Paying down a credit card is frustrating when new charges keep showing up on the same card. You make a payment, the balance drops for a moment, then groceries, gas, subscriptions, or another bill pushes it back up again.

Stopping new charges can make your payoff plan clearer and easier to trust. Instead of feeling like your payment disappeared, you can start separating everyday spending from the debt you are trying to reduce.

The first step is not to fix every money habit at once. It is to pause the cycle, change how you pay for daily expenses, and give your credit card balance a real chance to go down.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

Quick Overview: How to Stop Using Credit Cards While Paying Off Debt

- Stop new credit card charges before trying to speed up your payoff plan.

- Remove saved credit cards from shopping apps, browsers, digital wallets, and subscriptions.

- Use debit, cash, or a separate checking account for daily spending.

- Move bills off your credit card slowly so you do not create overdrafts or missed payments.

- Build a small buffer so every surprise expense does not go back on the card.

- Keep making at least the minimum payment while you work on the spending system.

- If you slip and use the card again, fix the trigger instead of giving up.

Why Paying Off Credit Cards Is Hard When You Keep Using Them

Credit card payoff becomes harder when the same card is doing two jobs at once.

One part of the card is debt you are trying to reduce. The other part is still being used for groceries, gas, subscriptions, takeout, bills, or small purchases that seem harmless in the moment.

That creates a frustrating cycle:

- You make a payment.

- The balance goes down.

- New charges are added.

- The balance climbs back up.

- It becomes hard to tell whether your plan is working.

This does not always mean you are being careless. Sometimes the card has become your backup plan because your checking account is tight, bills are uneven, or everyday costs are higher than expected.

The problem is that new charges hide your progress. Even if you are making payments, the balance may not move much because your card is still covering current spending.

Before you focus on paying the balance faster, it helps to stop the balance from growing. That gives every payment a clearer job.

It also helps to understand how to avoid paying interest on a credit card, especially if new purchases keep landing on the same account.

Start by Pausing New Charges, Not Closing the Card

The first step is usually to pause new charges, not rush to close the credit card.

Closing a card may sound like the fastest way to stop using it, but it can have side effects. It may affect your available credit, credit utilization, or account history. For many people, the safer first move is to make the card harder to use while keeping the account open.

You can start with simple changes:

- Take the card out of your wallet.

- Lock the card in your card issuer’s app if that option is available.

- Put the physical card somewhere inconvenient but safe.

- Turn off one-click checkout where the card is saved.

- Stop using the card for new purchases while you focus on paying it down.

This creates a pause between you and the card. That pause matters because credit cards are often easy to use before you have time to think through the purchase.

You are not trying to make a dramatic decision in one day. You are trying to stop the balance from growing while you decide the next practical step.

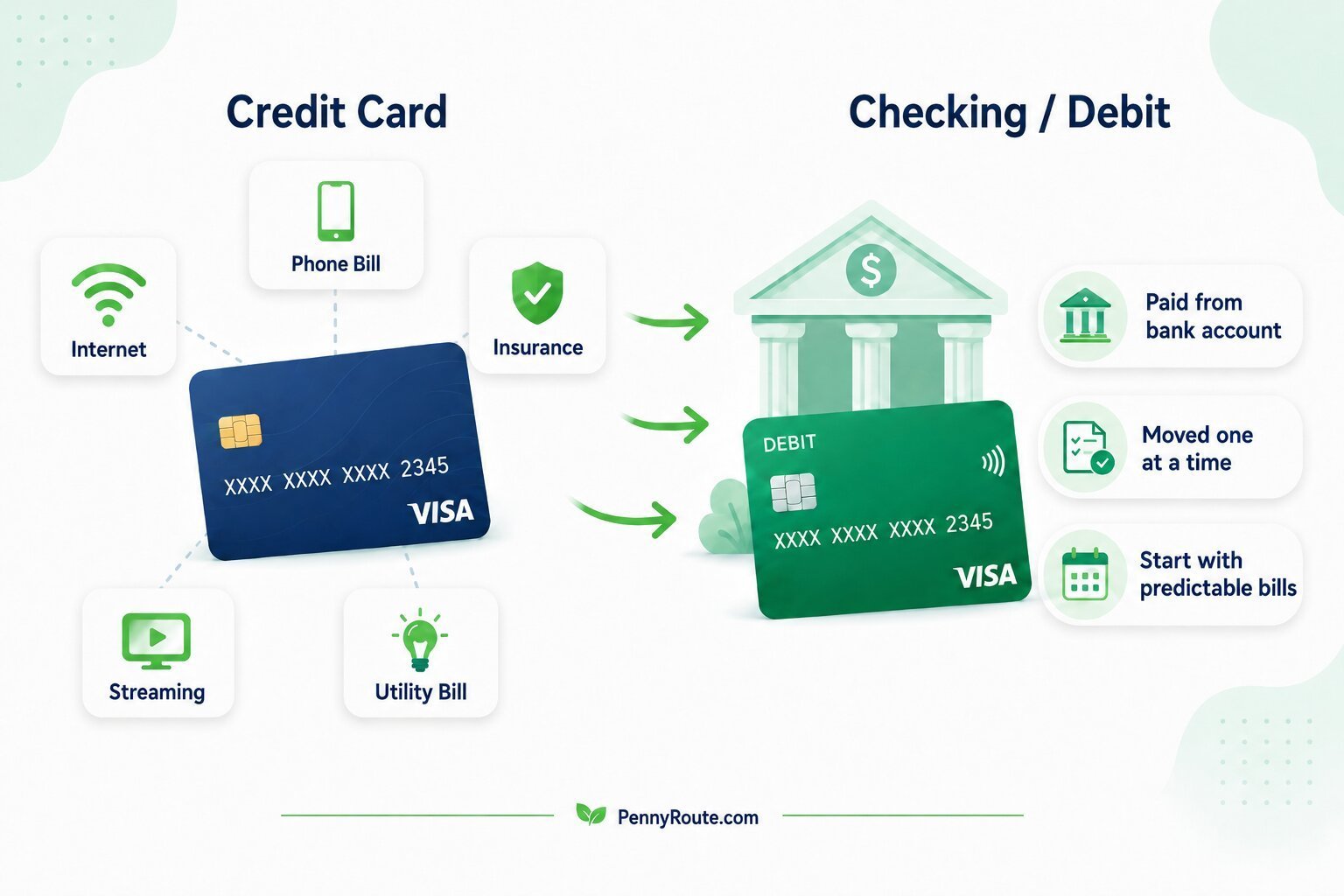

Replace Credit Card Spending With a New Payment System

Once the card is paused, you need another way to pay for everyday life.

This is the part many people skip. They decide to stop using credit cards, but groceries, gas, online orders, and small purchases still need a payment method. Without a replacement system, the card usually comes back out.

Start by removing saved credit cards from places where purchases happen quickly:

- Shopping apps

- Food delivery apps

- Grocery apps

- Ride-share apps

- Digital wallets

- Browser autofill

- Subscription accounts

- Online stores you use often

Then choose a new payment method for daily spending. That may be a debit card, cash, or a separate checking account used only for flexible expenses.

For example, you might move grocery and gas spending to debit, then use cash for categories where you tend to overspend. Or you might keep a separate “spending money” account so bill money does not get mixed with everyday purchases.

When the card is no longer saved everywhere, each purchase takes a little more thought. That extra pause can help you stay with the plan.

Make a Plan for Bills That Are Charged to Credit Cards

Daily spending is one part of the credit card cycle. Bills are another.

Many people keep using credit cards because important payments are already attached to the card. That might include phone bills, internet, insurance, utilities, streaming services, memberships, or subscription boxes you forgot existed. Those “small” automatic charges can quietly keep the balance from going down.

Start by listing every bill and subscription currently charged to the card. Check your last one or two statements so you do not miss anything.

Then sort them into three groups:

- Must keep: bills you need, such as insurance, phone, internet, or utilities

- Can pause or cancel: subscriptions, memberships, or services you do not use enough

- Can move later: bills that are important but may need to wait until your checking account has enough room

Do not move every bill at once if it could cause overdrafts or missed payments. Start with one predictable bill you can safely pay from checking or debit.

For example, you might move a $40 phone bill first, then wait a paycheck before moving another bill. This keeps the change manageable and helps you avoid replacing credit card debt with bank fees.

The purpose is not to create a perfect bill system overnight. It is to slowly stop automatic charges from rebuilding the balance you are trying to pay down.

Build a Small Buffer So the Card Is Not Your Backup Plan

Credit cards often become the backup plan when there is no extra room in checking.

A small buffer can help change that. It does not need to be a full emergency fund at first. Even a small amount set aside can keep one unexpected expense from going straight back on the card.

Start with a realistic target, such as $100, $250, or $500. The amount matters less than creating a little space between a surprise bill and your credit card.

You can use this buffer for small, necessary expenses like:

- Gas before payday

- A prescription

- A minor car repair

- A higher utility bill

- A school or work expense

- A small household repair

Keep this money separate from your credit card payment. If you send every spare dollar to the card and then need to use the card again two days later, your payoff plan can turn into a loop.

A small buffer gives your payments a better chance to stay paid. When the card is no longer your first backup option, the balance has more room to go down.

What If You Need the Credit Card for Essentials?

If you are using a credit card for groceries, gas, medicine, or basic bills, the problem may not be willpower. It may be a cash-flow problem.

In that situation, do not ignore your basic needs just to avoid using the card. Food, housing, utilities, transportation, insurance, and basic medical needs still come first.

Start by looking at what the card is covering. Is it filling a temporary gap, or has it become part of your monthly survival plan?

If it is temporary, you may need a short reset: reduce flexible spending, move one bill, or build a small buffer before payday.

If it happens every month, the issue may be bigger than credit card use. Your income, fixed expenses, debt payments, or bill timing may need a closer review.

If minimum payments are becoming hard to manage, the CFPB recommends contacting your credit card company before you miss a payment. Ask what options may be available based on what you can afford.

Needing a credit card for essentials is not something to be ashamed of. But it is a signal to slow down, protect the basics, and look for a safer plan before the balance grows further.

Keep Paying the Card While You Stop Using It

Stopping new charges does not mean ignoring the credit card balance.

If you can, keep making at least the minimum payment on time. Minimum payments help keep the account current and reduce the chance of late fees, penalty rates, or missed-payment problems.

After the minimum payment is covered, be careful with extra payments. Paying extra is helpful, but only if it does not leave you short for groceries, gas, rent, or bills before the next paycheck.

For example, sending an extra $200 to your credit card may seem like progress. But if that leaves your checking account too low and you need to charge groceries two days later, the payment may not really move you forward.

A safer approach is to cover essentials first, keep the card current, set aside a small buffer if you can, and then send extra money to the card. That way, your payment is less likely to come right back as a new charge.

What to Do If You Slip and Use the Card Again

Using the card once after you decided to stop does not erase your progress.

It simply gives you information. Look at what happened and ask a practical question: what made the card the easiest option in that moment?

Maybe the card was still saved in an app. Maybe your checking account was too tight before payday. Maybe a bill came earlier than expected. Maybe it was an impulse purchase that happened before you had time to think.

Once you know the trigger, fix the system around it.

If the card was saved in an app, remove it. If groceries went on the card because checking was low, adjust the grocery budget or build a small buffer. If a bill surprised you, add it to your calendar before the next due date.

If you can, pay off that new charge quickly so it does not blend into the old balance. Then return to the plan with the next purchase.

A 7-Day Reset to Stop Using Credit Cards

You do not need to change every money habit at once. A short reset can help you break the automatic card-use pattern and see where the biggest triggers are.

Day 1: Take the Card Out of Easy Reach

Remove the card from your wallet or lock it in your card issuer’s app if that option is available.

You are not making a forever decision. You are creating space between the urge to spend and the card itself.

Day 2: Remove Saved Card Details

Delete the card from shopping apps, food delivery apps, digital wallets, browser autofill, and online stores you use often.

Saved cards make spending too easy. Removing them adds a small pause before checkout, which can be enough to stop unnecessary charges.

Day 3: Choose One Spending Category to Move

Pick one category that usually ends up on the card, such as groceries, gas, takeout, or household items.

Move that category to debit, cash, or a separate spending account for the week.

Day 4: List Bills Charged to the Card

Check your recent statements and write down every bill, subscription, and automatic payment attached to the card.

Do not move everything yet. Just get the full list so you know what is keeping the card active.

Day 5: Move One Predictable Bill

Choose one bill you can safely move to checking or debit without causing an overdraft.

Start small if needed. Moving one bill is still progress because it reduces the amount automatically going back onto the card.

Day 6: Create One Clear Card Rule

Choose one rule that is easy to remember.

For example:

- No credit card for groceries while carrying a balance

- No credit card for takeout

- No credit card for “I’ll pay it back Friday” purchases

- No credit card for shopping apps

A simple rule works better than a complicated system you forget by Wednesday.

Day 7: Review What Triggered Card Use

Look back at the week and notice what made you want to use the card.

Was it convenience? A bill? A low checking balance? An impulse purchase? A real emergency?

That answer tells you what to fix next. The reset is not about proving you can be perfect for seven days. It is about finding the weak spot in the system and making it easier to avoid new charges.

Stop the New Charges Before Chasing Faster Payoff

Paying off credit card debt becomes more manageable when new charges stop replacing your progress.

Before you worry about the perfect payoff method, focus on one clear goal: keep the balance from growing. That might mean removing saved cards, moving one bill to checking, using debit for groceries, or building a small buffer before sending extra money to the card.

Small changes can make a real difference because they give your payments a chance to stay on the balance instead of disappearing under new purchases.

You do not need to fix the whole cycle in one day. Start with one spending category, one bill, or one card rule. Once new charges slow down, your payoff plan has more room to work.

FAQs About Stopping Credit Card Use While Paying Off Debt

Should I stop using credit cards while paying them off?

Usually, yes. If new charges keep replacing your payments, pausing credit card use can make your payoff progress easier to see. You do not have to close the card right away. Start by removing it from everyday spending and using debit, cash, or a separate checking account instead.

Should I close my credit card to stop using it?

Not always. Closing a credit card can affect your available credit, credit utilization, and account history. A safer first step may be to remove the card from your wallet, delete it from apps, or lock it in the issuer’s app if that option is available.

How do I stop using credit cards for bills?

Start by listing every bill and subscription charged to the card. Then move one bill at a time to checking or debit. Do not move everything at once if it could cause overdrafts or missed payments. Start with one predictable bill you can safely cover.

What if I need credit cards for groceries or gas?

Protect basic needs first. If groceries, gas, or medicine are going on the card every month, the issue may be cash flow, not just card use. Review your income, expenses, minimum payments, and bill timing. If minimum payments are becoming hard to manage, contact your card issuer or consider qualified help before the balance grows further.

How do I stop going back into credit card debt?

Remove easy access to the card, move daily spending to debit or cash, build a small buffer, and create clear rules for when the card is off-limits. Once the card is no longer your backup plan for everyday spending, your payments have a better chance to reduce the balance.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.