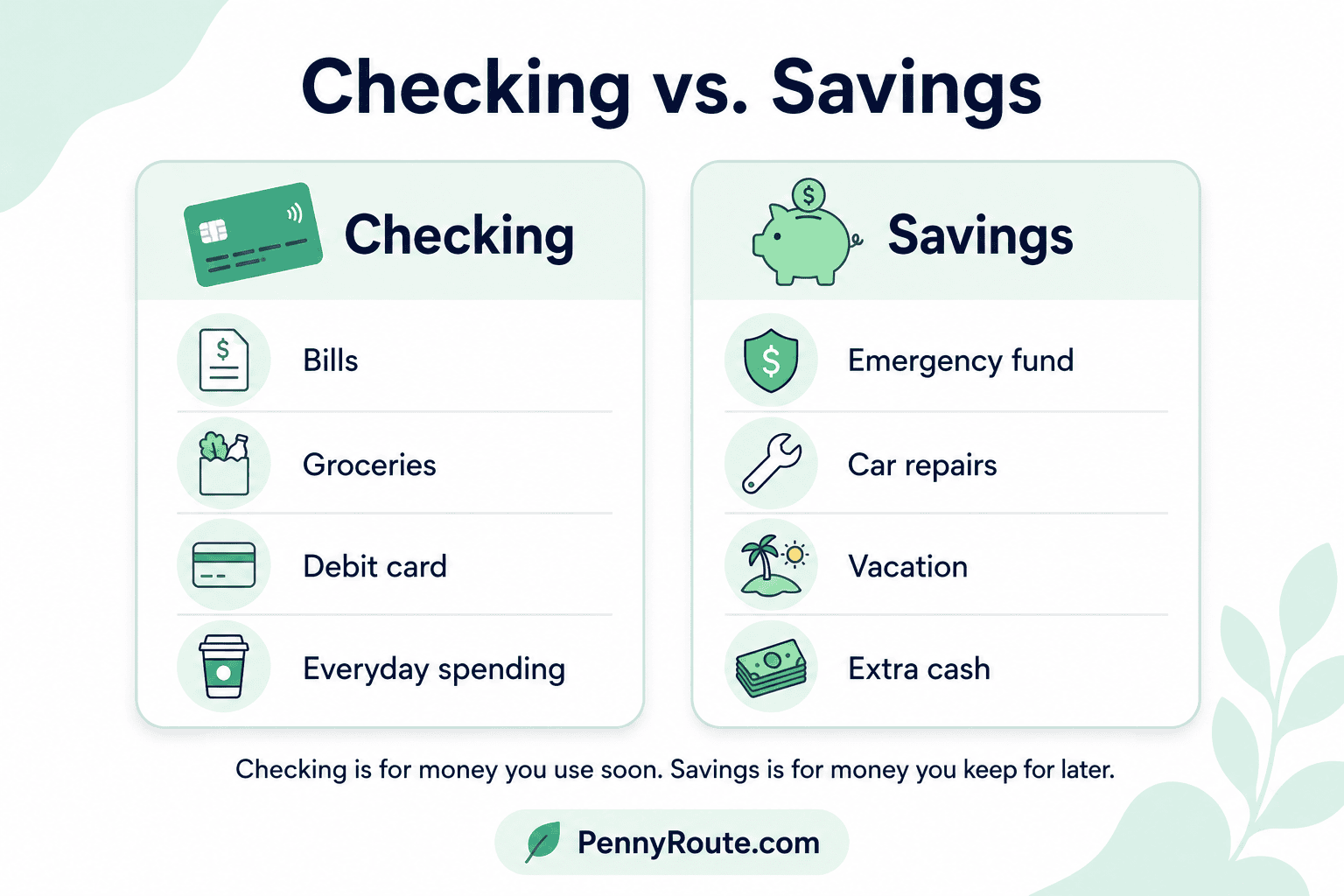

Checking and savings accounts can look similar because both hold money. But they are not meant to do the same job.

A checking account is usually for money you plan to use soon, such as bills, groceries, debit card purchases, ATM withdrawals, and automatic payments.

A savings account is usually for money you want to keep separate for later, such as an emergency fund, a planned purchase, or extra cash you do not want mixed with everyday spending.

The easiest way to think about checking vs. savings account is this: checking is for money that moves often, and savings is for money that waits.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

Checking vs. Savings Account: The Simple Difference

The simple difference is this: a checking account is for everyday money, while a savings account is for money you want to set aside.

| Account | Best For | Main Strength |

|---|---|---|

| Checking account | Bills, debit card purchases, regular spending | Easy access |

| Savings account | Emergency fund, short-term goals, extra cash | Separation and possible interest |

A checking account is useful when money needs to move in and out often. Your paycheck may come in, then rent, groceries, utilities, subscriptions, and card purchases may go out.

A savings account is useful when you want money to stay put. It can help you separate money for emergencies, future purchases, or planned expenses so it does not blend into daily spending.

Neither account is “better” on its own. They simply have different jobs. Checking helps you manage today’s money. Savings helps you protect money for later.

What a Checking Account Is Used For

A checking account is usually the account you use for everyday money. It is built for money that comes in and goes out often.

You might use a checking account for:

- Direct deposit from your job

- Rent or mortgage payments

- Utility bills

- Debit card purchases

- ATM withdrawals

- Transfers

- Subscriptions

- Automatic payments

For example, if your rent is due next week, your phone bill is on autopay, and you need to buy groceries this weekend, that money usually belongs in checking.

The main benefit of a checking account is easy access. You can spend, transfer, withdraw, and pay bills without moving money around every time.

The downside is that easy access can also make it easier to overspend. That is why checking works best when it holds money for bills, regular spending, and a small buffer, not every dollar you have.

What a Savings Account Is Used For

A savings account is usually for money you do not plan to spend right away. It gives you a separate place to keep cash for future needs, goals, or expenses that are not part of your everyday spending.

You might use a savings account for:

- Emergency savings

- Car repairs

- Medical costs

- Vacation savings

- Annual bills

- Holiday spending

- A future move

- Extra cash after bills are covered

For example, if you are saving $50 each paycheck for car repairs, that money may be better in savings than checking. It is still accessible, but it is not sitting next to your grocery money and subscriptions.

Some savings accounts also earn interest. The amount depends on the bank and account type, but the main beginner benefit is simple: savings helps you keep future money separate from money you use every day.

A savings account works best when it has a clear purpose. Even if you start small, separating savings from checking can make it easier to see what is safe to spend and what should stay untouched.

Key Differences Between Checking and Savings Accounts

Checking and savings accounts both hold money, but they work differently in everyday use. The NCUA’s money basics guide also explains that checking and savings accounts serve different everyday money needs, which is why it helps to understand how each one works before deciding where your money should sit.

| Feature | Checking Account | Savings Account |

|---|---|---|

| Main purpose | Daily spending and bills | Saving money for later |

| Access | Very easy | Usually less frequent |

| Debit card or checks | Common | Usually limited or unavailable |

| Interest | Usually low or none | Often higher than checking |

| Best for | Paychecks, bills, purchases, withdrawals | Emergency funds, goals, extra cash |

| Main risk to watch | Overspending or overdrafts | Using it too often for everyday spending |

The biggest difference is access.

Checking accounts are designed for frequent transactions. That makes them useful for daily life, but it also means money can leave quickly if you are not paying attention.

Savings accounts are designed to slow things down a little. The money is still yours, but keeping it separate can make it easier to avoid spending it by accident.

So, if the money needs to move soon, checking usually makes sense. If the money is waiting for a future purpose, savings is usually the better fit.

Do You Need Both Checking and Savings Accounts?

You do not always need both accounts right away. If you are just starting out, a checking account may be the first priority because it can handle income, bills, debit card purchases, and everyday spending.

But having both checking and savings can make money easier to manage.

A checking account helps you handle money that moves often. A savings account helps you protect money that should not be spent right away.

One account may be enough if:

- You are opening your first bank account

- Your balance is still very low

- You mainly need a place to receive income and pay bills

- You want to keep banking simple while you get started

Both accounts may help if:

- You want to build an emergency fund

- You are saving for short-term goals

- You want to separate bill money from savings

- You keep spending money that was meant for later

- You want a clearer system after payday

You do not need a complicated setup. For many beginners, one checking account and one savings account is enough to start.

If you are opening your first account, start with the basics and learn how to open a basic bank account online before adding more accounts.

How to Use Checking and Savings Together

Checking and savings accounts work best when they support each other.

A simple payday setup might look like this:

- Income goes into checking.

Your paycheck or regular income lands in your checking account first. - Bills and regular spending stay in checking.

Keep enough money there for rent, groceries, utilities, subscriptions, transportation, and other normal expenses. - Extra money moves to savings.

After bills and regular spending are covered, move money you do not need right away into savings. - Planned expenses can go into sinking funds.

If you are saving for car repairs, holidays, annual bills, or travel, sinking funds can help you keep those goals separate. - Checking keeps a small buffer.

Leave a little extra in checking for timing gaps, small surprises, or payments that clear earlier than expected.

This setup keeps everyday money easy to access while helping savings stay protected. It also makes your balance clearer because everything is not sitting in one account pretending to be “available.”

How Much Money Should Go in Each Account?

A simple starting point is to keep money for current expenses in checking and money for future needs in savings.

For checking, that usually means enough to cover:

- Rent or mortgage

- Utilities

- Groceries

- Transportation

- Subscriptions

- Debt payments

- Automatic payments

- Regular personal spending

- A small buffer

If you are not sure where to start, use the simple rule from our guide on how much money to keep in checking: regular monthly expenses plus a small cushion.

For savings, focus on money you do not need for daily spending. That may include:

- Emergency savings

- Short-term goals

- Planned expenses

- Extra cash after bills are covered

- Money you want to keep away from everyday spending

For example, if your monthly expenses are $2,500, you might keep around $2,800 to $3,000 in checking and move extra money to savings, depending on your goals and comfort level.

The exact split does not need to be perfect. The goal is to make sure bills are covered while your savings has a separate place to grow.

Common Mistakes to Avoid

Checking and savings accounts are simple once you understand their jobs, but a few small mistakes can make them harder to manage.

Keeping all your money in checking

Checking is easy to spend from, which is helpful for bills and daily purchases.

But if your emergency money, vacation savings, and extra cash all sit in checking, your balance can look higher than it really is. That makes it easier to spend money you meant to save.

Using savings like a second checking account

Savings works best when it has a purpose.

If you keep moving money in and out for everyday purchases, it becomes harder to tell what you are actually saving. Try to use checking for regular spending and savings for money you want to keep for later.

Moving too much out of checking before bills clear

Extra money is not always truly extra.

Before moving cash to savings, make sure important bills like rent, utilities, insurance, and card payments have cleared or are already planned for.

Ignoring account fees and balance rules

Both checking and savings accounts can have fees or requirements.

Check for monthly fees, minimum balance rules, overdraft fees, ATM fees, or transfer limits before choosing an account.

Not setting up account alerts

Low-balance alerts and transaction alerts can help you catch problems early.

They can also make it easier to notice unusual charges, forgotten subscriptions, or spending that is higher than expected.

Which Account Should You Use? Simple Examples

Sometimes the easiest way to choose between checking and savings is to look at what the money is for.

| Situation | Better Account |

|---|---|

| Paying rent next week | Checking |

| Buying groceries | Checking |

| Monthly phone bill autopay | Checking |

| Debit card spending | Checking |

| Cash you may need today | Checking |

| Emergency fund | Savings |

| Saving for car repairs | Savings or sinking fund |

| Vacation savings | Savings |

| Holiday spending | Savings or sinking fund |

| Extra money after bills | Savings |

Here is the simple rule: if the money needs to move soon, checking usually makes sense. If the money is waiting for a future need, savings is usually the better place.

For example, your rent money should not be tucked away in savings if rent is due in a few days. But money for a car repair that might happen months from now probably does not need to sit in checking next to your grocery money.

Checking and Savings Work Better Together

Checking and savings accounts do not need to compete with each other. They work best when each one has a clear job.

Your checking account can handle the money you use often, such as income, bills, debit card purchases, transfers, and regular spending. While your savings account can hold the money you want to protect. For example, emergency savings, short-term goals, planned expenses, and extra cash after bills are covered.

You do not need a perfect setup to start. Even a simple system can help:

- Keep bill money in checking

- Move future money to savings

- Leave a small buffer for timing gaps

- Review both accounts regularly

The goal is to make your money easier to understand. Together, they give your money a simple system: one place for daily use and one place for future needs.

FAQs About Checking vs. Savings Accounts

Is it better to keep money in checking or savings?

It depends on what the money is for. Money for bills, debit card purchases, and daily spending usually belongs in checking. Money for emergencies, short-term goals, or extra cash you do not need right away usually belongs in savings.

Can I use a savings account like a checking account?

A savings account is not the best place for everyday spending. You may be able to transfer money from savings when needed, but checking is usually better for regular purchases, bill payments, ATM withdrawals, and debit card use.

Should my paycheck go into checking or savings?

Most people have their paycheck deposited into a checking account first. From there, you can keep enough for bills and regular spending, then move some money to savings for emergencies, goals, or planned expenses.

How much money should I keep in checking vs. savings?

A simple approach is to keep regular monthly expenses plus a small buffer in checking. Savings can hold your emergency fund, short-term goals, sinking funds, and money you do not need for daily spending.

Do savings accounts earn more than checking accounts?

Often, yes. Savings accounts usually earn more interest than checking accounts, but rates vary by bank and account type. Even when the interest is small, savings can still be useful because it keeps future money separate from everyday spending.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.