Bad spending habits are not always obvious. Sometimes, it is not one huge purchase that throws your budget off track. It is the small choices that keep repeating.

The sale item you did not plan to buy. The quick online order. The “it’s only $10” purchase. The payday treat that quietly turns into a full shopping cart.

That does not mean you are bad with money. It usually means your spending has a few patterns that need more attention.

Once you notice which habits are making you overspend, you can start fixing them one at a time. Small changes are easier to keep, and they can make your budget much less stressful.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

What Are Bad Spending Habits?

Bad spending habits are repeated money choices that can make it harder to stay within your budget, save money, or avoid debt.

They are not always huge mistakes. Many poor spending habits look normal in the moment, especially when the purchase is small or convenient.

For example, spending $8 here and $12 there may not seem like much. But when those choices repeat several times a week, they can quietly take money away from bills, savings, debt payments, or other goals.

The goal is not to stop spending completely. It is to notice which habits are causing problems, so you can make better choices before your money disappears.

Why Bad Spending Habits Are Hard to Notice

Bad spending habits can be hard to spot because they often look normal while they are happening.

You may not notice one small purchase. You may not worry about one takeout meal, one sale item, or one quick app order. The problem usually starts when those choices become automatic.

Many spending habits are also tied to triggers, such as:

- boredom

- stress

- payday excitement

- social pressure

- convenience

- online shopping apps

- saved payment details

Spending triggers can be emotional or situational. MoneyHelper explains that stress, boredom, sales, ads, and social media can all influence how people spend. That is why simply saying “I need to spend less” does not always work.

A better first step is to ask, “What usually makes me spend when I did not plan to?”

Once you know the trigger, the habit becomes easier to change.

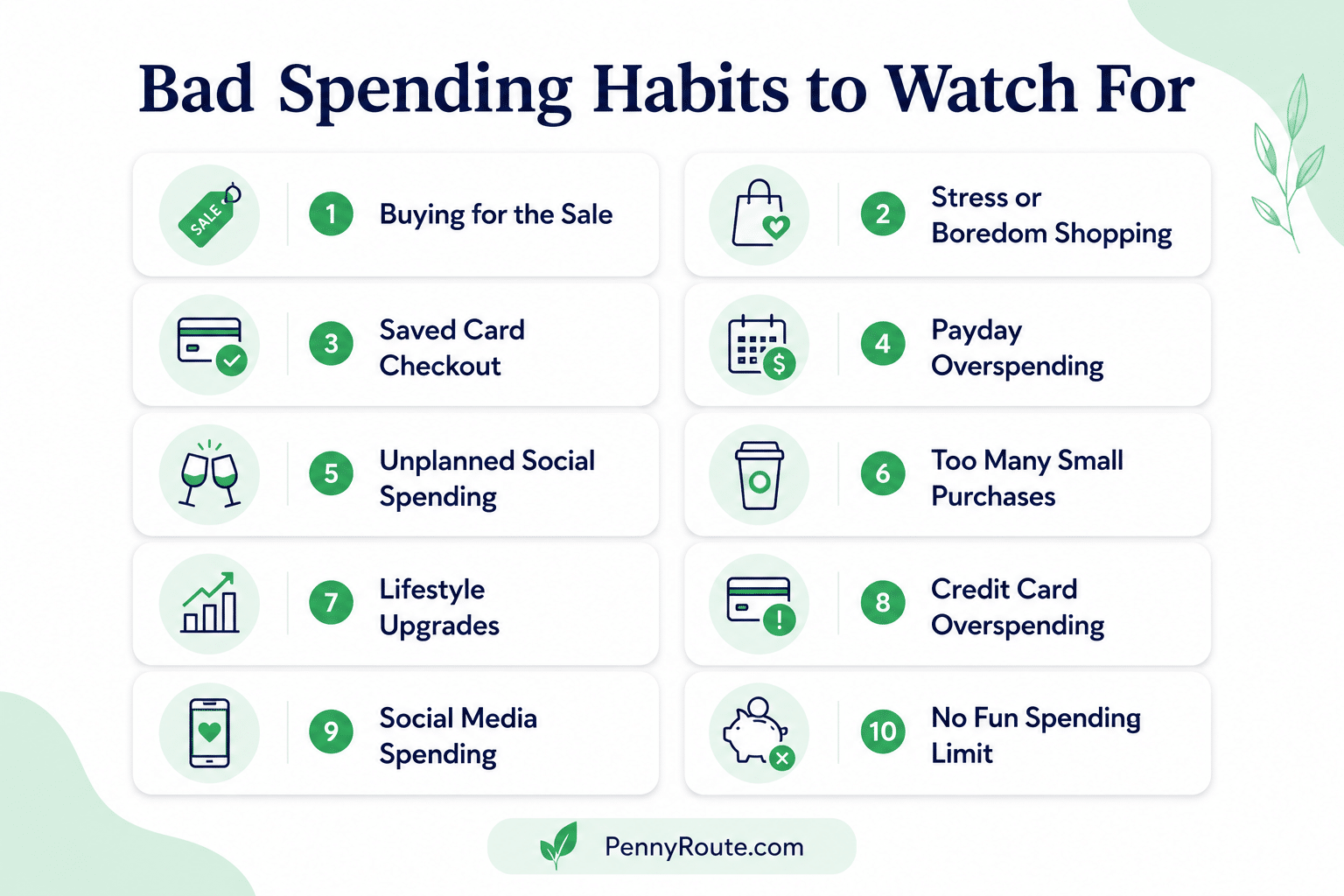

10 Bad Spending Habits That Make You Overspend

Bad spending habits are easier to fix when you can clearly see what they look like in real life.

Here are common spending patterns that can quietly pull money away from your budget.

1. Buying Something Mainly Because It Is on Sale

A discount can make a purchase feel smart, even when you did not need the item in the first place.

This habit is tricky because it sounds responsible. You may think, “I saved 40%,” but if the item was not planned, you still spent money you could have kept.

For example, buying a $60 jacket for $35 only saves money if you already needed a jacket and had room for it in your budget. If not, it is still $35 gone.

Small fix: Before buying a sale item, ask yourself, “Would I still want this if it were full price?” If the answer is no, the discount may be the reason you want it. That quick pause can help you spot impulse buys before they happen, which is one simple way to stop overspending.

2. Shopping When You Are Bored, Stressed, or Tired

Shopping can become an easy distraction when your mood is low or your brain is worn out.

You may open a shopping app “just to look,” then end up buying something because it gives you a quick lift. The problem is that the purchase does not usually fix the real issue. It only adds another charge to your budget.

This is one of the most common bad spending habits because it often happens without much planning. You are not always shopping because you need something. Sometimes, you are shopping because you need a break.

Small fix: Create a short “before I buy” pause. Drink water, take a quick walk, message a friend, or wait 24 hours before checking out. If you still want the item later and it fits your budget, you can decide with a clearer mind.

3. Keeping Saved Payment Details on Shopping Apps

Saved payment details make online shopping almost too easy.

When your card is already saved, you do not have to pause, get your wallet, type in the details, or think twice. A purchase can happen in a few taps, especially when an app already has your address, card, and delivery options ready.

That convenience can turn into overspending when you buy things before your budget has a chance to say, “Excuse me?”

Small fix: Remove saved cards from shopping apps you use too often. Adding a little friction can give you enough time to ask, “Do I actually need this right now?”

4. Treating Payday Like Permission to Spend

Payday can make your account balance look better than it really is.

When money lands in your account, it is easy to think you have more room to spend. But some of that money may already belong to rent, bills, groceries, debt payments, savings, or other upcoming expenses.

This habit can lead to overspending early in the pay cycle. Then, by the end of the week or month, money starts feeling tight again.

Small fix: Before spending on payday, subtract your bills, savings, and basic expenses first. What is left is your real spending room, not the full paycheck amount.

5. Saying Yes to Every Plan Without Checking Your Budget

Social plans can quietly become one of the easiest ways to overspend.

A dinner here, a birthday gift there, a weekend plan, a quick coffee, or a last-minute event may not seem like a big deal on its own. But when you say yes automatically, your budget may end up paying for plans you never really checked.

This does not mean you need to say no to everything. It just means your money needs a quick vote before your calendar fills up.

Small fix: Before saying yes, check two things: the real cost and your spending room. If it does not fit, suggest something cheaper, like coffee instead of dinner, a walk instead of shopping, or hosting at home instead of going out.

6. Buying Cheap Items Too Often

Cheap purchases can be sneaky because each one feels harmless.

A $5 item here, a $7 add-on there, or a “tiny treat” at checkout may not seem worth worrying about. The problem starts when small purchases happen so often that they become a regular part of your spending.

This habit can also make it harder to notice where your money went. You may look back and think, “I did not buy anything big,” but your account balance tells a different story.

Small fix: Set a weekly limit for small unplanned purchases. You do not have to cut them out completely. Just give them a clear boundary so they do not quietly take over your budget.

7. Upgrading Small Lifestyle Choices Without Noticing

Lifestyle upgrades are not always big or dramatic.

Sometimes, they show up as slightly nicer versions of things you already buy. A more expensive coffee order. A higher phone plan. Premium versions of apps. Brand-name groceries when store brands would work. A more expensive gym, subscription, or delivery option.

One upgrade may not hurt your budget. But when several small upgrades become your new normal, your monthly spending can rise without you noticing.

This is one reason bad spending habits can be hard to catch. You may not feel like you are overspending because each choice seems reasonable on its own.

Small fix: Pick one category and compare what you spend now with what you used to spend. If the increase is not adding real value to your life, consider switching back or choosing a lower-cost option.

8. Using Credit Cards Like Extra Money

A credit card can be useful, but it can also make overspending easier if you treat it like extra income.

This habit usually starts with small choices. You charge a few things now and tell yourself you will deal with them later. But when the bill arrives, those “later” purchases still need to be paid for.

The issue is not the card itself. The issue is spending without a clear payoff plan.

Small fix: Before using a credit card, ask, “Can I pay this off when the bill comes?” If the answer is no, it may be better to pause the purchase unless it is a true emergency.

9. Copying Spending Habits From Friends or Social Media

It is easy to spend more when everyone around you seems to be doing the same.

Maybe your friends eat out often, take weekend trips, buy new outfits, or upgrade their phones. Maybe social media keeps showing you “must-have” products, room makeovers, budget planners, kitchen gadgets, or routines that look affordable until you start adding them to your cart.

The problem is that you usually see the spending, not the full financial picture behind it. Someone else’s normal may not fit your income, bills, savings goals, or current budget.

Small fix: Before copying a purchase or plan, ask, “Would I still want this if no one else saw it?” If the answer is no, it may be more about pressure than real value.

10. Not Setting a Limit for Fun Spending

Fun spending is not bad. A budget that leaves no room for small treats, hobbies, or social plans can be hard to stick with.

The problem starts when fun spending has no limit. A coffee, movie, dinner, app purchase, game, book, or weekend plan may be perfectly fine. But without a clear amount, it is easy to keep saying yes until your budget is stretched.

This habit can also lead to guilt, which is not helpful. You spend, feel bad, promise to stop completely, then repeat the same pattern later.

Small fix: Give yourself a set amount for fun spending each week or month. Once that money is used, pause extra non-essential spending until the next reset. This keeps fun in your budget without letting it take over.

How to Break One Bad Spending Habit at a Time

Trying to fix every spending habit at once can backfire.

It sounds productive, but it can make your budget feel too strict too quickly. Then the plan becomes harder to follow.

A better approach is to choose one habit and work on that first.

Start with the habit that causes the most stress or the one that happens most often. For example, if online shopping is your biggest issue, you might remove saved payment details from shopping apps. If social plans keep breaking your budget, you might set a weekly going-out limit.

Use this simple process:

- Pick one habit. Do not try to fix all ten at the same time.

- Find the trigger. Ask what usually happens right before you spend.

- Add one small barrier. Use a waiting rule, remove an app, set a limit, or check your budget first.

- Review after one week. See what worked, what felt difficult, and what needs adjusting.

The goal is not to become perfect with money overnight. The goal is to make spending decisions a little less automatic.

Once you fix one spending trigger, you can build simple daily money habits that help you stay more aware of where your money goes.

When Bad Spending Habits Are Not the Whole Problem

Sometimes, spending habits are only part of the picture.

If rent, groceries, debt payments, childcare, transportation, or other basic costs take up most of your income, cutting small purchases may not fix everything. You may already be trying hard, and still have very little room left in your budget.

That does not mean habit changes are pointless. It just means they work best when you also look at the bigger numbers.

You may need to review your main bills, adjust your budget categories, look for lower-cost options, or make a plan for debt payments if they are taking up too much of your income.

Start with the spending habits you can control, but do not blame yourself if the bigger issue is that your budget needs more breathing room.

Small Spending Changes Are Easier When You Know the Trigger

Bad spending habits are easier to change when you stop looking at them as personal failures.

Most overspending has a pattern behind it. Maybe you spend more when you are tired, bored, excited after payday, scrolling social media, or trying to keep up with plans that do not fit your budget.

Once you know the trigger, you can make a small change before the spending happens.

You do not need to fix every habit today. Pick one habit from this list, add one simple boundary, and review how it goes after a week.

Small changes may not look impressive at first, but they can help you feel more in control of your money one decision at a time.

FAQs About Bad Spending Habits

What are examples of bad spending habits?

Examples of bad spending habits include buying things just because they are on sale, shopping when you are bored or stressed, using credit cards without a payoff plan, saying yes to plans without checking your budget, and making too many small unplanned purchases.

How do I stop bad spending habits?

Start by choosing one habit to fix first. Then look for the trigger behind it. For example, if you shop online when you are bored, remove saved payment details from shopping apps or use a 24-hour waiting rule before buying. Small barriers can help you pause before spending.

What causes poor spending habits?

Poor spending habits are often caused by convenience, stress, boredom, social pressure, payday excitement, or easy access to online shopping.

They are not always about being careless with money. Many spending habits become automatic because they are tied to emotions, routines, or situations that happen often.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.