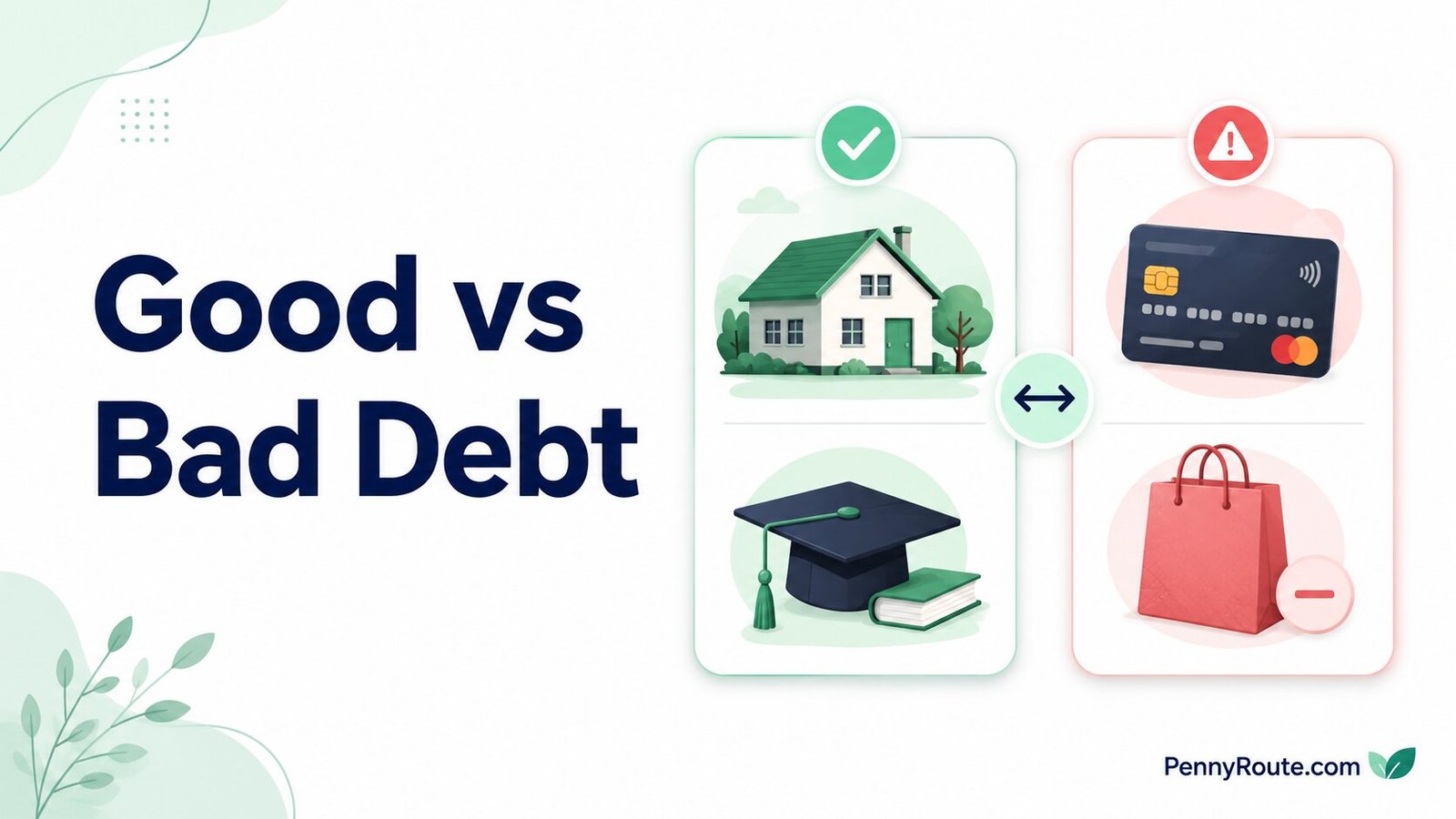

Debt can feel confusing because people talk about it in two very different ways. Some say all debt is bad and should be avoided. Others say certain types of debt can help you build a better future. The truth is usually somewhere in the middle.

Debt is not automatically good or bad just because of its name. A student loan, mortgage, car loan, or credit card balance can help or hurt depending on the cost, the payment, the purpose, and your plan to pay it back.

That is why it helps to understand the difference between good debt and bad debt before borrowing money or deciding which debt to pay off first. The right question is not only “What kind of debt is this?” It is also “Can I afford it, and does it move me forward?”

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

What Is Good Debt?

Good debt is debt that may help you build value, increase income, or support a long-term goal.

That does not mean the debt is risk-free. It still needs to be affordable, and it still needs a clear payoff plan.

Common examples of good debt may include:

- a reasonable mortgage on a home you can afford

- student loans for education that improves your earning potential

- a business loan with a clear plan and realistic numbers

- a loan for training or certification that can help your career

- a necessary car loan if it helps you get to work and fits your budget

The word “good” can be misleading. Good debt is not good because it feels normal or because many people use it. It is only useful when the cost makes sense and the debt helps your future more than it hurts your current budget.

What Is Bad Debt?

Bad debt is debt that is expensive, hard to repay, or used for things that do not add lasting value.

This often includes debt with high interest rates, unclear payoff plans, or payments that make your monthly budget harder to manage.

Common examples of bad debt may include:

- high-interest credit card balances

- payday loans

- high-interest personal loans for wants

- buy now, pay later purchases that stack up

- loans used mainly for lifestyle spending

- unaffordable car loans or long loan terms

Bad debt is not about judging what you bought. It is about the cost of carrying that debt and whether it helps or hurts your financial stability.

A purchase may feel small at first, but if the debt grows through interest, late fees, or repeated borrowing, it can become much harder to deal with later.

Good Debt vs Bad Debt: Key Differences

The easiest way to compare good debt and bad debt is to look beyond the label.

A debt may sound “good” because it is tied to education, a home, or a business. But if the payment is too high or the interest rate is painful, it can still create problems.

A debt may sound “bad” because it involves a credit card or personal loan. But if it was used for a true need and you have a realistic payoff plan, the situation may be fixable.

Here is a simple way to compare them:

| Question to Ask | Good Debt Usually | Bad Debt Usually |

|---|---|---|

| Does it help your future? | Supports income, stability, or long-term value | Pays for things that lose value quickly |

| Is the interest rate manageable? | Has a lower or reasonable rate | Has a high rate or costly fees |

| Is there a payoff plan? | Has a clear repayment timeline | Gets carried month to month without a plan |

| Does the payment fit your budget? | Leaves room for bills, savings, and essentials | Makes the rest of your budget feel tight |

| Is the debt tied to a need or goal? | Helps with housing, education, work, or business | Often funds non-essential spending |

| What happens if income drops? | Still has some room in the budget | Quickly becomes hard to manage |

Experian also notes that the difference between good debt and bad debt often depends on whether the debt supports financial growth or becomes difficult to repay.

The main difference is not just what you borrowed for. It is whether the debt helps you move forward without putting too much pressure on your monthly budget.

Examples of Good Debt and Bad Debt

Some debts are easy to label, but many fall into a gray area.

A mortgage, student loan, car loan, or credit card balance can be helpful or harmful depending on the amount, interest rate, repayment plan, and how it fits your budget.

Mortgage Debt

Mortgage debt is often considered good debt because a home may build value over time.

But that does not mean every mortgage is a good idea. A home can also come with property taxes, insurance, repairs, maintenance, utilities, and moving costs.

- Good debt example:

A mortgage payment that fits your budget and still leaves room for savings, bills, and normal life. - Bad debt example:

A mortgage that takes up so much income that every repair, tax increase, or surprise bill creates stress.

Student Loan Debt

Student loans can be good debt when they help you increase your earning potential.

But they can become difficult if the amount borrowed is much higher than the income you can realistically expect after school.

- Good debt example:

A reasonable student loan for a degree, training, or certification that supports a clear career path. - Bad debt example:

Borrowing heavily without understanding the monthly payment, interest, job prospects, or repayment options.

Credit Card Debt

Credit cards are not automatically bad.

They can be useful if you pay the balance in full and use them carefully. The problem starts when balances roll over month to month with high interest.

- Good use example:

Using a credit card for planned expenses and paying it off when the bill comes. - Bad debt example:

Carrying a growing balance while still adding new purchases to the card.

Car Loan Debt

A car loan can be necessary if reliable transportation helps you get to work, school, or important appointments.

But a car loan can become bad debt if the payment is too high, the loan term is too long, or the total cost stretches your budget.

- Good debt example:

A practical car loan with a payment you can afford, for a vehicle that meets your needs. - Bad debt example:

Buying more car than your budget can handle because the monthly payment looks manageable at first.

If a car loan would stretch your budget, it may be worth making a plan to save up for a car first.

Buy Now, Pay Later Debt

Buy now, pay later can make a purchase feel smaller because the cost is split into payments.

That can be risky when several payment plans overlap at the same time.

- Good use example:

Using it rarely for a planned purchase you can already afford. - Bad debt example:

Using multiple payment plans for wants, then losing track of what is due and when.

When Good Debt Can Turn Bad

Good debt can turn bad when the cost, payment, or risk becomes too much for your budget.

This can happen even when the reason for borrowing seems reasonable. A student loan, mortgage, business loan, or car loan may support a useful goal, but the debt still needs to fit your real life.

Good debt can become a problem when:

- you borrow more than you need

- the interest rate is higher than expected

- the monthly payment leaves no room for savings

- there is no clear payoff plan

- your income drops after borrowing

- the debt depends on everything going perfectly

- you keep adding new debt before paying down the old balance

For example, a car loan may help you get to work. But if the payment, insurance, fuel, and repairs take up too much of your income, the loan can still create pressure.

Taking on debt without checking the full cost can become one of those bad financial decisions that affect your budget for years.

A debt may start with a good purpose, but it still needs a realistic plan. If the payment makes the rest of your budget feel tight every month, it may not be as “good” as it looked at first.

How to Decide If a Debt Is Worth Taking On

Before taking on debt, slow down and look at the full cost.

A payment can look affordable by itself, but debt affects more than one line in your budget. It can change how much room you have for bills, savings, emergencies, and normal spending.

A simple budget can help you see whether a new payment fits with your bills, savings, and other priorities.

Ask these questions first:

- What is the total cost?

Look beyond the purchase price. Include interest, fees, insurance, maintenance, and any extra costs that come with the debt. - What is the interest rate?

A lower payment may still cost more if the loan term is long or the interest rate is high. - Can the monthly payment fit with your real budget?

The payment should fit after your essentials are covered. - What happens if your income drops?

If one smaller paycheck would make the payment hard to manage, the debt may be risky. - Does this debt help your future?

Ask whether it supports income, stability, education, housing, transportation, or another real goal. - What is the payoff plan?

Know when the debt should be paid off and how you will make the payments. - What are you giving up to afford it?

Every payment takes money from somewhere else. Make sure the trade-off is worth it.

If the debt helps your future, fits your budget, and has a clear payoff plan, it may be manageable. If it only adds pressure or depends on everything going perfectly, it may be better to pause.

How Good Debt and Bad Debt Affect Your Payoff Plan

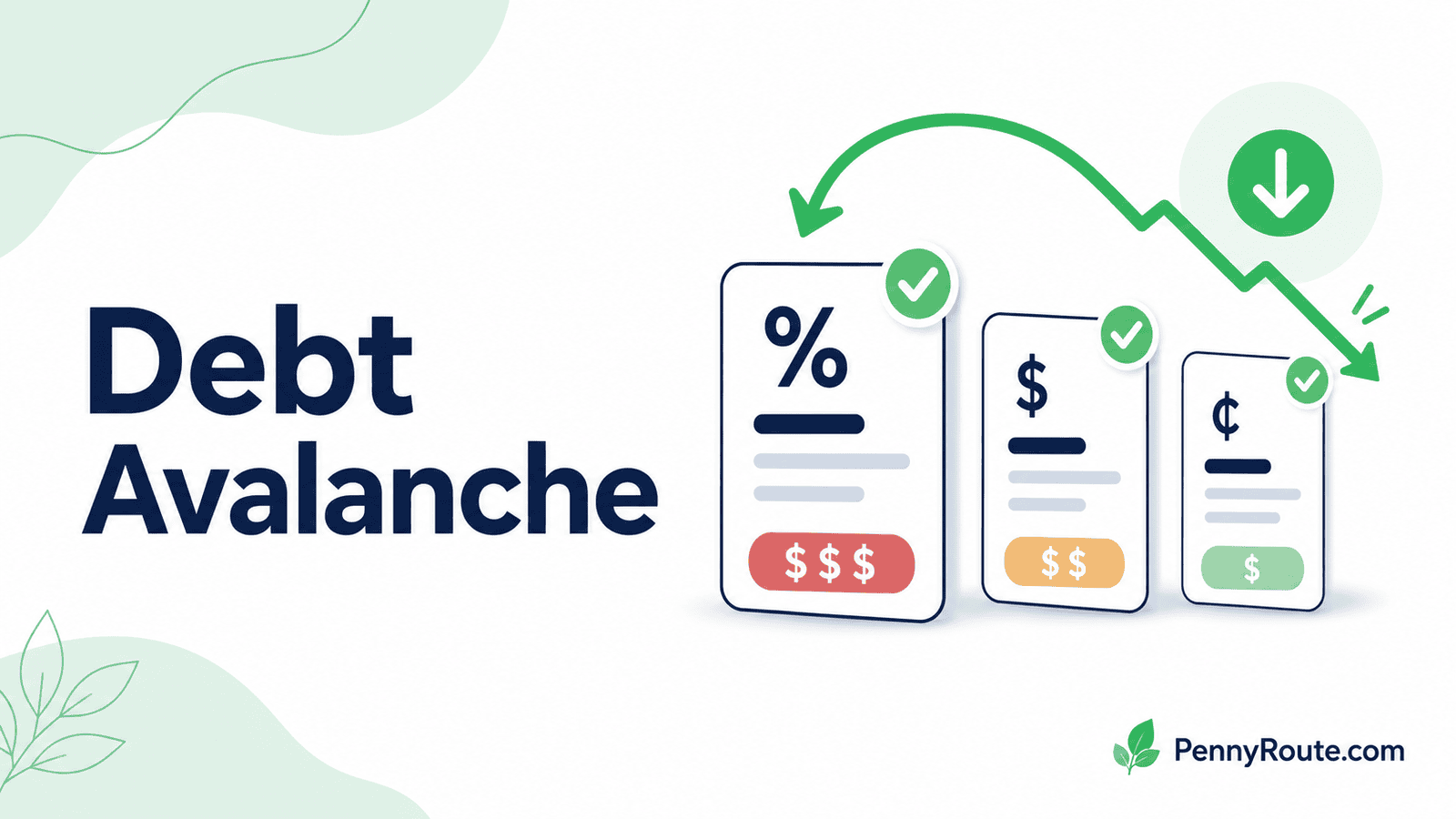

Knowing the difference between good debt and bad debt can help you decide where extra payments may make the biggest impact.

High-interest debt usually deserves attention because it can cost more the longer it sits. This often includes credit card balances, payday loans, high-interest personal loans, or buy now, pay later payments that are starting to stack up.

Lower-interest debt, such as a manageable mortgage or student loan, may not always need to be your first extra-payment target. You still need to make required payments, but extra money may go further when it is focused on expensive debt first.

If you are deciding which debt to pay off first, start with essentials and minimum payments. Then look at urgency, interest rates, balances, and consequences before choosing where extra money should go.

Debt Works Best When It Has a Purpose and a Plan

Debt is not always simple enough to label as good or bad.

A mortgage, student loan, car loan, or business loan can help if it supports a real goal and fits your budget. But even debt with a good purpose can become stressful if the payment is too high, the interest rate is expensive, or there is no clear payoff plan.

The same is true in reverse. A debt that started as a mistake can still be improved when you stop adding to it and start paying it down.

Before borrowing, look at the full cost, the monthly payment, and what the debt will help you do. If it moves you forward without putting too much pressure on your budget, it may be manageable.

Debt works best when it has a purpose, a plan, and a payment you can actually afford.

FAQs About Good Debt vs Bad Debt

Is a credit card good debt or bad debt?

A credit card is not automatically bad debt. If you use it for planned purchases and pay the balance in full each month, it can be a normal payment tool.

Credit card debt usually becomes bad debt when you carry a balance month to month with high interest, keep adding new purchases, or only make minimum payments without a payoff plan.

Is a car loan good debt or bad debt?

A car loan can be useful if reliable transportation helps you get to work, school, appointments, or other important places, and the payment fits your budget.

It can become bad debt if the monthly payment is too high, the loan term is too long, or the full cost of the car leaves little room for bills, savings, insurance, fuel, and repairs.

Should I pay off good debt or bad debt first?

In many cases, it makes sense to focus extra payments on high-interest debt first because it costs more over time.

Still, you should keep making minimum payments on every debt. The best payoff order depends on your interest rates, balances, budget, and which method helps you stay consistent.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.