Saving money fast is not always simple when bills are waiting, groceries cost more than expected, and payday still feels too far away.

But saving does not have to mean cutting every small comfort or turning your life into a financial obstacle course. Most of the time, the fastest progress comes from finding the places where money is quietly slipping away, then fixing those first.

That might be an unused subscription, last-minute takeout, a bill you have not reviewed in years, or small purchases that do not feel expensive until they repeat all month.

The goal is not to become perfect with money overnight. It is to create a little breathing room, protect the money you free up, and make your next few weeks feel easier than the last.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

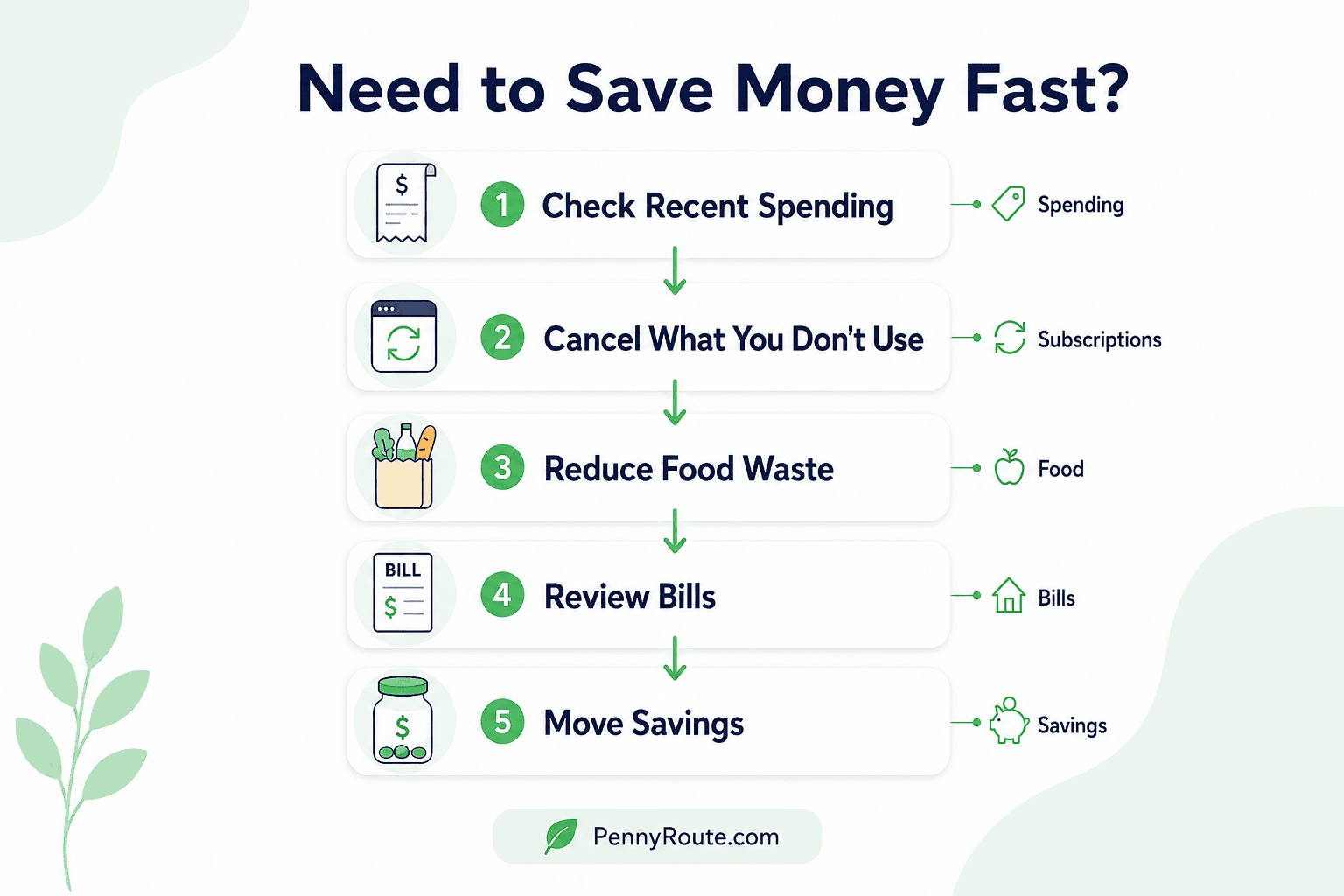

Quick Overview: How to Save Money Fast

- Review your recent spending so you know where your money is going.

- Cancel unused subscriptions, free trials, and duplicate services.

- Reduce last-minute takeout by keeping a few easy meals at home.

- Compare recurring bills like phone, internet, insurance, and utilities.

- Use a pause rule before buying non-essential items.

- Avoid buying things only because they are on sale.

- Keep a small amount for fun so saving does not feel like punishment.

- Move the money you free up into savings before it disappears into other spending.

Start With Where Your Money Is Going

Before you cut anything, look at where your money is actually going.

You do not need a complicated spreadsheet for this. Open your bank account, credit card statement, or payment app and review the last 7 to 30 days. The goal is not to judge every purchase. It is simply to spot patterns.

Group your spending into a few basic categories:

- fixed bills, like rent, loan payments, insurance, or phone bills

- flexible spending, like groceries, gas, dining out, and household items

- extra spending, like shopping, subscriptions, delivery fees, and small impulse purchases

This quick review helps you see which expenses are creating the most pressure.

For example, you may notice that your grocery bill is reasonable, but food delivery is adding up. Or your shopping is fine, but three old subscriptions are still charging your card every month. Sometimes the problem is not one large purchase. It is several small charges quietly working together.

If you are trying to make a budget, this step gives you the real numbers to work with. Guessing usually makes saving harder because you may cut the wrong thing and leave the real money leak untouched.

Start with the spending you repeat often. That is usually where the fastest savings are hiding.

You do not need a complicated spreadsheet for this. Open your bank account, credit card statement, or payment app and review the last 7 to 30 days. The goal is not to judge every purchase. It is simply to track your spending and spot patterns.

Cut the Expenses You Won’t Miss First

The easiest expenses to cut are the ones you barely use, forgot about, or do not care about anymore.

This is a better place to start than cutting something you actually enjoy. If you cancel every small comfort right away, saving money starts to feel like punishment. That usually does not last.

Look for expenses like:

- unused subscriptions

- free trials that turned into paid plans

- duplicate streaming services

- app upgrades you forgot about

- delivery memberships you rarely use

- bank fees or account fees

- memberships you keep “just in case”

- small impulse buys you regret later

A $9.99 subscription may not seem like much, but three or four forgotten subscriptions can quietly take money every month. Canceling them is a quick win because you only have to make the decision once.

Also check for duplicate services. You may not need multiple streaming platforms, cloud storage plans, meal delivery memberships, or fitness apps at the same time.

The point is not to remove everything enjoyable. It is to stop paying for things that no longer earn their place in your budget.

Reduce Food Spending Without Making Meals Complicated

Food is one of the easiest places to overspend because it shows up in so many small ways: groceries, snacks, work lunches, delivery fees, coffee runs, and last-minute takeout.

You do not need a perfect meal plan to save money here. Start by making food decisions a little easier before you are tired, hungry, or already scrolling through delivery apps.

Keep a Few Easy Meals at Home

The most useful meals are not always the fancy ones. They are the meals you can make when you have no energy left.

Keep a few simple options ready, such as:

- pasta and sauce

- eggs and toast

- rice bowls

- soup and sandwiches

- frozen vegetables with a quick protein

- wraps, quesadillas, or baked potatoes

These meals do not need to win an award. They just need to stop a $12 problem from becoming a $40 takeout order.

Shop With a Short List

A short grocery list helps you avoid random purchases and forgotten ingredients.

Before you shop, check what you already have in the fridge, freezer, and pantry. Then write down only what you need for the next few days or the week ahead.

This keeps grocery shopping practical, not overwhelming. You are not trying to plan every bite of food like a restaurant manager. You are just giving yourself enough structure to avoid buying food that goes unused.

Use What You Already Have First

Before buying more groceries, look for food you can use up.

Check for:

- leftovers

- frozen meals or ingredients

- canned goods

- pasta, rice, oats, or other staples

- vegetables that need to be used soon

- snacks you forgot you had

This helps reduce food waste and gives you a small break from spending.

Cut Takeout Triggers

Takeout usually happens for a reason.

Maybe you are tired after work. Maybe there is nothing easy at home. Maybe you forgot to pack lunch. Maybe grocery shopping got pushed back again.

Instead of saying “I’ll never order takeout,” look for the trigger behind it. If the problem is tired weeknights, keep two easy dinners ready. If lunch is the issue, pack something simple the night before. If errands run late, keep a backup meal at home.

Saving money on food is much easier when your plan works on real days, not just perfect ones.

Review Monthly Bills and Recurring Payments

Some of the best savings come from bills you only need to review once.

That is why recurring payments are worth checking carefully. They may not feel like everyday expenses, but they quietly shape how much money is left every month.

Look at bills and payments such as:

- phone plans

- internet

- insurance

- utilities

- streaming services

- gym memberships

- storage units

- app subscriptions

- bank account fees

- credit card annual fees

Start with anything you have not reviewed in a while. Phone plans, internet packages, and insurance policies often change over time, and you may be paying for more than you actually need.

For example, you might be paying for extra phone data you barely use, a faster internet plan than your household needs, or a membership you keep meaning to cancel. None of these decisions are dramatic, but fixing them can free up money every month.

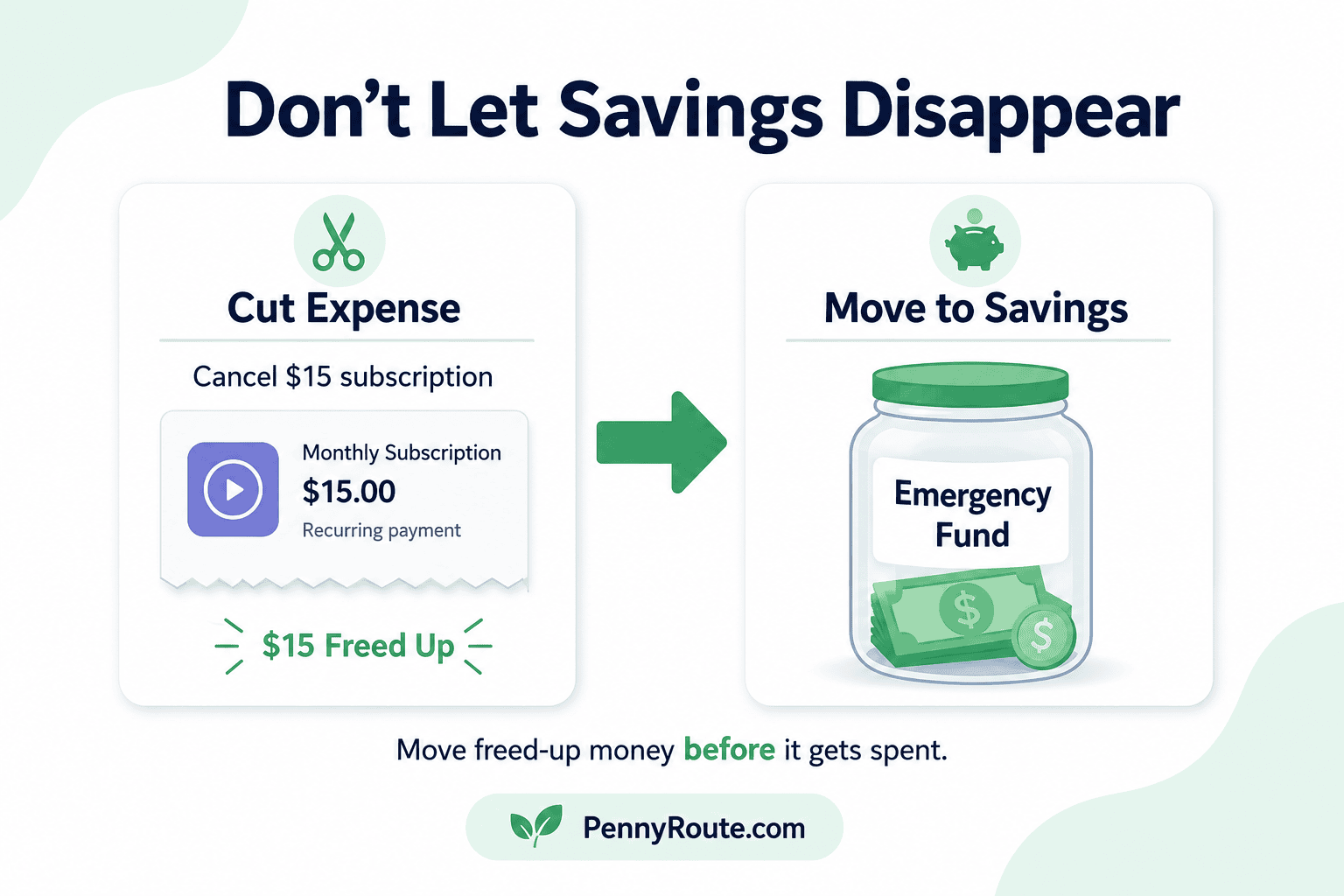

The best part about lowering a recurring bill is that the savings can keep showing up. Canceling a $15 service or reducing a $30 bill does not just help today. It can make next month easier too.

Use a Pause Rule Before Buying

Impulse purchases are sneaky because they often make sense in the moment.

You see something useful, cute, discounted, or “almost sold out,” and your brain starts building a case for why you need it right now. Then a few days later, the excitement is gone and the charge is still there.

A pause rule gives you space before spending.

For small non-essential purchases, wait 24 hours before buying. For bigger purchases, wait a few days or even a week. If you still want the item and it fits your budget, you can buy it with a clearer head.

Try asking yourself:

- Do I still want this tomorrow?

- Will I actually use it often?

- Am I buying this because I need it, or because I am bored or stressed?

- Is this replacing something, or just adding more clutter?

- Would I still buy it if it were not on sale?

A wishlist can help too. Instead of checking out immediately, save the item and come back later. Many purchases lose their magic once they sit in the wishlist for a while.

This does not mean you can never buy anything fun. It just helps you stop buying things you don’t need before small “treat yourself” moments turn into a budget problem.

Save Money on Shopping Without Buying Cheap Junk

Saving money does not always mean buying the cheapest option.

Sometimes the cheapest item breaks faster, wears out sooner, or needs to be replaced so often that it costs more in the long run. The better goal is to spend less on the things that do not matter much, and spend wisely on the things you use often.

Compare Prices Before You Buy

Before buying something non-essential, do a quick price check.

This is especially useful for household items, clothes, electronics, school supplies, and larger purchases. You do not need to spend an hour comparing every tiny item, but a quick search can help you avoid paying more than necessary.

Also check whether the lower price comes with extra shipping fees, lower quality, or a return policy that makes the deal less useful.

Use Unit Prices for Everyday Items

For groceries and household basics, the bigger package is not always the better deal.

Check the unit price when possible. This shows the cost per ounce, pound, liter, item, or similar measurement. It helps you compare different sizes and brands more fairly.

This works well for items like rice, pasta, toilet paper, detergent, cereal, snacks, and cleaning products.

For groceries and household basics, the bigger package is not always the better deal. Check the unit price when possible. This shows the cost per ounce, pound, liter, item, or similar measurement and helps you compare unit prices more fairly.

Buy Generic When Quality Is Similar

Generic or store-brand products can be a simple way to save money, especially for basics.

Try them for items where the brand does not matter much to you, such as pantry staples, cleaning supplies, paper products, basic medicine, and simple household items.

You do not have to switch everything. If there is a brand you genuinely prefer and use often, keep it. Save on the things where you barely notice the difference.

Be Careful With Sales

A sale only saves money if you were already planning to buy the item.

It is easy to buy something just because it is 40% off, but spending money on something you do not need is still spending money. Before buying a sale item, ask whether you would still want it at full price.

If the answer is no, the discount may be doing more convincing than the item itself.

Buy Secondhand When It Makes Sense

Some things are worth buying secondhand, especially when they do not need to be brand new.

This can include furniture, books, kids’ items, basic tools, small appliances, clothes, sports gear, and home office items.

Check the condition carefully and avoid buying used items where safety, hygiene, or warranties matter more. A secondhand bargain is only helpful if it actually works for your needs.

Spend More Carefully on Items You Use Often

For things you use every day, the cheapest option is not always the smartest.

Shoes, mattresses, work bags, winter coats, cookware, and basic tools are examples where quality may matter. Spending a little more on something durable can be better than replacing a low-quality version again and again.

The point is not to buy luxury. It is to avoid cheap purchases that quietly become expensive.

Lower Everyday Household Costs

Everyday household costs are not always large, but they repeat often enough to matter.

This includes things like electricity, water, cleaning supplies, laundry, paper products, toiletries, and small home items you buy without thinking too much about them.

Start with simple changes that do not make daily life harder.

Use What You Already Have

Before buying more household items, check what is already in your cabinets, drawers, closets, or storage bins.

You may find extra soap, toothpaste, cleaning spray, batteries, light bulbs, trash bags, or paper products hiding in places you forgot about. Using what you already own gives your budget a small break and helps avoid duplicate purchases.

Make Household Supplies Last Longer

Small habits can help stretch common household items.

Use the right amount of laundry detergent instead of pouring extra “just to be safe.” Reuse cleaning cloths instead of reaching for paper towels every time. Finish one product before opening another.

None of this needs to become extreme. The goal is simply to stop replacing things faster than necessary.

Reduce Energy and Water Waste

Simple home habits can also lower monthly costs.

Turn off unused lights, run full laundry loads, avoid letting water run during small tasks, and fix small leaks quickly. If your utility costs have been rising, a few practical changes can help you save on utility bills without making your home uncomfortable.

Avoid Buying Home Items on Autopilot

Household purchases can become automatic.

You see a cleaning product, storage basket, candle, kitchen gadget, or pack of “just in case” items and toss it into the cart. It may not seem like much, but these small extras can add up.

Before buying, ask:

- Do I already have something similar?

- Will I use this soon?

- Is this solving a real problem?

- Am I buying this because it is useful, or because it looks nice in the moment?

Your home does not need more stuff just because a store shelf made a good argument.

Try a No-Spend Day or Low-Spend Week

A no-spend day can help you save money fast because it gives your wallet a short break.

This does not mean skipping bills, groceries, medicine, transportation, or anything essential. It simply means pausing non-essential spending for a day, a weekend, or a full week if that feels realistic.

During a no-spend day, you might:

- eat meals from food you already have

- make coffee or snacks at home

- use free entertainment

- delay online shopping

- avoid browsing stores “just to look”

- skip delivery fees and convenience purchases

A low-spend week is a softer version. Instead of spending nothing, you choose a small limit for extras and make the most of what you already have.

For example, you might decide:

“This week, I’ll use pantry meals, avoid takeout, and only spend on essentials.”

This works well when you need quick breathing room before payday or want to reset after a higher-spending week.

The goal is not to prove how little you can survive on. It is to notice how often money leaves your account out of habit, boredom, or convenience.

Make the Savings Actually Count

Cutting an expense is helpful, but the money can disappear quickly if you do not give it a job.

For example, if you cancel a $15 subscription but leave the extra $15 sitting in your checking account, it may get absorbed by snacks, delivery fees, or another small purchase before you notice it. Technically, you reduced an expense. But you may not actually save the money.

When you free up money, move it somewhere on purpose.

That could mean sending it to:

- a savings account

- an emergency fund

- a debt payment

- a bill that is coming due

- a separate “buffer” account for small surprises

Even small amounts count. If you save $10 on takeout, $15 from a canceled subscription, and $20 from a lower phone bill, that is $45 you can move before it blends into the rest of your spending.

This step matters most when money is tight. If you are trying to budget on a low income, protecting small savings can help you create a little breathing room instead of watching every extra dollar vanish by the end of the month.

The easiest method is to transfer the money as soon as you save it. Cancel a subscription? Move that amount. Spend less on groceries this week? Move part of the difference. Get a lower bill? Send the savings before the month finds another use for it.

Saving money fast is not just about spending less. It is about keeping the money you worked to free up.

What Not to Do When Trying to Save Money Fast

When you want quick savings, it is tempting to cut everything at once. That might work for a few days, but it can also create stress, missed payments, or rebound spending later.

A better approach is to save money without making your life harder than it needs to be.

Don’t Skip Essential Bills

Skipping rent, utilities, insurance, loan payments, or minimum debt payments can create bigger problems than the money you save in the moment.

Late fees, service interruptions, credit damage, or penalty charges can make things more expensive later. If a bill is hard to pay, contact the provider before the due date and ask about payment plans, hardship options, or due date changes.

Don’t Cut Every Enjoyable Thing

Saving money should not feel like a punishment.

If you remove every small thing you enjoy, you may end up frustrated and spend more later. Keep one or two affordable treats that genuinely matter to you, then cut the spending you barely notice or often regret.

That might mean keeping a weekly coffee with a friend but canceling unused subscriptions. Or keeping one streaming service while pausing the others.

Don’t Buy Something Just Because It Is on Sale

A discount is not savings if you were not planning to buy the item.

Sales, coupon codes, limited-time offers, and cashback deals can make spending feel responsible, even when it is still unnecessary. Before buying, ask whether you would want the item without the discount.

If the sale is the main reason you want it, waiting is usually the better move.

Don’t Focus Only on Tiny Expenses

Small expenses matter when they repeat often, but do not ignore larger bills.

Canceling a $5 subscription helps, but reviewing a phone, internet, insurance, or utility bill may free up more money. Look at both: the small spending leaks and the bigger recurring costs.

Fast savings usually come from fixing a few repeat expenses, not from obsessing over every tiny purchase.

Don’t Use Cashback as an Excuse to Spend

Cashback apps, rewards points, and coupons can be useful when they reduce the cost of something you already planned to buy.

But they are not helpful if they convince you to spend more. Earning $3 back on a $60 purchase you did not need is still a $57 problem.

Use rewards as a bonus, not a reason to shop.

Don’t Make Risky Money Moves for Quick Cash

Be careful with payday loans, high-interest borrowing, skipping insurance, draining emergency savings for non-urgent spending, or selling things you will need to replace soon.

Quick savings should give you more breathing room, not create a bigger financial mess next month.

FAQs About Saving Money Fast

What is the fastest way to save money?

The fastest way to save money is to cut expenses you can reduce right away, such as unused subscriptions, free trials, delivery fees, impulse purchases, takeout, and bills you may be overpaying for.

Once you free up money, move it to savings quickly so it does not disappear into other spending.

How can I save money when I live paycheck to paycheck?

Start by focusing on small changes you can make this week. Review recent spending, pause non-essential purchases, use food you already have, and cancel anything you do not use.

If money is very tight, aim for a small buffer first. Even $5 or $10 set aside can help with the next small surprise.

How can I save $100 quickly?

To save $100 quickly, combine a few small changes: cancel unused subscriptions, skip takeout for a week, use pantry meals, pause shopping, return something you do not need, or lower one recurring bill.

You do not need one perfect $100 fix. A few $10, $20, and $30 changes can get you there.

What expenses should I cut first?

Cut expenses you do not use, do not value, or often regret. Good examples include unused subscriptions, duplicate services, free trials, bank fees, delivery fees, and impulse purchases.

After that, review bigger recurring bills like phone, internet, insurance, and utilities.

Is it better to cut small expenses or big bills?

Both can help. Small expenses matter when they repeat often, while big bills can create larger monthly savings with one change.

The best approach is to check both: small spending leaks and larger recurring costs.

How can I save money without feeling deprived?

Cut low-value spending before cutting things you enjoy. Keep a few affordable things that genuinely matter to you, then reduce expenses you barely notice or regret later.

A small fun-money amount can also make saving easier to stick with.

Where should I keep the money I save?

Keep saved money separate from everyday spending if possible. Use a savings account, emergency fund, sinking fund, or separate account for upcoming bills.

The key is to move the money before it gets absorbed into normal spending.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.