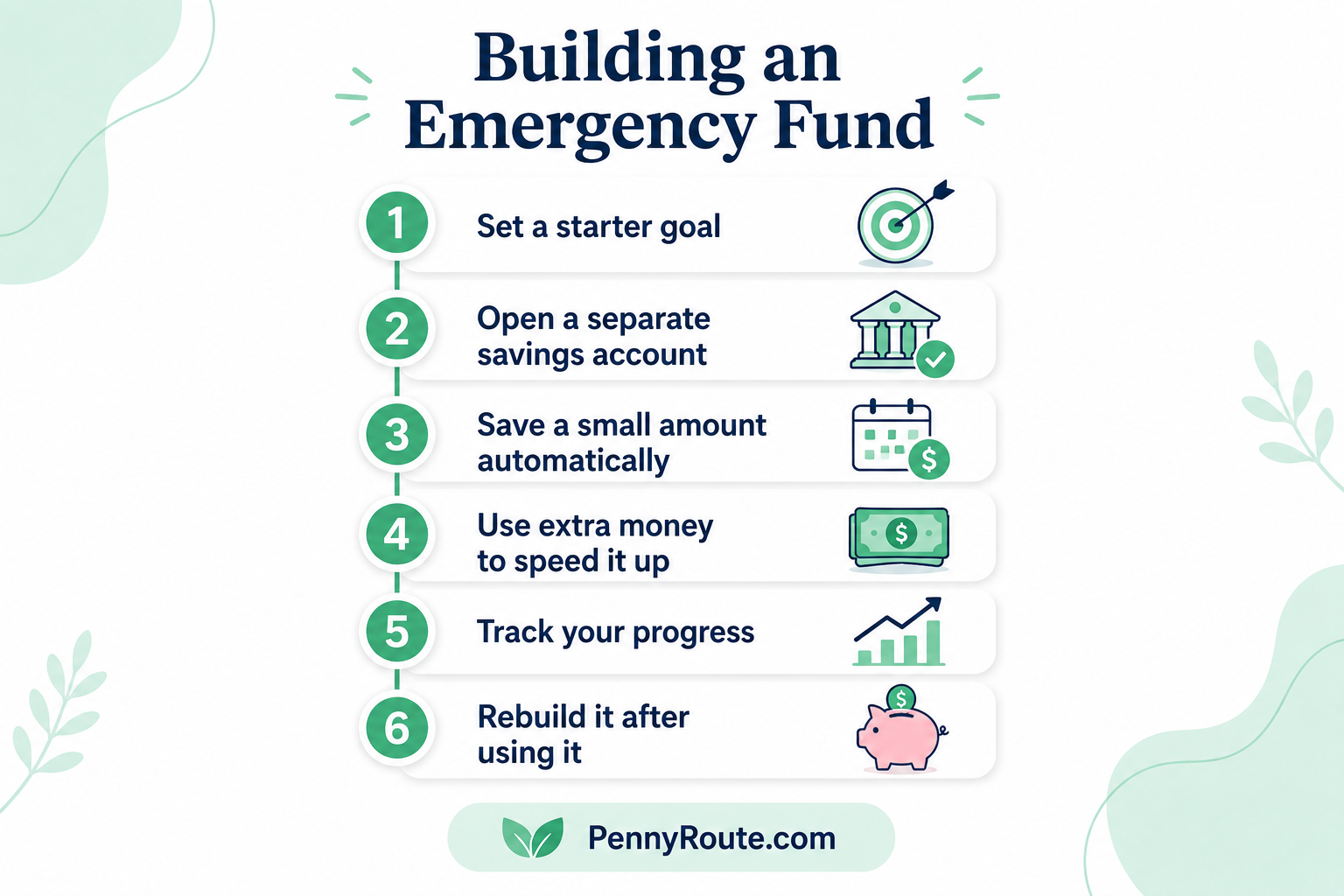

How to Build an Emergency Fund Step by Step

Building an emergency fund is easier when you treat it as a series of small milestones instead of one large savings target.

Choose Your First Milestone

Start with a number that feels possible. For many beginners, that may be $500 or $1,000. If even that feels too high right now, start with $100.

The first milestone is not meant to solve every emergency. It gives you a small cushion so one urgent expense does not immediately become a credit card balance or missed bill.

Keep the Money Separate

Choose a place for your emergency fund before you start saving. A separate savings account can make the money easier to protect because it is not mixed with groceries, bills, and everyday spending.

You can still keep it accessible. The point is to create enough separation that you do not accidentally spend it.

Set a Small Automatic Transfer

If possible, set up a small transfer after payday. This could be $10, $25, $50, or whatever fits your budget.

Automatic saving helps because you do not have to restart the decision every time you get paid. Even small amounts can build momentum when they happen consistently.

This is similar to the pay yourself first budget, where savings moves before everyday spending has a chance to absorb the money.

Use Extra Money When It Appears

Small windfalls can help your emergency fund grow faster without adding pressure to your regular budget.

Tax refunds, cashback, work bonuses, gifts, refunds, or money from selling unused items can all move you closer to your next milestone. You do not have to use every extra dollar, but sending part of it to your emergency fund can make a noticeable difference.

Build Toward the Next Stage

Once you reach your first milestone, move to the next one. That might be one month of essential expenses, then three months, then more if your situation calls for it.

This staged approach keeps the process realistic. You are not failing because you do not have a full emergency fund yet. You are building the cushion one layer at a time.

Where Should You Keep Your Emergency Fund?

Your emergency fund should be easy to access in a real emergency, but separate enough that you do not spend it by accident.

Use a Separate Savings Account

For most people, a separate savings account is a practical choice. It keeps the money away from daily checking activity while still making it available when you need it.

A high-yield savings account can also work well if it gives you easy access and does not lock the money away.

Avoid Mixing It With Everyday Spending

Try not to keep your full emergency fund in your regular checking account.

When emergency savings sit beside grocery money, bill money, and spending money, it becomes easier to use them for non-emergencies without noticing.

Be Careful With Investments

Emergency savings usually should not depend on the stock market or accounts with withdrawal delays.

An emergency fund is mainly about safety and access, not chasing the highest possible return. If you may need the money quickly, it should not be somewhere that could lose value right before you need it.

Keep It Safe and Accessible

If you use a bank savings account, the FDIC notes that keeping emergency savings in a separate FDIC-insured account can make the money less tempting to spend while still keeping it protected at an insured bank.

The best place for your emergency fund is simple: safe, separate, and available when a real emergency happens.

If you are deciding between everyday access and separation, understanding checking vs. savings accounts can make the choice easier.

When Should You Use Your Emergency Fund?

Use your emergency fund when an expense is urgent, unexpected, and important enough that delaying it could create a bigger problem.

Good reasons to use an emergency fund may include:

- job loss or reduced work hours

- an urgent medical or dental expense

- a necessary car repair if you need the car for work or basic transportation

- an essential home repair, such as a broken heater, plumbing issue, or safety problem

- basic bills during a temporary income gap

- emergency travel for a serious family situation

The key word is necessary. A sale, vacation, routine maintenance, holiday shopping, or annual bill may feel expensive, but those are usually better handled with a sinking fund or regular budget category.

Car costs are a good example. If your car suddenly breaks down and you need it to get to work, that may be an emergency. But predictable costs like oil changes, new tires, and routine repairs usually fit better in a car repair fund.

Before using your emergency fund, ask yourself three quick questions:

| Question | Why It Helps |

|---|---|

| Is this urgent? | It helps separate real emergencies from costs that can wait. |

| Is this necessary? | It keeps the fund focused on basic needs and financial stability. |

| Was this unexpected? | It protects the fund from planned expenses that should have their own category. |

If the answer is yes to all three, using your emergency fund may make sense. After that, the next step is to rebuild it when your budget allows.

Emergency Fund vs. Rainy Day Fund vs. Sinking Fund

An emergency fund, rainy day fund, and sinking fund can all help protect your budget, but they are not meant for the same type of expense.

| Fund Type | Best For | Example |

|---|---|---|

| Emergency fund | Bigger urgent situations | Job loss, reduced income, major urgent repair |

| Rainy day fund | Smaller unexpected costs | A higher utility bill or minor repair |

| Sinking fund | Planned future expenses | Car insurance, holiday gifts, annual subscriptions |

Emergency Fund

An emergency fund is for bigger financial shocks that affect your basic needs or income. It can help cover essentials during job loss, reduced work hours, urgent repairs, or other serious unexpected situations.

Rainy Day Fund

A rainy day fund is usually for smaller surprises that do not require a full emergency fund withdrawal. For example, a minor repair, small unexpected bill, or temporary budget gap may fit better here.

Sinking Fund

A sinking fund is for planned expenses you can see coming. Annual bills, routine car maintenance, holiday spending, and school costs may feel stressful, but they are usually better handled before they become emergencies.

Keeping these funds separate helps you use the right money for the right problem. Your emergency fund stays protected for serious situations, while smaller surprises and planned expenses have their own place in your budget.

Should You Build an Emergency Fund or Pay Off Debt First?

If you have debt, it can be hard to know whether extra money should go toward emergency savings or faster debt payoff.

For many beginners, a small starter emergency fund comes first. That could be $500, $1,000, or another amount that helps you avoid turning every surprise expense into new debt. Keep making at least the minimum payments on your debts so you avoid late fees and other problems.

Start With a Small Cushion

A starter emergency fund gives you a little breathing room while you work on debt.

Without even a small cushion, one urgent car repair, medical bill, or income dip can push you back onto a credit card. That can make debt payoff feel like one step forward and one expensive step back.

Focus More on High-Interest Debt Next

Once you have a starter cushion, you may choose to put more extra money toward high-interest debt, especially credit cards or other expensive balances.

This does not mean you stop saving forever. It simply means your emergency fund and debt payoff can happen in stages instead of competing for every dollar at the same time.

Keep Building Later

After your high-interest debt feels more manageable, you can build your emergency fund toward one month of essential expenses, then three to six months over time.

The balance depends on your risk level. If your income is unstable, your job feels uncertain, or you have dependents, keeping a larger emergency cushion may matter more while you pay down debt.

How to Build an Emergency Fund When Money Is Tight

Building an emergency fund can feel frustrating when most of your income already has a job before it arrives.

If saving $500 or $1,000 feels out of reach right now, start smaller. A first goal of $100 or $250 can still give you a little breathing room and help you build the habit.

Save Small Amounts Consistently

You do not need a large transfer to make progress.

Saving $5, $10, or $25 at a time may feel small, but it is still better than waiting until you can save a perfect amount. Small transfers also make the habit easier to keep when your budget is tight.

Use Extra Money Carefully

If you receive a refund, cashback, gift, overtime pay, or money from selling something you no longer use, consider putting part of it into your emergency fund.

You do not have to send every extra dollar to savings. Even setting aside a portion can help your fund grow without adding pressure to your normal bills.

Reduce the First Target

A starter emergency fund should fit your real life.

If $1,000 feels impossible right now, aim for $100 first. Then try $250. Then $500. Each step gives you more protection than having nothing set aside.

Avoid Comparing Your Timeline

Someone else may build an emergency fund in three months. You may need longer, and that is still progress.

What matters is creating a cushion that is stronger than last month. Even a small emergency fund can reduce the chance that one surprise expense turns into new debt.

If bills already take most of your paycheck, broader ideas for how to save money on a low income can help you find small places to start.

How Often Should You Review Your Emergency Fund?

Your emergency fund does not need constant attention, but it should not stay untouched for years without a quick check.

A good rule is to review it once or twice a year, or whenever your life changes in a way that affects your basic expenses.

Review After Major Budget Changes

Update your emergency fund target if your rent increases, groceries cost more, insurance changes, or your monthly bills become higher.

Your old emergency fund number may have made sense last year, but it may not fully match your current cost of living.

Review After Life Changes

A job change, new baby, move, marriage, divorce, new pet, or shift to one income can change how much cushion you need.

Your emergency fund should reflect the household you have now, not the one you had when you first created the savings goal.

Review After You Use the Fund

If you use part of your emergency fund, make a simple plan to rebuild it.

You do not have to replace the full amount immediately, but the fund should move back onto your budget so it does not stay half-empty for months.

A Simple Emergency Fund Plan to Start This Month

You do not need to build a full emergency fund all at once. Start with one small cushion, one clear place for the money, and one repeatable savings habit.

| Step | What to Do |

|---|---|

| 1 | Choose your first emergency fund goal, such as $100, $500, or $1,000. |

| 2 | List your essential monthly expenses so you know your bigger target later. |

| 3 | Pick a separate savings place for the money. |

| 4 | Set one small transfer after payday, even if it is only $10 or $25. |

| 5 | Add part of any extra money when it appears. |

| 6 | Review your progress after one month. |

| 7 | Move to the next milestone when the first one feels steady. |

The first step matters most because it gives you something to build on. Once you have a small emergency cushion, the next surprise expense may still be annoying, but it does not have to knock your whole budget off track.

Emergency Fund FAQs

How much should I have in an emergency fund?

A common long-term target is three to six months of essential expenses, but you do not need to start there. A starter emergency fund of $500 to $1,000 can still help with smaller urgent expenses while you build toward a larger cushion.

Is $1,000 enough for an emergency fund?

$1,000 can be a helpful starter emergency fund, but it may not be enough for larger emergencies like job loss, major repairs, or several months of reduced income. Treat it as a first milestone, then build toward one month and eventually three to six months of essential expenses.

What is the emergency fund formula?

The simple emergency fund formula is: monthly essential expenses × number of months = emergency fund goal. For example, if your essential expenses are $2,500 per month, a three-month emergency fund would be $7,500.

Where should I keep my emergency fund?

A separate savings account is usually a practical place for an emergency fund because it keeps the money away from everyday spending while still making it accessible. A high-yield savings account can also work if it does not limit access when you need the money.

Should I keep my emergency fund in checking or savings?

Savings is usually better than checking for most of your emergency fund because it creates separation from daily spending. You may keep a small amount in checking if needed, but the main fund should be protected from accidental use.

Can I invest my emergency fund?

Emergency fund money usually should not be invested because you may need it quickly. Investments can lose value or take time to access, which can create problems during a real emergency.

What counts as an emergency?

An emergency is usually urgent, unexpected, and necessary. Examples include job loss, reduced income, urgent medical costs, essential car repairs, major home repairs, or basic bills during a temporary income gap.

Is an emergency fund the same as a rainy day fund?

No. A rainy day fund is usually for smaller unexpected costs, while an emergency fund is for bigger financial shocks that affect your income, housing, health, transportation, or basic needs.

Should I build an emergency fund before paying off debt?

Many people start with a small emergency fund before focusing heavily on debt payoff. A starter cushion can help prevent new debt when an urgent expense appears, while minimum debt payments should still stay current.

How often should I update my emergency fund goal?

Review your emergency fund once or twice a year, or after major life changes. A rent increase, new job, income change, new baby, move, or higher monthly bills can all change how much emergency savings you need.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.