Payday brings relief, but that relief does not always last long.

Your paycheck lands, a few bills go out, groceries cost more than expected, and a couple of small purchases sneak in. Before you know it, the money you planned to stretch until the next payday is already running low.

If that sounds familiar, you are not alone. The issue is not always careless spending. Sometimes your paycheck simply does not have a clear plan before everyday expenses start pulling from it.

A simple payday routine can help you decide what happens first: bills, savings, essentials, debt, and spending money. That way, your paycheck has a job before random spending gets a chance to take over.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

What You Need to Know First

- A payday routine helps you give your paycheck a clear plan before spending starts.

- Start by setting aside money for bills, essentials, savings, and debt before flexible spending.

- Splitting your spending money by week can help your paycheck last until the next payday.

- A short waiting period before non-essential purchases can reduce payday impulse spending.

- The goal is not to control every dollar perfectly. It is to stop your paycheck from disappearing without a plan.

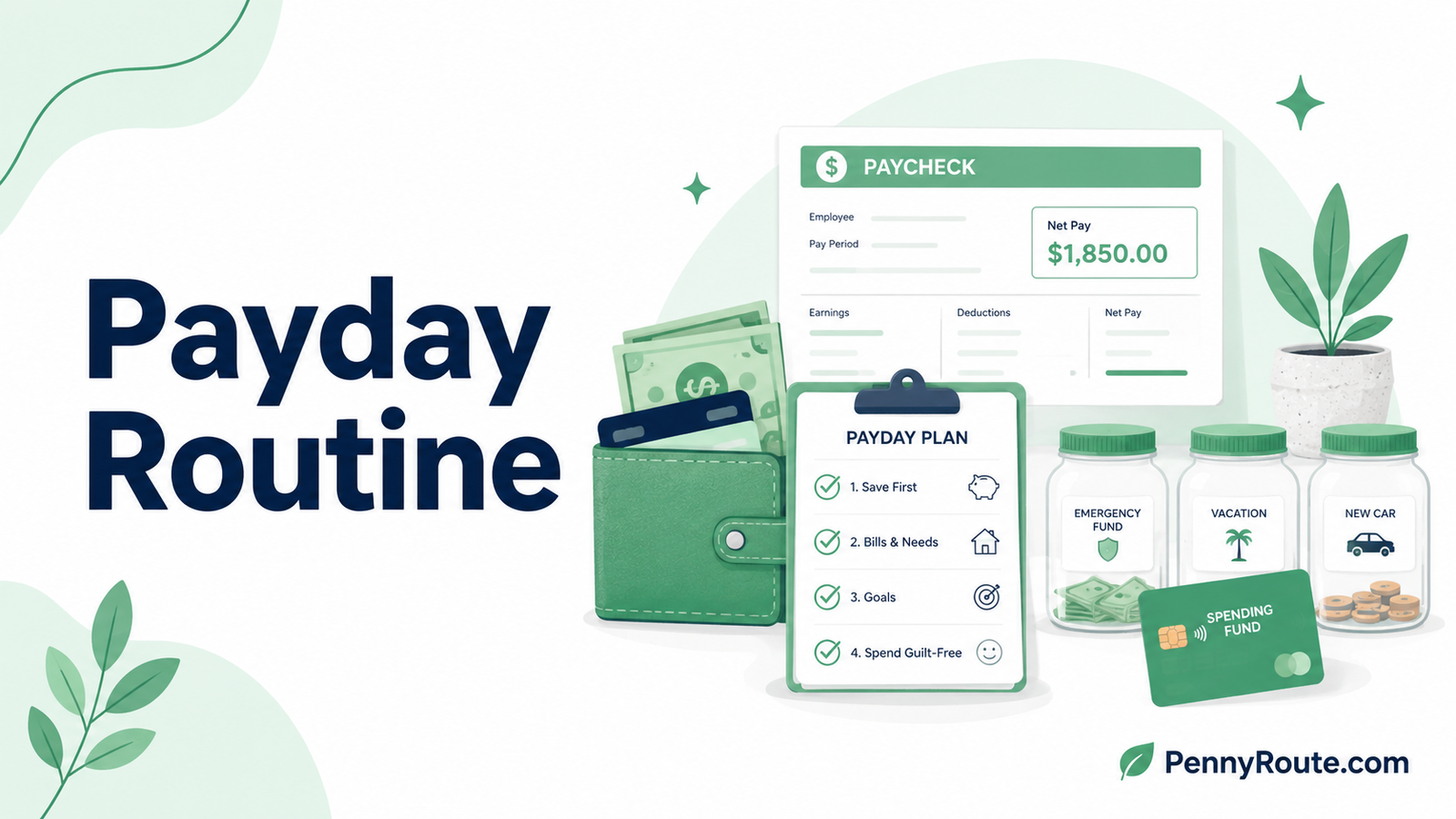

What Is a Payday Routine?

A payday routine is a simple set of steps you follow every time you get paid. Instead of letting your paycheck sit in your account and hoping it lasts, you decide where the money needs to go before you start spending. That usually means setting aside money for bills, essentials, savings, debt payments, and flexible spending.

Think of it as a quick money check-in for your paycheck.

Your routine does not need to be complicated. It can take 10 minutes and still make a big difference. The main goal is to know what money is already spoken for and what money is actually available to spend.

A payday routine can work whether you are paid weekly, biweekly, twice a month, or on an irregular schedule. The exact numbers may change, but the habit is the same: pause, plan, then spend.

A payday routine is one of the easiest better money habits to build because it gives your money a job as soon as it arrives.

Why Your Paycheck Disappears So Fast

Your paycheck may disappear quickly because the full balance looks available, even when part of it already belongs to bills, groceries, debt payments, and upcoming expenses.

That is where payday gets tricky. Your account balance may say one number, but your real spending money is usually much smaller.

For example, if you get paid $1,800, it may feel like you have $1,800 to work with. But if $900 needs to go toward rent, utilities, insurance, and debt payments before your next payday, you do not really have $1,800 available to spend.

A few common reasons paychecks disappear fast include:

- Spending before checking upcoming bills

- Forgetting about expenses due later in the month

- Treating small purchases as harmless

- Keeping bill money and spending money in the same account

- Buying things right after payday because the balance looks higher

- Using credit cards to cover the gap after overspending

This does not mean you need a perfect budget. It means your paycheck needs a quick plan before everyday spending starts pulling from it.

Payday Routine: 6 Steps to Follow Every Time You Get Paid

A payday routine works best when it is simple enough to repeat. You do not need a complicated spreadsheet or a perfect budget. You just need a clear order for what happens when your paycheck arrives.

Here are six steps you can follow every payday.

Check the Paycheck Amount First

Start by checking how much money actually landed in your account.

This is especially important if your hours change, you earn overtime, you have deductions, or your income is not the same every pay period. Do not build your plan around what you expected to receive. Build it around the amount that actually arrived.

If something looks wrong, check your pay stub or contact your employer before moving money around. A small paycheck error can create a bigger problem if you only notice it after bills are due.

Set Aside Money for Bills Before Spending

Before you buy anything extra, look at which bills are due before your next payday.

This may include rent or mortgage, utilities, phone bill, insurance, loan payments, subscriptions, childcare, or credit card minimums. If the bill is coming due before your next paycheck, that money should be treated as already spoken for.

You can keep it simple:

- List bills due before your next payday

- Add up the total

- Move that amount to a separate bills account if you use one

- If not, write it down so you know that money is not available for spending

This one habit can prevent a lot of payday stress. Your account balance may still look healthy, but now you know which part is truly available and which part is waiting for bills.

Move Savings Before You Spend

If you wait to save whatever is left at the end of the pay period, there may not be much left.

That is why it helps to move savings soon after you get paid. This does not have to be a large amount. Even $10, $25, or $50 can help you build the habit.

Start with one savings goal if money is tight. For many beginners, that could be a starter emergency fund. If you already have one, you might save for car repairs, annual bills, holiday spending, or another upcoming expense.

The point is simple: give savings a place in your payday routine before everyday spending gets first chance at the money.

MyMoney.gov’s pay yourself first guidance also explains that saving can be easier when you set money aside each pay period before you are tempted to spend it.

Cover Groceries, Gas, and Essentials

After bills and savings, set aside money for the essentials you need before your next payday.

This usually includes groceries, gas or transportation, basic household items, prescriptions, school costs, or anything else your household needs to function. These expenses may not always be fixed, but they still need a place in your paycheck plan.

A simple way to handle this is to estimate based on your normal spending.

For example, if you usually spend around $150 a week on groceries and gas, and your next payday is two weeks away, set aside about $300 for those essentials before deciding how much flexible spending money you have.

This step helps you avoid the classic payday problem: spending too freely at the start, then trying to stretch a tiny amount for groceries at the end.

Split Your Spending Money by Week

Once bills, savings, debt payments, and essentials are covered, look at what is left for flexible spending.

This is the money you can use for things like eating out, entertainment, coffee, hobbies, small personal purchases, or anything that is not already planned.

The trick is not to spend it all in the first few days.

If you have $240 left until your next payday and you get paid every two weeks, split it into $120 per week. You can even break it down further if daily limits help you stay aware.

This makes your spending money easier to manage because you are not relying on one big number. You are giving yourself smaller limits that match how long the money needs to last.

Use a 24-Hour Pause for Non-Essential Purchases

Payday can make extra purchases feel easier to justify because your balance is higher than usual.

Before buying something non-essential, give yourself a short pause. For small purchases, 24 hours may be enough. For bigger purchases, wait a few days if you can.

During that pause, ask yourself:

- Do I still want this after waiting?

- Can I buy it without touching bill money or savings?

- Will this make the rest of the pay period harder?

- Is there a cheaper option that would work?

This does not mean you can never buy anything fun. It simply gives you time to decide instead of letting the higher payday balance make the decision for you.

Payday Routine Example

Here is a simple example of how a payday routine could look.

Let’s say your take-home paycheck is $1,800, and your next payday is two weeks away.

| Payday Step | Example Amount |

|---|---|

| Bills due before next payday | $850 |

| Groceries, gas, and essentials | $300 |

| Savings | $100 |

| Extra debt payment | $75 |

| Flexible spending | $300 |

| Small buffer | $175 |

These numbers are only an example. Your paycheck, bills, and spending needs may look completely different.

The main idea is to separate the money before you start spending. In this example, the full paycheck is $1,800, but only $300 is flexible spending money. Without a payday routine, it would be easy to treat the full account balance like available money and accidentally spend money needed for bills or essentials later.

If your paycheck feels hard to split, starting with a simple budget can make your payday routine easier to follow.

What If Your Paycheck Is Already Stretched?

A payday routine helps, but it cannot magically fix a paycheck that is already too small for your expenses.

If most of your money is gone as soon as you get paid, start with priorities. Cover the essentials first: housing, utilities, food, transportation, insurance, and minimum debt payments. These are the expenses that keep your basic life running.

Then look for one small adjustment before your next payday. That might mean pausing a subscription, planning cheaper meals, delaying a non-essential purchase, or using cash for flexible spending so you do not accidentally go over.

If a bill will be late, contact the company before the due date if possible. Some providers may offer payment plans, extensions, or hardship options.

Even if you can only save a small amount, try to save something when you can. A tiny buffer will not solve everything, but it can help you avoid relying on debt for every small surprise.

Payday Routine for Different Pay Schedules

Your payday routine may look a little different depending on how often you get paid. The habit stays the same, but the timing changes.

If You Get Paid Weekly

Weekly paychecks can be easier to manage because the next payday is close. Focus on the bills and essentials that need to be covered during that week.

Set aside money for any bill due before the next paycheck, then plan groceries, gas, and flexible spending for the next seven days. If possible, move a small amount into savings each week, even if it is only a few dollars.

If You Get Paid Biweekly

Biweekly paychecks need to stretch for about two weeks, so splitting your spending money is important.

After bills, savings, and essentials are covered, divide your flexible spending into two weekly amounts. This helps you avoid spending too much in week one and feeling stuck in week two.

If You Get Paid Twice a Month

If you are paid twice a month, your paydays may not always line up neatly with your bills.

One simple method is to assign certain bills to each paycheck. For example, the first paycheck might cover rent and utilities, while the second covers insurance, phone, groceries, and savings.

This works best when you keep a list of due dates so you know which paycheck needs to cover which bills.

If Your Income Changes

If your income changes from week to week, build your payday routine around your lowest expected income.

Start with a basic version of your budget that covers essentials only. During higher-income weeks, use extra money to build a buffer, catch up on bills, save for irregular expenses, or pay down debt.

Variable income can make planning harder, but a simple routine still helps. The goal is to protect your essentials first, then decide what extra money should do before it disappears.

Payday Mistakes That Make Your Paycheck Disappear Faster

A payday routine works better when you know what usually throws it off. Here are a few common mistakes to watch for:

- Spending before checking which bills are due before your next payday.

- Treating your full account balance like spending money.

- Forgetting irregular expenses, such as annual subscriptions, car registration, gifts, school costs, or insurance premiums.

- Keeping bill money, savings, and spending money in one account without tracking what each amount is for.

- Using credit cards to cover everyday spending after the paycheck runs low.

You do not need to fix every mistake at once. Start with the one that causes the most stress, then adjust your next payday routine around it.

Payday Routine Checklist

This checklist does not need to be perfect. The goal is to give your paycheck a clear plan before the money starts moving in different directions.

If you like a more detailed system, zero-based budgeting can help you give every dollar a job before the month begins.

Keep Payday Simple, Not Perfect

A payday routine does not need to control every dollar or turn payday into a long budgeting session.

It just needs to help you pause before spending, cover the most important things first, and know what money is actually available until the next paycheck.

Some pay periods will still be messy. A bill may be higher than expected, groceries may cost more, or you may spend more than planned. That does not mean the routine failed. It means you adjust and try again next payday.

Start with the basics: check your paycheck, cover bills, save something if you can, plan essentials, and split what is left. Small payday habits can make your money feel less rushed, less random, and a little easier to manage.

FAQs About Payday Routines

What is a payday routine?

A payday routine is a simple set of steps you follow every time you get paid. It helps you plan bills, savings, essentials, debt payments, and spending money before your paycheck starts disappearing.

What should I do first when I get paid?

Start by checking the paycheck amount that actually arrived. Then review which bills are due before your next payday so you know how much money is already spoken for.

How do I stop spending money right after payday?

Set aside bill money first, move something into savings, and decide how much flexible spending money you have left. If payday spending is a problem, use a 24-hour pause before buying anything non-essential.

Should I save money or pay bills first on payday?

Cover essential bills first so you avoid late fees and missed payments. After that, try to move even a small amount into savings before spending on non-essentials.

How do I budget a biweekly paycheck?

List the bills due before your next paycheck, set aside money for groceries and transportation, move savings if possible, then split your remaining flexible spending into two weekly amounts.

What if my paycheck is not enough for all my bills?

Start with essentials like housing, utilities, food, transportation, insurance, and minimum debt payments. If a bill may be late, contact the provider before the due date and ask about payment options.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.