A budget with too many categories can get old fast. Rent, groceries, gas, subscriptions, savings, debt, fun money, gifts, car repairs, random “how did I spend that much?” purchases — it can start to feel like your money needs its own filing cabinet.

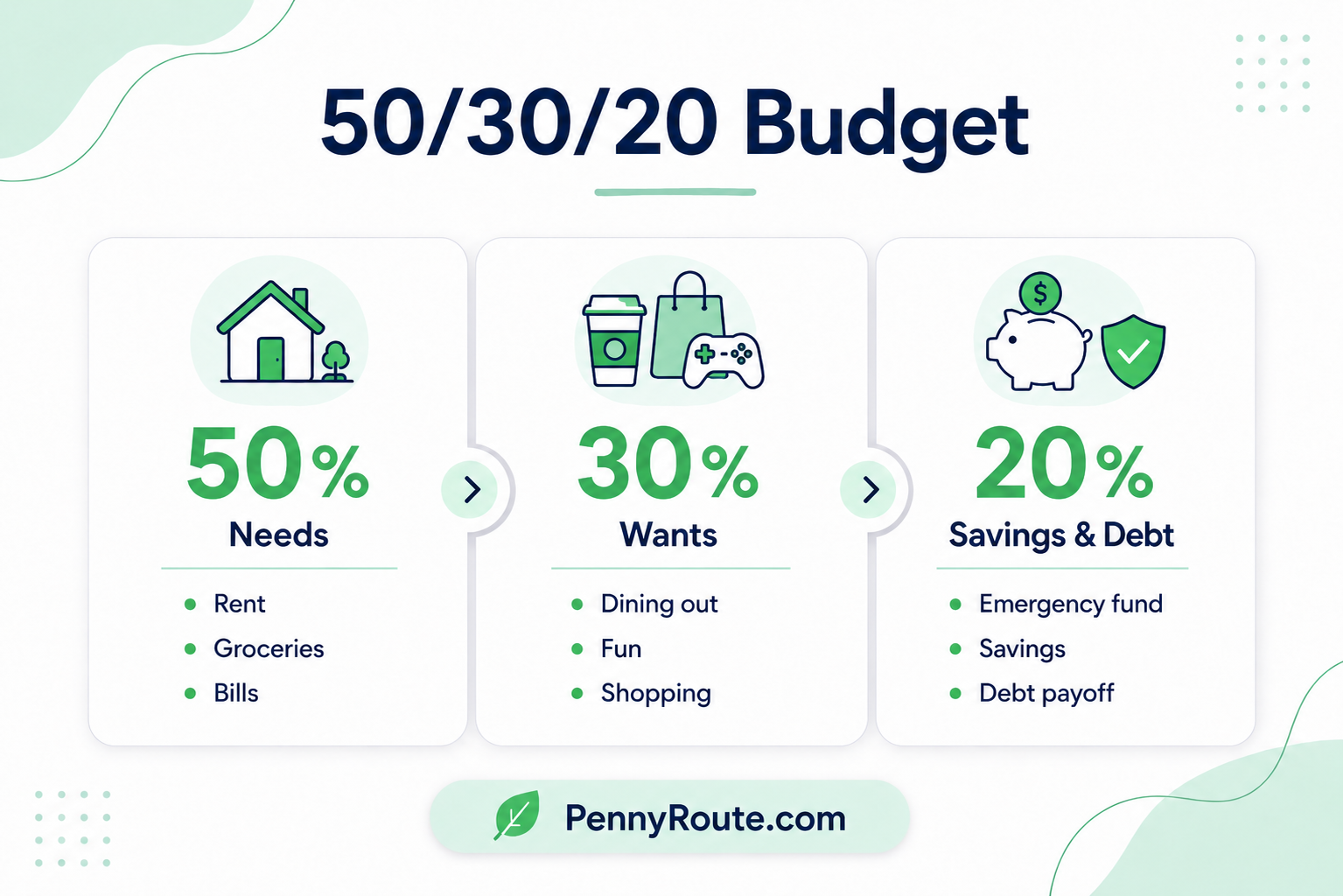

The 50/30/20 budget method keeps things simpler. Instead of tracking every small category from the start, it divides your take-home pay into three main groups: 50% for needs, 30% for wants, and 20% for savings or extra debt payments.

It is not a perfect rule for every income or every city. Rent may be high, groceries may take up more than expected, and debt payments may need extra attention. But as a starting point, the 50/30/20 rule can help you see whether your money is balanced or stretched too thin.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

What Is the 50/30/20 Budget Method?

The 50/30/20 budget method is a simple way to divide your take-home pay into three broad groups:

- 50% for needs

- 30% for wants

- 20% for savings and extra debt payments

The important phrase here is take-home pay. This method usually works best when you use the money that actually reaches your bank account after taxes and payroll deductions, not your full salary before deductions.

So if your paycheck after taxes is $3,000 per month, the basic split would look like this:

| Category | Monthly Amount |

|---|---|

| Needs | $1,500 |

| Wants | $900 |

| Savings and extra debt payments | $600 |

This does not mean every household will fit the percentages perfectly. The real value of the 50/30/20 rule is that it gives you a quick way to check your balance.

If your needs are taking 70% of your income, you can see why saving feels hard. If your wants are quietly taking over, the numbers will show that too.

That makes this budgeting method useful even if you need to adjust the percentages. It gives you a starting point, not a money rulebook with a tiny judge’s wig.

How the 50/30/20 Rule Works

The 50/30/20 rule works by giving your take-home pay three main jobs: essentials, lifestyle spending, and future goals.

Here’s the basic split:

| Category | Percentage | Simple Meaning |

|---|---|---|

| Needs | 50% | Things you must pay for |

| Wants | 30% | Things you enjoy but could reduce |

| Savings and extra debt payments | 20% | Money for future goals and faster debt payoff |

The method is simple, but the categories can get a little blurry.

Groceries are usually a need. Restaurant meals are usually a want. A basic phone plan may be a need, while the most expensive plan with every upgrade may be more of a want.

That is why the 50/30/20 budget works best when you are honest about what each expense is doing in your life. Not in a harsh way. Just in a “let’s not call three streaming services a utility bill” kind of way.

The goal is not to make your spending perfect. The goal is to see whether your money is mostly going where you want it to go.

Calculate Your Take-Home Pay First

Before you use the 50/30/20 budget, start with your take-home pay.

Take-home pay is the money you actually receive after taxes and payroll deductions. It is not your full salary before deductions.

For example, if your salary is $4,000 per month before taxes, but $3,200 reaches your bank account, use $3,200 for your 50/30/20 budget.

Here’s how that would break down:

| Category | Percentage | Monthly Amount |

|---|---|---|

| Needs | 50% | $1,600 |

| Wants | 30% | $960 |

| Savings and extra debt payments | 20% | $640 |

If you are paid every two weeks, you can still use the method. Add up your expected take-home pay for the month, then apply the percentages to that amount.

If your income changes from month to month, use a lower average or your lowest typical monthly income as your starting point. That gives your budget more breathing room and keeps you from building your plan around a unusually good month.

Put 50% Toward Needs

The first part of the 50/30/20 budget is for needs.

Needs are the expenses you must pay to live, work, and keep your basic financial life stable. These are usually the bills and essentials that cannot be skipped without causing bigger problems.

Common needs include:

| Need | Examples |

|---|---|

| Housing | Rent or mortgage |

| Food | Basic groceries |

| Utilities | Electricity, water, gas, trash |

| Transportation | Gas, public transport, basic car costs |

| Insurance | Health, car, renters, or home insurance |

| Debt minimums | Minimum credit card, loan, or student loan payments |

| Childcare | Essential childcare costs |

| Basic communication | Phone or internet needed for work, school, or daily life |

For example, if your monthly take-home pay is $3,200, the 50/30/20 method gives you $1,600 for needs.

This does not mean your needs will always fit perfectly into 50%. Housing, groceries, insurance, and transport can take up more than expected, especially in high-cost areas.

If your needs are over 50%, do not treat that as failure. Treat it as information. It may mean you need to adjust the percentages, reduce a few flexible costs, or focus on increasing income over time.

Also, be careful with “needs” that have upgraded versions. Groceries are a need. Frequent premium grocery deliveries may be partly a want. A phone plan may be a need. The most expensive plan with extras you barely use may not be.

The goal is not to judge every purchase. It is to make sure your essentials are not quietly taking over the whole budget.

Put 30% Toward Wants

The next part of the 50/30/20 budget is for wants.

Wants are the things that make life more enjoyable, but are not essential for basic living, work, or financial stability. This is the category for lifestyle spending.

Common wants include:

| Want | Examples |

|---|---|

| Eating out | Restaurants, coffee shops, takeaway |

| Entertainment | Movies, concerts, games, events |

| Shopping | Clothes, home decor, non-essential purchases |

| Subscriptions | Streaming services, paid apps, memberships |

| Travel | Weekend trips, vacations, hotel stays |

| Hobbies | Books, crafts, sports, fitness extras |

| Upgrades | Premium phone plans, luxury brands, convenience services |

For example, if your monthly take-home pay is $3,200, the 50/30/20 method gives you $960 for wants.

This category is not “bad spending.” A budget that removes every enjoyable thing usually does not last very long. You are allowed to have fun money. The point is to give it a limit so it does not accidentally take over your savings, bills, or debt payoff.

Wants can also be tricky because they sometimes hide inside needs. Food is a need, but restaurant meals are usually wants. Internet may be a need, but multiple streaming subscriptions are wants. Transportation may be a need, but upgrading your car mainly for comfort or status may fall partly into wants.

A helpful way to check is to ask: “Could I reduce or pause this if I needed to?”

If the answer is yes, it probably belongs in wants.

Put 20% Toward Savings and Extra Debt Payments

The final part of the 50/30/20 budget is for savings and extra debt payments.

This is the money that helps you build stability, prepare for future expenses, and make progress beyond your regular monthly bills.

Common examples include:

| Savings or Debt Goal | Examples |

|---|---|

| Emergency fund | Saving for unexpected expenses |

| Sinking funds | Car repairs, holidays, annual bills, school costs |

| Retirement | Workplace retirement account, IRA, pension contributions |

| Investing | Long-term investment goals |

| Extra debt payments | Paying more than the minimum on credit cards, loans, or student debt |

| Short-term savings | Car, house deposit, wedding, travel, moving costs |

For example, if your monthly take-home pay is $3,200, the 50/30/20 method gives you $640 for savings and extra debt payments.

One important detail: minimum debt payments usually belong in needs because they are required monthly obligations. Extra payments above the minimum can go in this 20% category.

So if your credit card minimum payment is $100 and you choose to pay an extra $150, the $100 would usually count as a need, while the extra $150 would count toward savings and debt payoff.

This category is where your budget starts working for future you. Even if you cannot reach the full 20% right now, starting with a smaller amount still counts. Saving $50 consistently is better than waiting for the “perfect” month that never seems to arrive.

50/30/20 Budget Example

Let’s put the full method together with a simple example.

Say your monthly take-home pay is $3,200. Using the 50/30/20 budget, your money would be divided like this:

| Category | Percentage | Monthly Amount |

|---|---|---|

| Needs | 50% | $1,600 |

| Wants | 30% | $960 |

| Savings and extra debt payments | 20% | $640 |

| Total | 100% | $3,200 |

Here’s what that could look like in a real monthly budget:

| Category | Amount |

|---|---|

| Rent | $1,050 |

| Groceries | $300 |

| Utilities | $120 |

| Transportation | $80 |

| Insurance | $50 |

| Needs total | $1,600 |

| Eating out | $180 |

| Subscriptions | $70 |

| Shopping and personal spending | $250 |

| Entertainment | $150 |

| Miscellaneous wants | $310 |

| Wants total | $960 |

| Emergency fund | $250 |

| Extra debt payment | $200 |

| Sinking funds | $190 |

| Savings and extra debt payments total | $640 |

This is only an example, not a perfect template.

Your rent may be higher. Your transportation costs may be lower. You may need more room for debt payoff, childcare, or groceries. The point is to use the 50/30/20 split as a quick starting framework, then adjust it to match your real numbers.

A budget is more useful when it reflects your actual life, not someone else’s neat-looking table.

Is the 50/30/20 Rule Realistic?

The 50/30/20 rule is realistic for some people, but not for everyone exactly as written.

It works best when your essential expenses are close to 50% of your take-home pay. If your rent, groceries, insurance, transport, and minimum debt payments already take up most of your income, the original split may feel too tight.

That does not mean the method is useless. It just means you may need to adjust it.

For example, your current budget might look more like this:

| Category | Percentage |

|---|---|

| Needs | 65% |

| Wants | 25% |

| Savings and extra debt payments | 10% |

That may not be the “classic” 50/30/20 split, but it still gives you useful information. It shows that your essentials are taking a larger share of your income, which explains why saving 20% may feel difficult right now.

The 50/30/20 rule works best as a starting point, not a pass-or-fail test.

If your numbers do not fit perfectly, start with where you are. Then look for small ways to reduce flexible spending, build savings gradually, or adjust the percentages until your budget feels more realistic.

What If Your Needs Are More Than 50%?

If your needs are more than 50%, do not quit the budget right away.

This is common, especially if housing, groceries, childcare, insurance, or transportation costs are high. The 50/30/20 rule is a helpful target, but it does not always match real life perfectly.

Start by looking at your current split.

| Current Split | What It Means |

|---|---|

| 60% needs / 25% wants / 15% savings | Slightly stretched, but still workable |

| 70% needs / 20% wants / 10% savings | Essentials are taking most of the budget |

| 80% needs / 15% wants / 5% savings | Budget may need bigger adjustments or income support |

Once you know your numbers, take one step at a time.

First, check whether everything in your needs category is truly a need. Rent, basic groceries, utilities, insurance, and minimum debt payments usually belong there. But upgraded services, premium plans, frequent delivery fees, or convenience spending may partly belong in wants.

Next, protect your essentials. Do not cut important bills, insurance, food, or minimum debt payments just to force the numbers into 50/30/20. A budget should help you stay stable, not make life riskier.

Then, adjust the percentages temporarily. You might use:

| Adjusted Budget | When It May Help |

|---|---|

| 60/25/15 | Your essentials are a little high |

| 70/20/10 | Your income is tight right now |

| 80/15/5 | You need a short-term survival budget |

Even if you cannot save 20% yet, saving a smaller amount still matters. Starting with 5% or 10% can help you build the habit while you work toward more breathing room.

The goal is progress, not forcing your budget into a shape that does not fit.

Pros and Cons of the 50/30/20 Budget

The 50/30/20 budget is popular because it is simple, but simple does not always mean perfect for every situation.

Here’s a quick look at the benefits and limits.

| Pros | Cons |

|---|---|

| Easy to understand | May not fit high-cost areas |

| Beginner-friendly | Too broad if you need detailed tracking |

| Gives room for wants | Needs and wants can be confusing |

| Encourages regular saving | Harder if your income changes often |

| Works without a complicated spreadsheet | May need adjusting if you have heavy debt |

| Helps you see your overall money balance | Does not automatically control overspending in specific categories |

The biggest strength of the 50/30/20 budget is that it gives you a clear starting point. You can quickly see whether your money is mostly going toward essentials, lifestyle spending, or future goals.

The biggest weakness is that it may be too broad if you need close control. For example, if your grocery spending, takeout, or shopping keeps creeping up, a three-category budget may not give you enough detail.

In that case, you can still use 50/30/20 as your big-picture plan, then add smaller limits inside each category.

Who Should Use the 50/30/20 Budget?

The 50/30/20 budget is a good fit if you want a simple way to organize your money without tracking every small category.

It works especially well if your income is fairly steady and your essential expenses are not taking up most of your paycheck.

The 50/30/20 budget may work well if you:

- Are new to budgeting

- Want a simple starting point

- Have steady monthly income

- Prefer broad categories instead of detailed tracking

- Want a balance between bills, fun money, and savings

- Need a quick way to see where your money is going

This method can also work well if you are not ready for a strict budget yet. It gives you structure, but it does not ask you to plan every dollar in detail.

The 50/30/20 budget may not be ideal if you:

- Have very high essential expenses

- Live on a tight or low income

- Have irregular income

- Are dealing with heavy debt

- Overspend in specific categories

- Need detailed control over every dollar

For example, if your rent, groceries, childcare, and minimum debt payments already take up 75% of your take-home pay, the classic 50/30/20 split may feel unrealistic.

That does not mean you cannot use the method at all. You may just need to adjust the percentages or use it as a quick check instead of a strict monthly rule.

How to Adjust the 50/30/20 Rule to Fit Real Life

The 50/30/20 rule is useful, but it is not the only split you are allowed to use.

If the classic version does not fit your income, expenses, or goals right now, adjust the percentages instead of dropping the budget completely.

Better Money Habits explains that you can tweak the percentages based on your circumstances, such as living in an expensive city or saving for a larger goal.

Here are a few examples:

| Situation | Possible Adjustment |

|---|---|

| Your essentials are higher than 50% | Try 60/25/15 |

| Your income is tight right now | Try 70/20/10 temporarily |

| You want to save more aggressively | Try 50/20/30 |

| You are focused on debt payoff | Try 50/20/30, with more going toward extra payments |

| Your income changes monthly | Use your lowest typical income as the base |

| You live in a high-cost area | Start with your real numbers, then improve slowly |

The exact percentages matter less than the habit behind them.

You are trying to make sure your money has a clear direction: essentials first, some room for life, and something going toward future you.

For example, if your current split is 65/25/10, start there. Then you might aim for 60/25/15 over time by reducing one flexible expense, negotiating a bill, increasing income, or putting small raises toward savings instead of lifestyle upgrades.

A flexible budget you can actually use is better than a perfect formula you abandon after two weeks.

50/30/20 Budget vs. Zero-Based Budget

The 50/30/20 budget and zero-based budgeting can both help you manage your money, but they work in different ways.

The 50/30/20 budget gives you broad spending limits. Zero-based budgeting gives every dollar a specific job.

| 50/30/20 Budget | Zero-Based Budget |

|---|---|

| Uses three broad categories | Uses detailed categories |

| Splits income by percentages | Assigns every dollar before spending |

| Easier for beginners | More hands-on |

| Good for big-picture planning | Good for tight control |

| Requires less tracking | Requires more regular updates |

| Works well for steady income | Works well when you need clarity |

The 50/30/20 budget may be better if you want a simple structure without tracking every tiny expense.

Zero-based budgeting may be better if your money feels hard to control, your paycheck disappears too quickly, or you want to plan every dollar before the month begins.

You can also combine both. Use the 50/30/20 rule as your big-picture target, then use zero-based budgeting inside those categories if you want more detail.

Common Mistakes to Avoid With the 50/30/20 Budget

The 50/30/20 budget is simple, but a few small mistakes can make it harder to use.

- Using gross income instead of take-home pay: Build your budget around the money that actually reaches your bank account after taxes and deductions.

- Calling too many wants “needs”: Groceries are a need, but regular food delivery usually belongs in wants. A basic phone plan may be a need, but the most expensive plan with extras may not be.

- Forgetting irregular expenses: Annual subscriptions, car repairs, holiday gifts, insurance renewals, and school costs can throw off your budget if you do not plan for them.

- Putting all debt payments in one place: Minimum debt payments usually count as needs. Extra payments can go in the 20% savings and debt payoff category.

- Treating the percentages as strict rules: If your current split is 60/25/15, start there and improve gradually. The goal is progress, not perfect math.

Start With the Split You Can Actually Use

The 50/30/20 budget is a helpful starting point, but it does not have to be perfect on day one.

Start by calculating your current split. How much of your take-home pay goes to needs, wants, and savings or extra debt payments right now?

Maybe your numbers are close to 50/30/20. Maybe they look more like 65/25/10. Either way, that gives you something useful: a clear starting point.

From there, choose one small adjustment.

You might reduce one flexible expense, start a small sinking fund, move $25 into savings each payday, or put a little extra toward debt. Small changes are easier to repeat, and repeated changes are what actually improve your budget.

The 50/30/20 rule gives you a simple way to check whether your money is balanced. Use it as a guide, adjust it when needed, and keep improving one small part of your budget at a time.

Ready to compare this with other options? Read our guide to 7 budgeting methods to find the system that fits your money best.

FAQs About the 50/30/20 Budget Method

Is the 50/30/20 budget weekly or monthly?

You can use the 50/30/20 budget weekly, biweekly, or monthly.

Most people use it monthly because rent, utilities, subscriptions, and loan payments are often monthly expenses. If you get paid weekly or biweekly, you can still add up your expected take-home pay for the month and apply the 50/30/20 split from there.

Is the 50/30/20 rule based on gross or net income?

The 50/30/20 rule is usually based on net income, also called take-home pay.

That means you use the money that actually reaches your bank account after taxes and payroll deductions, not your full salary before deductions.

Do debt payments count as needs or savings?

Minimum debt payments usually count as needs because they are required monthly obligations.

Extra debt payments can go in the 20% savings and extra debt payments category because they help you pay debt down faster.

What if I cannot save 20%?

Start with what you can.

If 20% is not realistic right now, try 5% or 10% and build from there. Saving a smaller amount consistently is still better than waiting until your budget looks perfect.

Is the 50/30/20 budget good for low income?

The 50/30/20 budget can be a helpful starting point for low income, but the percentages may need adjusting.

If essentials take up more than 50% of your income, start with your real numbers first. Even a 70/20/10 split can give your money more structure while you work toward more breathing room.

Is the 50/30/20 budget better than zero-based budgeting?

It depends on how much structure you want. The 50/30/20 budget is simpler because it uses three broad categories. Zero-based budgeting gives more control because every dollar gets assigned a specific job.

Can I combine the 50/30/20 budget with another method?

Yes. You can use 50/30/20 as your big-picture plan and combine it with another method for more control.

For example, you could use envelope budgeting for groceries and eating out, or use zero-based budgeting inside each 50/30/20 category.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.