Debt can take up too much space in your monthly budget. Between minimum payments, interest charges, due dates, and everyday expenses, progress can feel slow even when you are making payments on time.

That is frustrating, but it does not mean you are stuck.

Paying off debt faster usually starts with a simple plan: list what you owe, choose one debt to focus on first, pay more than the minimum when possible, and avoid adding new balances while you work through the plan.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

Quick Overview: How to Pay Off Debt Faster

- List every debt with the balance, interest rate, minimum payment, and due date.

- Keep making minimum payments on all debts to avoid fees, penalties, and credit damage.

- Choose one target debt using the snowball, avalanche, or hybrid method.

- Put any extra money toward your target debt until it is paid off.

- Look for ways to lower interest, but check fees and repayment terms first.

- Avoid adding new debt while you are paying off old balances.

- Get extra help if minimum payments are unaffordable or debt is affecting basic needs.

Before You Try to Pay Off Debt Faster

Paying off debt faster works best when your basic bills are covered first.

Before you send extra money to debt, make sure you can still cover housing, utilities, groceries, transportation, insurance, and minimum payments on every account. If extra payments leave you short on essentials, you may end up using credit again and losing the progress you just made.

A good debt payoff plan should reduce pressure over time, not make your monthly budget impossible to live with.

Once your basic monthly needs are covered, the next step is to see every debt clearly in one place.

List Every Debt You Owe

Before you can pay off debt faster, you need a clear picture of what you are dealing with.

That means listing every debt in one place. It may not be the most exciting task, but it removes the guesswork. Once you can see the balances, interest rates, and minimum payments together, it becomes much easier to choose a smart payoff plan.

Create a simple list with:

- The lender or creditor

- Total balance

- Interest rate

- Minimum monthly payment

- Due date

- Type of debt

Here is an example:

Use this as a simple debt payoff worksheet

| Debt | Balance | Interest Rate | Minimum Payment | Due Date | Target Order |

|---|---|---|---|---|---|

| Credit card 1 | $2,400 | 24.99% | $75 | 12th | 2 |

| Personal loan | $5,000 | 11.50% | $180 | 18th | 3 |

| Medical bill | $900 | 0% | $50 | 25th | 4 |

| Store card | $650 | 28.99% | $35 | 3rd | 1 |

The “target order” column is optional at first. You can fill it in after you choose a payoff method. If you use the debt snowball method, your first target is usually the smallest balance. If you use the debt avalanche method, your first target is usually the debt with the highest interest rate.

Do not worry about making decisions yet. At this stage, you are just gathering the facts.

Once everything is listed, you can see which debts are costing you the most, which balances are smallest, and how much you need each month just to stay current. This gives your payoff plan a solid starting point.

Make Minimum Payments on Everything First

Before you put extra money toward one debt, make sure you can cover the minimum payments on all your debts.

This may sound obvious, but it is an easy mistake to make. For example, paying an extra $100 toward one credit card is not helpful if it causes you to miss the minimum payment on another account.

Minimum payments help you stay current and avoid late fees, penalty rates, and possible credit damage. They may not pay off debt quickly on their own, but they protect the foundation of your payoff plan.

A simple approach is:

- Pay the minimum due on every debt.

- Pick one debt as your main target.

- Put any extra money toward that target debt only.

- Once that debt is paid off, move the extra payment to the next one.

This keeps your plan organized. Instead of spreading extra money across several debts and barely noticing progress, you give one balance your full attention while keeping everything else current.

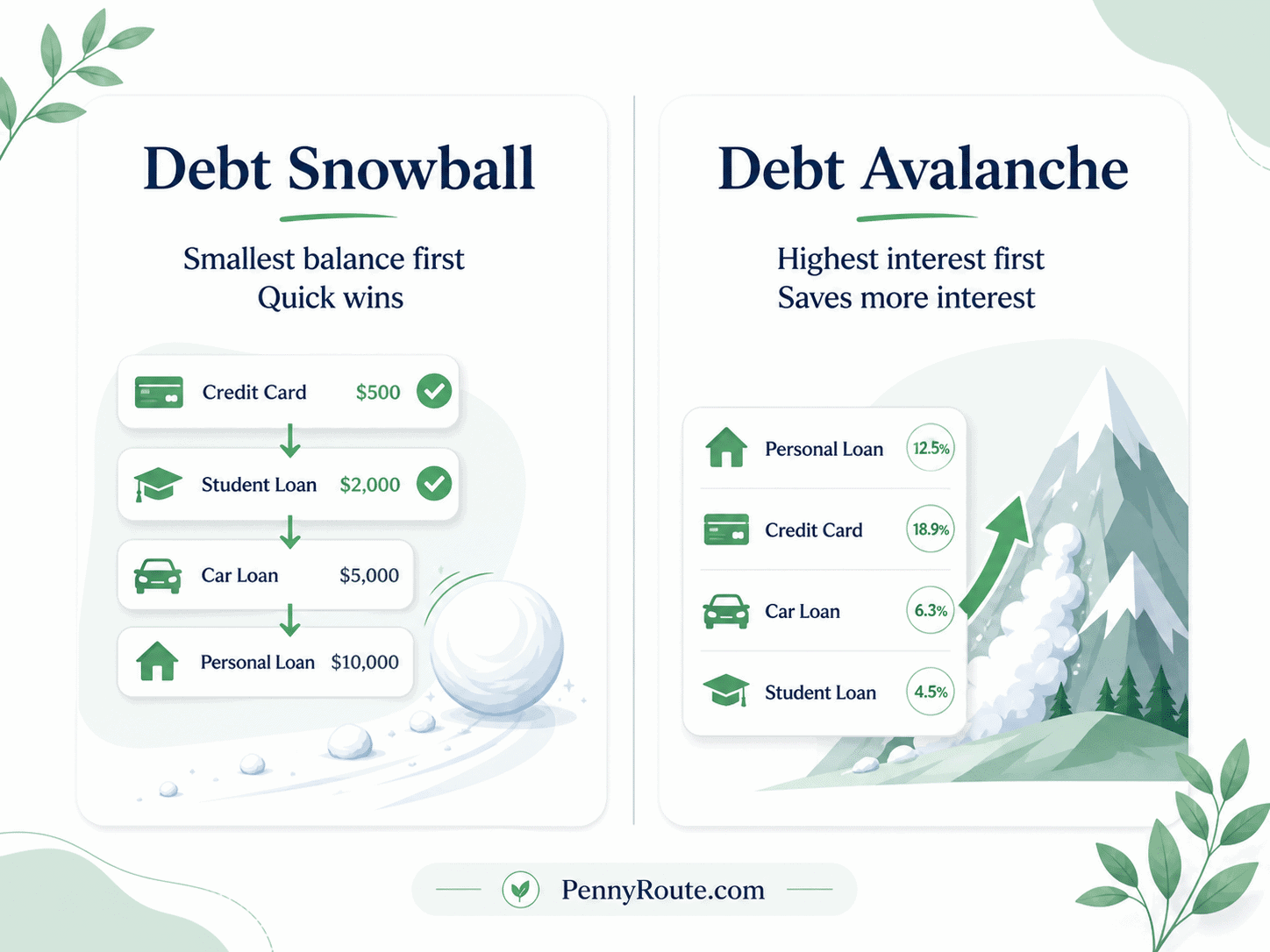

Choose Your Debt Payoff Method

Once your debts are listed, choose one payoff method to guide your plan.

You do not need to switch methods every time you read a new tip. The method is there to help you focus your extra money on one debt at a time instead of spreading it too thin across every balance.

Here are three simple options:

| Method | How It Works | Best For |

|---|---|---|

| Debt snowball | Pay extra toward the smallest balance first while making minimum payments on everything else. | Building motivation with quick wins |

| Debt avalanche | Pay extra toward the highest interest rate first while making minimum payments on everything else. | Saving more on interest over time |

| Hybrid method | Start with one small balance for momentum, then focus on higher-interest debt. | Balancing motivation and interest savings |

The debt snowball method can help if you need a quick win. Paying off a small balance may give you the confidence to keep going.

The debt avalanche method can help if your main goal is to reduce interest costs. This method targets the most expensive debt first.

A hybrid method can work if you want both momentum and savings. For example, you might pay off one small store card first, then switch to the debt with the highest interest rate.

The best method is the one you can stick with. Choose your first target debt, make minimum payments on the rest, and send extra money to that target until it is gone.

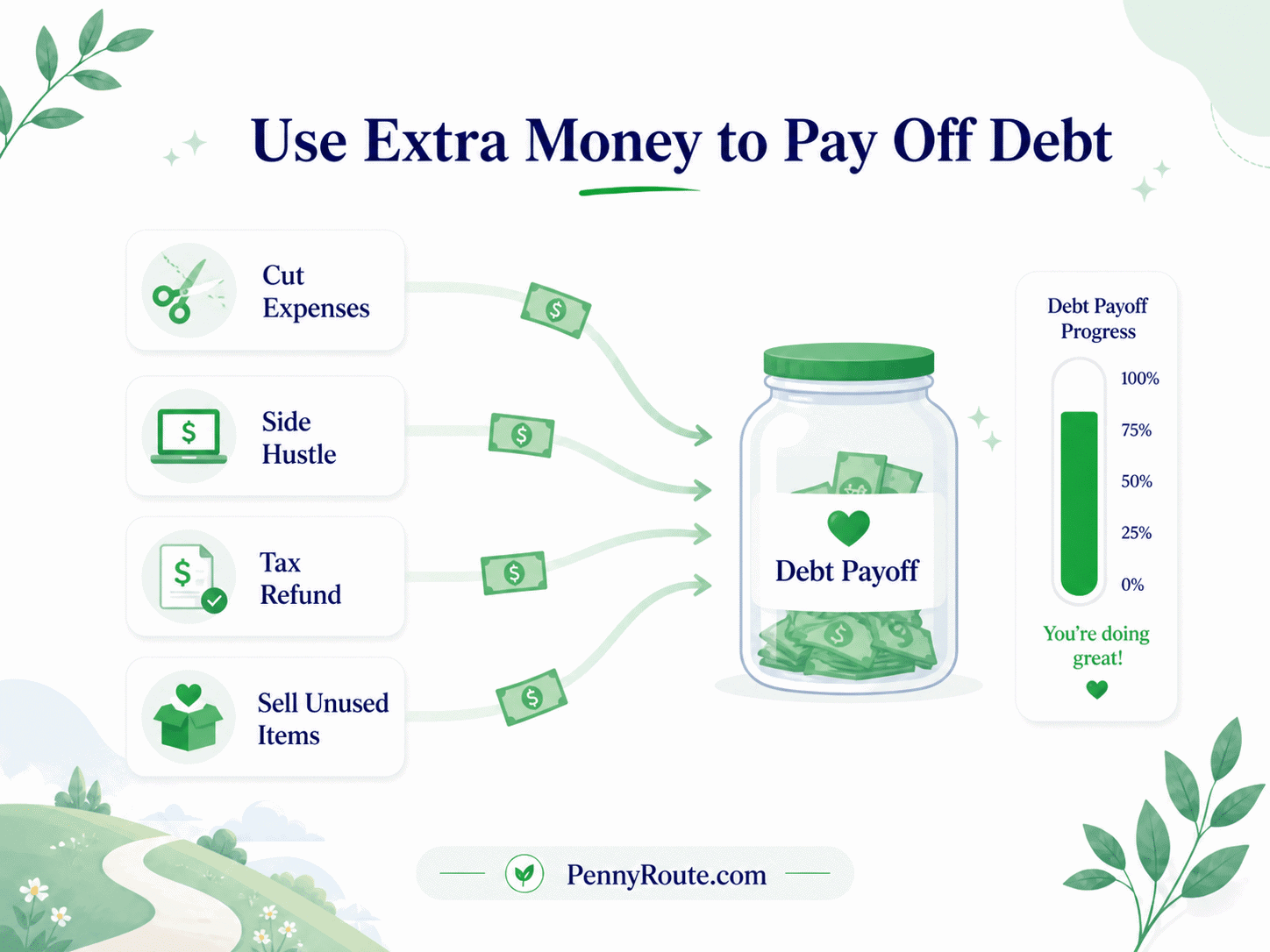

Find Extra Money Without Making Your Budget Miserable

Paying off debt faster usually requires extra money, but that does not mean you need to cut every enjoyable thing from your life.

A plan that is too strict may work for a week or two, then fall apart. Instead, look for small changes you can repeat without making your budget feel impossible.

Start with flexible spending categories, such as:

- eating out

- subscriptions

- entertainment

- clothing

- personal spending

- convenience purchases

- unused memberships

For example, if you reduce takeout spending by $80 a month and cancel a $15 subscription you barely use, that gives you $95 to send toward your target debt. That may not sound dramatic, but over six months, it adds up to $570 before interest savings.

You can also look for temporary ways to bring in extra money, such as selling unused items, picking up extra hours, doing a small side gig, or using cash-back rewards toward debt.

The goal is not to punish yourself. It is to find money that is leaking out quietly and redirect it toward the debt you want gone first.

Pay More Than the Minimum When You Can

Minimum payments help keep your accounts current, but they usually do not move the debt down quickly.

When you pay only the minimum, a larger part of your payment may go toward interest instead of reducing the balance. That is why even small extra payments can help, especially on high-interest debt.

The key is to send extra money to one target debt at a time. Keep making minimum payments on everything else, then put your extra payment toward the debt you chose in your payoff method.

For example, if your minimum payment on a credit card is $75 and you add an extra $50, your total payment becomes $125. That extra $50 can help reduce the balance faster than the minimum payment alone.

Once that credit card debt is paid off, do not let the freed-up payment disappear into normal spending. Roll it into the next target debt. If you were paying $125 toward the first debt, add that amount to the payment on your next target.

This creates momentum. Each paid-off debt gives you more money to put toward the next one.

Related: What to Do If You Can Only Make Minimum Payments on Your Debt

Lower Your Interest Rate Where Possible

A lower interest rate can help more of your payment go toward the balance instead of interest.

This can be especially helpful with credit cards, store cards, or other high-interest debt. Even if your monthly payment stays the same, a lower rate may help the debt shrink faster.

A few options to explore include:

- asking your credit card issuer for a lower interest rate

- transferring a balance to a lower-rate card

- refinancing a loan

- consolidating debt with a lower-interest personal loan

- checking whether a nonprofit credit counselor can help you review options

Before you move debt around, look closely at the details. A balance transfer may charge a fee. A consolidation loan may have a longer repayment term. A lower monthly payment can look helpful, but if the term is much longer, you may not save as much as expected.

Also, avoid using debt consolidation as a way to free up old credit cards for new spending. Moving debt only helps if the new plan lowers your cost, simplifies repayment, or helps you stay consistent.

Lowering interest can be useful, but it is not magic. The real progress still comes from paying more toward the balance and avoiding new debt while you work through the plan.

Avoid Adding New Debt While Paying Off Old Debt

Paying off debt is harder when new balances keep getting added at the same time.

This does not mean you are careless. Sometimes debt grows because the budget is too tight, an emergency happens, or credit cards become the backup plan for groceries, gas, or bills.

Start by looking at why new debt is happening. Is it from unexpected expenses, everyday spending, medical costs, car repairs, or income that does not cover the month? The answer matters because the solution will not be the same for everyone.

If new debt comes from everyday spending, your budget may need clearer limits for flexible categories. If it comes from surprise expenses, even a small emergency fund can help reduce the need to borrow again. If it comes from income not covering essentials, cutting subscriptions may not be enough.

You can also make debt harder to add by removing saved card details from shopping apps, leaving credit cards at home, using a debit card for everyday spending, or setting a short waiting period before nonessential purchases.

The goal is not to never use credit again. It is to stop new balances from quietly undoing the progress you are working hard to make.

Use Extra Money Wisely

Extra money can help you make faster progress if you decide what to do with it before it gets absorbed into normal spending.

This includes money such as:

- tax refunds

- work bonuses

- cash gifts

- side hustle income

- overtime pay

- cash-back rewards

- extra paychecks

- money from selling unused items

You do not have to put every extra dollar toward debt, especially if you also need a small emergency fund or have an important bill coming up. But choosing a plan ahead of time can keep the money from disappearing without much to show for it.

For example, if you receive a $600 tax refund, you might put $400 toward your target debt, $100 into emergency savings, and keep $100 for a planned need. That still moves your debt down without making the rest of your budget feel ignored.

Before you spend extra money, ask one question:

What would help my financial situation most one month from now?

Sometimes the answer is debt payoff. Sometimes it is catching up on a bill, building a small buffer, or covering an upcoming expense so you do not need to borrow again.

When Paying Off Debt Faster May Not Be Enough

Sometimes the problem is bigger than needing a better payoff method.

If you cannot afford minimum payments, rely on credit cards for basic needs, or feel like debt keeps growing no matter what you cut, it may be time to get extra support. That does not mean you failed. It means the situation may need more than a do-it-yourself plan.

Consider getting help if:

- you are missing minimum payments

- you are using credit cards to cover groceries, rent, gas, or utilities

- debt collectors are contacting you

- your balances keep growing even while you make payments

- you are unsure which bills to pay first

- debt payments are making it hard to cover basic needs

A nonprofit credit counselor may help you review your budget, understand your options, and create a repayment plan. You can also contact lenders directly to ask about hardship options, payment plans, or temporary relief.

Be careful with companies that promise fast debt fixes, guaranteed results, or pressure you to stop paying your creditors without explaining the risks. Debt relief options can have fees, credit consequences, and tax considerations, so it is worth reading the details before you agree to anything.

Paying off debt faster is a good goal, but staying safe and current on basic needs matters too. If the numbers are not working, getting help early can prevent the situation from becoming harder to manage.

Try a Simple 30-Day Debt Payoff Starter Plan

If paying off debt feels overwhelming, start with a 30-day plan.

You do not have to fix everything this month. The first goal is to get organized, choose your first target debt, and make one clear move forward.

Week 1: List Your Debts

Gather your balances, interest rates, minimum payments, due dates, and account details. Put everything in one place so you can see the full picture.

Week 2: Choose Your First Target Debt

Pick the debt you want to focus on first. You can use the snowball method for a quick win, the avalanche method to reduce interest, or a hybrid method if you want both motivation and savings.

Week 3: Find One Extra Payment

Look for one realistic way to send extra money to your target debt. That might mean reducing takeout, canceling an unused subscription, selling something you no longer need, or using part of a bonus or refund.

Week 4: Review and Adjust

Check what worked and what felt too hard. If the plan was realistic, repeat it next month. If it felt too tight, adjust the amount instead of quitting completely.

Small progress still counts. One organized month can give you a clearer plan for the next one.

Common Mistakes That Slow Down Debt Payoff

Paying off debt takes time, but a few small mistakes can make the process feel even slower.

Most of these are not dramatic mistakes. They are the kind that happen when you are busy, stressed, or trying to manage too many money goals at once.

Paying Extra on Too Many Debts at Once

Sending a little extra to every debt may feel productive, but it can slow your momentum.

In most cases, it works better to make minimum payments on all debts, then put extra money toward one target debt. This helps you see clearer progress and pay off one balance at a time.

Ignoring Interest Rates

A small balance can feel easier to handle, but a high-interest debt may be costing you more every month.

You do not have to choose the avalanche method, but you should know which debts have the highest rates. That helps you make smarter decisions when extra money is available.

Making the Plan Too Strict

A debt payoff plan that leaves no room for real life can be hard to follow.

If every spare dollar goes to debt and nothing is left for groceries, gas, small surprises, or basic personal spending, the plan may fall apart quickly. A realistic plan you can repeat is usually better than an intense plan you quit after two weeks.

Forgetting About Irregular Expenses

Debt payoff gets harder when annual bills, car repairs, medical costs, or holidays surprise your budget.

Try to set aside small amounts for irregular expenses while paying off debt. This can help you avoid using credit again when predictable costs show up.

Adding New Debt Without Noticing

New debt can quietly erase the progress you are making.

Check whether credit cards are still covering everyday spending, subscriptions, or unexpected costs. If new balances keep appearing, pause and fix the reason before pushing harder on extra payments.

Quitting After a Slow Month

Some months will be slower than others.

A lower extra payment, an unexpected bill, or a missed goal does not erase your progress. Review what happened, adjust the plan, and keep going with the next payment you can make.

Should You Save Money or Pay Off Debt First?

Saving money and paying off debt are both important, so it can be hard to know which one should come first.

A simple approach is to start with a small emergency fund while still making minimum payments on every debt. Even a small buffer can help you avoid using credit again when an unexpected bill, car repair, or medical cost shows up.

After that, you can focus more extra money on debt payoff, especially if you have high-interest debt. Credit cards and store cards can grow quickly when interest is high, so paying them down may save you money over time.

That does not mean you should ignore savings completely. If every extra dollar goes to debt and you have no backup, one surprise expense can push you right back into borrowing.

A balanced plan might look like this:

- make minimum payments on all debts

- build a small starter emergency fund

- send extra money to your target debt

- keep setting aside small amounts for irregular expenses

- increase savings once high-interest debt is under control

If your debt has very low interest, or if your income is unstable, saving a larger buffer may matter more. If your debt has very high interest, paying it down faster may be the stronger move.

The best choice is the one that helps you reduce debt without leaving your budget so fragile that one surprise knocks you backward.

Helpful Debt Payoff Resources

You do not have to figure out every debt decision alone.

If you want extra guidance, start with trustworthy resources that explain your options clearly and avoid pressure. Debt payoff advice can affect your budget, credit, and long-term finances, so it is worth using sources that are educational and careful.

Here are a few helpful places to start:

- Federal Trade Commission: How to Get Out of Debt

- Consumer Financial Protection Bureau: How to Reduce Your Debt

- Consumer Financial Protection Bureau: Debt Collection

These resources can help you understand debt payoff methods, credit counseling, debt collectors, and warning signs to watch for before choosing a debt relief option.

Use them as support, not as another reason to delay action. Even one clear next step, such as listing your debts or calling a lender, can help you move forward.

Start With One Debt and One Clear Plan

Paying off debt faster does not mean you need to fix everything at once.

Start by listing what you owe, choosing one target debt, and finding one realistic extra payment you can repeat. That may feel small at first, but small payments become more powerful when they are focused and consistent.

Your plan may need adjusting as your income, bills, or expenses change. That is normal. A useful debt payoff plan should fit real life, not fall apart the first time something unexpected happens.

Pick your first target, make the minimum payments on everything else, and send what extra money you can toward that one debt. One paid-off balance can give you the momentum to keep going.

FAQs About Paying Off Debt Faster

What is the fastest way to pay off debt?

The fastest practical way to pay off debt is to make minimum payments on every account, choose one target debt, and put all extra money toward that debt until it is paid off. You can use the debt avalanche method to reduce interest or the debt snowball method to build momentum.

Is it better to pay off the smallest debt or highest interest debt first?

Paying off the smallest debt first can help you build motivation quickly. Paying off the highest-interest debt first may save more money over time. The better choice depends on whether you need quick wins or want to focus mainly on interest savings.

Should I pay off debt or save money first?

It usually helps to build a small emergency fund while making minimum debt payments. After that, you can send more extra money toward high-interest debt while still keeping some savings for unexpected expenses.

How can I pay off debt faster with low income?

Start by listing every debt, making minimum payments, and choosing one target debt. Then look for small repeatable changes, such as reducing flexible spending, lowering bills, selling unused items, or adding temporary income where possible.

Does paying more than the minimum help?

Yes. Paying more than the minimum can reduce your balance faster and may lower the total interest you pay, especially on high-interest debt. Even small extra payments can help when you apply them consistently to one target debt.

What should I do if I cannot afford my minimum payments?

If you cannot afford minimum payments, contact your lenders, review hardship options, and consider speaking with a nonprofit credit counselor. Avoid companies that promise quick debt fixes without clearly explaining fees, risks, and possible credit consequences.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.