When two people earn different amounts, the same bill can feel very different. One partner may be able to cover their share of rent, groceries, and utilities without much stress. The other may pay the same amount and have very little left for savings, debt payments, or personal spending.

That is why some couples use an income-based split. Instead of dividing shared bills equally, each person contributes based on how much they earn.

This can be a helpful middle ground if you want to keep finances fair without combining every account. A good setup should be clear, easy to calculate, and flexible enough to update when income or expenses change.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

What Does It Mean to Split Bills Based on Income?

Splitting bills based on income means each person pays a percentage of shared expenses based on their share of the total household income.

For example, if one partner earns 60% of the combined take-home income and the other earns 40%, they may split shared bills 60/40.

This is also called a proportional split. It is usually used for shared costs like rent, utilities, groceries, household supplies, and other bills both people agree to share.

Personal expenses can still stay separate.

How to Calculate an Income-Based Bill Split

Use monthly take-home pay for the calculation, not gross salary.

Take-home pay usually gives a more realistic number because it shows what each person actually has available after taxes and paycheck deductions.

Here is the formula:

Your income ÷ total household income = your bill percentage

Then apply that percentage to the shared expenses.

For example:

- Partner A takes home $4,500/month

- Partner B takes home $2,500/month

- Total take-home income is $7,000/month

- Shared monthly expenses are $3,200

| Partner | Take-Home Income | Calculation | Bill Percentage | Share of $3,200 |

|---|---|---|---|---|

| Partner A | $4,500 | $4,500 ÷ $7,000 | 64% | $2,048 |

| Partner B | $2,500 | $2,500 ÷ $7,000 | 36% | $1,152 |

The numbers do not have to be perfect down to the cent. Many couples round the split to make it easier, such as 65/35 instead of 64/36.

So in this example, the couple might use a simple 65/35 split:

| Partner | Rounded Split | Share of $3,200 |

|---|---|---|

| Partner A | 65% | $2,080 |

| Partner B | 35% | $1,120 |

That small rounding difference can make the system easier to remember and easier to use every month.

Quorum FCU explains proportional splitting with a clear example, such as one partner making 70% of the income and paying 70% of the expenses. This supports the article well, but again, it is a credit union site.

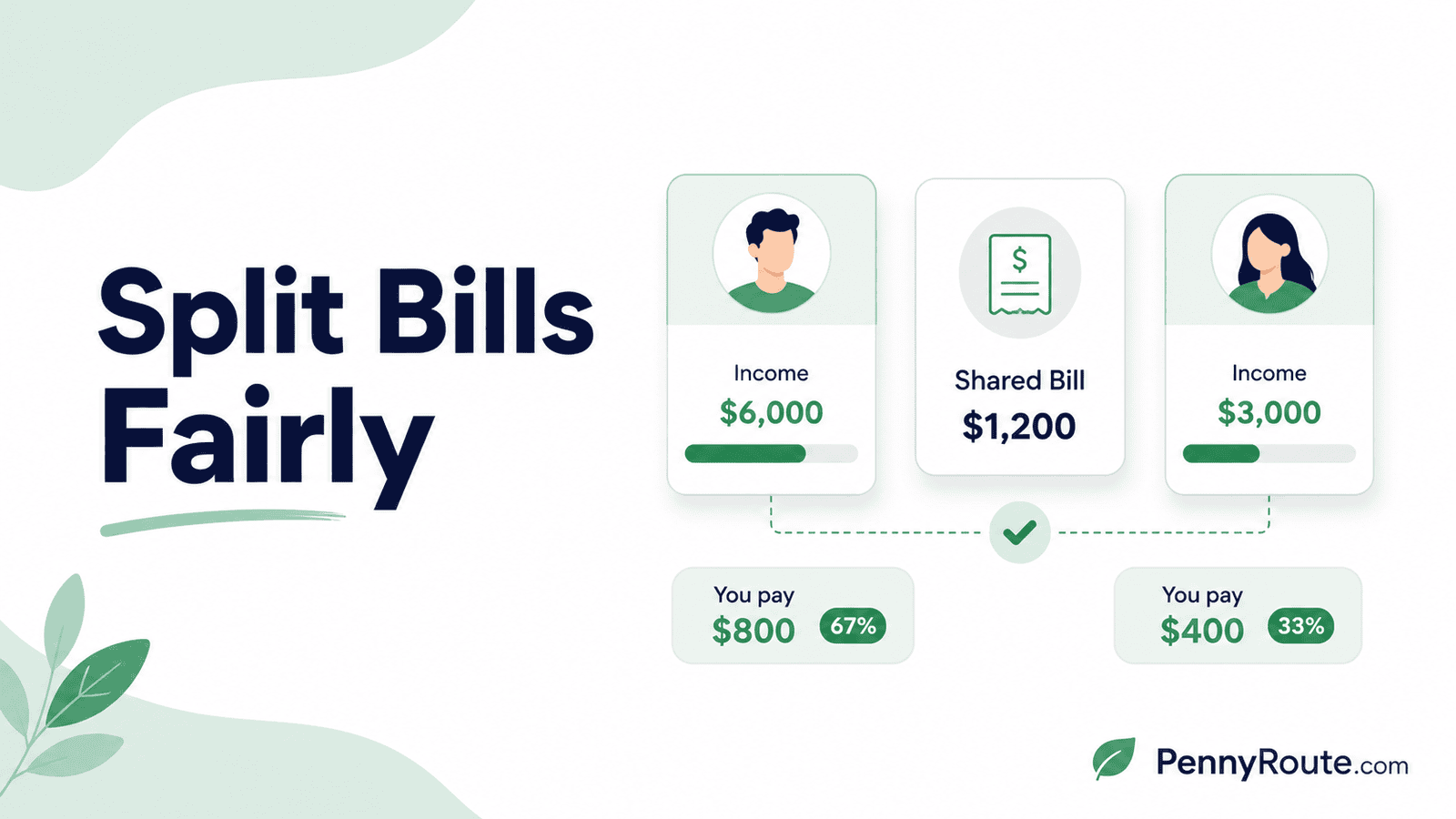

Example: 60/40 Split for Couples

A 60/40 split is one of the easiest income-based splits to understand.

It usually works when one partner earns about 60% of the combined income and the other earns about 40%.

For example:

- Partner A takes home $6,000/month

- Partner B takes home $4,000/month

- Total take-home income is $10,000/month

- Shared monthly expenses are $4,000

Because Partner A earns 60% of the household income, they pay 60% of the shared bills. Partner B pays 40%.

| Partner | Income Share | Share of $4,000 Bills |

|---|---|---|

| Partner A | 60% | $2,400 |

| Partner B | 40% | $1,600 |

This can feel more balanced than each person paying $2,000, especially if the lower earner would have very little left after a 50/50 split.

A 60/40 split is not a rule. It is just one example. If the income gap is larger, the split may look more like 70/30. If the incomes are closer, it may look more like 55/45.

Example: 70/30 Split for a Larger Income Gap

A 70/30 split may make sense when one partner earns much more than the other.

For example:

- Partner A takes home $7,000/month

- Partner B takes home $3,000/month

- Total take-home income is $10,000/month

- Shared monthly expenses are $4,500

Partner A earns 70% of the household income. Partner B earns 30%.

| Partner | Income Share | Share of $4,500 Bills |

|---|---|---|

| Partner A | 70% | $3,150 |

| Partner B | 30% | $1,350 |

If the couple split those same bills 50/50, each person would pay $2,250. That may be manageable for Partner A, but much harder for Partner B.

A 70/30 split can help the lower earner keep more room for savings, debt payments, and personal spending while still contributing to shared expenses.

This is especially useful when the couple’s lifestyle is partly based on the higher earner’s income, such as choosing a more expensive apartment, neighborhood, car, or travel plan.

Should You Use Gross Income or Take-Home Pay?

For most couples, take-home pay is the better number to use.

Gross income is what you earn before taxes, retirement contributions, health insurance, and other paycheck deductions. Take-home pay is what actually reaches your bank account.

Since bills are paid from the money you actually receive, take-home pay usually gives a clearer picture.

For example, two people may both have strong salaries on paper, but one person may have higher tax withholding, insurance costs, retirement contributions, or other deductions. If you use gross income, the split may look fair but feel off in real life.

Use monthly take-home pay when possible. If one person is paid weekly, biweekly, or irregularly, convert it into a monthly estimate so both numbers are easier to compare.

This does not have to be perfect down to the last dollar. The point is to use numbers that reflect what each person can realistically contribute.

Which Expenses Should Be Included?

Use income-based splitting for expenses that are truly shared.

These are usually costs that support both people, the home, or a goal you are working toward together.

Common shared expenses include:

- Rent or mortgage

- Utilities

- Groceries

- Internet

- Household supplies

- Shared subscriptions

- Shared insurance

- Childcare

- Pet costs

- Transportation, if shared

- Shared savings goals

- Planned household purchases

Make one shared expense list before calculating the split. That way, both people know exactly what the percentage applies to.

For example, rent and groceries may be shared. One person’s solo shopping, hobby spending, or personal subscription may stay outside the calculation.

This keeps the income-based split focused on household expenses instead of turning every purchase into a couple decision.

What Should Stay Personal?

An income-based split works best when it is used for shared bills, not every single expense.

Some costs usually make more sense as personal expenses unless both people agree otherwise.

Personal expenses may include:

- Hobbies

- Clothes

- Solo meals or coffee

- Individual subscriptions

- Personal gifts

- Personal debt payments

- Personal savings goals

- Family support obligations

- Beauty, grooming, or wellness costs

- Fun money for each person

For example, if one partner has a streaming service only they use, that may stay personal. If both people use it regularly, it can go on the shared expense list.

The same idea applies to debt. A personal loan, old credit card balance, or student loan does not automatically become a shared bill just because you are splitting household expenses by income.

You can still decide to help each other, especially in a serious relationship or marriage. But that should be a clear agreement, not an assumption.

What If One Person Has Irregular Income?

Income-based splitting is easiest when both people earn a steady paycheck. But many couples do not have that.

One person may freelance, work hourly, earn commission, drive for gig apps, run a small business, or have seasonal income. In that case, using the same income number every month may not work.

Here are a few ways to handle it:

- Use an average income: Look at the last 3 to 6 months and use the average monthly take-home pay.

- Use last month’s income: Recalculate the split each month based on what actually came in.

- Set a minimum contribution: The irregular earner pays a realistic base amount, then adds more in higher-income months.

- Build a shared buffer: Keep a small cushion in the shared bill account for slower months.

- Review more often: A monthly check-in may work better than reviewing every few months.

For example, if one partner’s income changes often, the couple might use a 3-month average for rent and utilities, then adjust flexible categories like groceries or savings goals month by month.

The aim is to keep shared bills paid without pretending irregular income is the same as a fixed salary.

What If the Lower Earner Still Feels Stretched?

An income-based split can make bills feel more balanced, but it cannot fix expenses that are simply too high.

If the lower earner still has very little left after paying their share, look at the shared costs together. The issue may not be the percentage. It may be the rent, lifestyle, savings target, or regular expenses the couple is trying to maintain.

This can happen when shared choices are based mostly on the higher earner’s budget.

For example, a higher-income partner may feel comfortable with a more expensive apartment, frequent dining out, or a larger travel budget. But if the lower earner is still struggling after the split, those choices may need to be adjusted.

A few options can help:

- Lower the shared expense budget

- Choose rent or housing costs both people can afford

- Reduce aggressive savings goals for a while

- Keep personal spending separate and realistic

- Review debt payments or other obligations

- Build a small buffer into the shared bill account

A proportional split helps, but both people still need room to breathe after shared bills are paid.

Is Splitting Bills Based on Income Always Fair?

Splitting bills based on income can be fair, but it is not automatically perfect.

It works best when both people are honest about income, agree on which expenses are shared, and feel comfortable with the percentage split.

It may not feel fair if:

- One person is not open about their income

- One partner keeps increasing shared expenses

- The higher earner pays more but feels they get no say in the budget

- The lower earner pays less but avoids contributing where they reasonably can

- One person uses money as control

- The setup creates resentment instead of clarity

The higher earner paying more should not mean they control every decision. The lower earner paying less should not mean their contribution matters less.

A healthy income-based split still needs respect on both sides. The numbers can help, but the agreement only works if both people feel heard.

How to Set Up an Income-Based Split in Real Life

Once you know the percentages, decide how you will actually pay the bills each month.

The simplest setup is to keep shared expenses in one place.

Here is one way to do it:

- List your shared monthly expenses.

- Calculate each person’s income percentage.

- Decide how much each person will contribute.

- Transfer those amounts into a shared account or tracking system.

- Pay shared bills from that account or mark them as paid in your tracker.

This works best when it fits into your larger plan for budgeting as a couple, including shared bills, personal spending, savings goals, and regular check-ins.

For example, if the split is 65/35 and shared bills are $3,200, Partner A may transfer $2,080 and Partner B may transfer $1,120 into a shared bill account each month.

If you do not want a joint account, you can use a spreadsheet or bill-splitting app instead. One person may pay the bill, then the tracker shows how much the other person owes.

The setup does not need to be fancy. It just needs to show what is due, who is paying, and whether the split still matches your current income.

How Often Should You Recalculate the Split?

An income-based split should not stay frozen forever.

Incomes change. Rent changes. Bills change. Sometimes one person gets a raise, loses hours, starts a new job, takes parental leave, or picks up extra debt payments.

You do not need to recalculate every week. For most couples, reviewing the split every 3 to 6 months is enough.

You may want to review it sooner if:

- One person gets a raise or pay cut

- One person loses a job or starts a new one

- Rent, mortgage, or utilities change

- One partner’s debt payments change

- You move in together, get married, or have a child

- Shared savings goals become too aggressive

- One person feels stretched after bills

A regular review keeps the split fair without turning every small income change into a new budget meeting.

How to Talk About Splitting Bills Based on Income

Talking about money can feel awkward, especially if you are asking to change how bills are currently split.

Try to keep the conversation focused on the numbers and the shared setup, not blame.

You could say:

“Can we look at how we split shared bills? Since our incomes are different, I’m feeling stretched with the current setup. I’d like us to see whether an income-based split would work better.”

Or:

“I want us to have a system that feels fair for both of us. Can we look at our take-home income, shared bills, and what each person has left after expenses?”

A few tips can help:

- Choose a calm time, not right after a money disagreement.

- Use take-home income instead of guessing.

- Talk about shared bills first, not every personal purchase.

- Suggest testing the split for one or two months.

- Agree on when you will review it again.

The conversation does not need to solve everything at once. Start with the shared bills, make the first version clear, and adjust from there.

Choose a Split That Leaves Both People Room to Breathe

plitting bills based on income can be helpful when one person earns more, but the setup should still feel clear and respectful for both partners.

The higher earner should not feel responsible for everything, and the lower earner should not feel like their contribution matters less.

Start with take-home income, list only the expenses you both agree are shared, and choose a percentage that is easy to use each month.

Then review the setup when income, bills, or life changes. A fair split is not just about the math. It is about building a system both people can understand, afford, and keep using.

FAQs About Splitting Bills Based on Income

How do you split bills based on income?

Add both partners’ monthly take-home income, then calculate each person’s percentage of the total. Use those percentages to divide shared expenses. For example, if one partner earns 60% of the household income, they may pay 60% of shared bills.

Is splitting bills based on income fair?

Splitting bills based on income can be fair when one partner earns more and a 50/50 split would leave the lower earner stretched. It works best when both people agree on the shared expenses, use clear numbers, and review the setup when income or bills change.

Should rent be split based on income?

Rent can be split based on income if one partner earns more or if the rent amount was chosen around the higher earner’s budget. This can help prevent the lower earner from spending too much of their income on housing.

What is a 60/40 split in a relationship?

A 60/40 split means one person pays 60% of shared expenses and the other pays 40%. This usually fits when one partner earns about 60% of the combined household income and the other earns about 40%.

Should personal expenses be split based on income?

Usually, no. Income-based splitting works best for shared expenses like rent, utilities, groceries, and household bills. Personal spending, individual subscriptions, personal debt, and hobbies usually stay separate unless both people agree otherwise.

What if my partner does not want to split bills based on income?

Start with a calm conversation using real numbers. Show both take-home incomes, shared bills, and what each person has left after expenses. You can suggest testing an income-based split for one or two months instead of making a permanent change right away.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.