Saving money can feel frustrating when your budget already looks full. You want to put money aside, but after bills, groceries, gas, and everyday expenses, there may not be much left to save.

The 100 envelope challenge gives you a simple way to turn saving into small, visible steps. Instead of guessing how much to save, you follow numbered envelopes and build momentum as your savings grow.

By the end of the full challenge, you can save $5,050. But the best version is the one that fits your real life without making your bills harder to manage.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

Quick Overview: 100 Envelope Challenge

- The 100 envelope challenge helps you save money by filling envelopes numbered 1 to 100.

- If you complete all 100 envelopes, you save $5,050.

- The full challenge is often done in 100 days, but you can slow it down to fit your budget.

- You can use cash envelopes, a printable tracker, or a digital savings account.

- The challenge works best when you use extra money, not money needed for bills, groceries, rent, or debt payments.

- Smaller versions, like the 50 envelope challenge or half challenge, can make saving feel more realistic.

What Is the 100 Envelope Challenge?

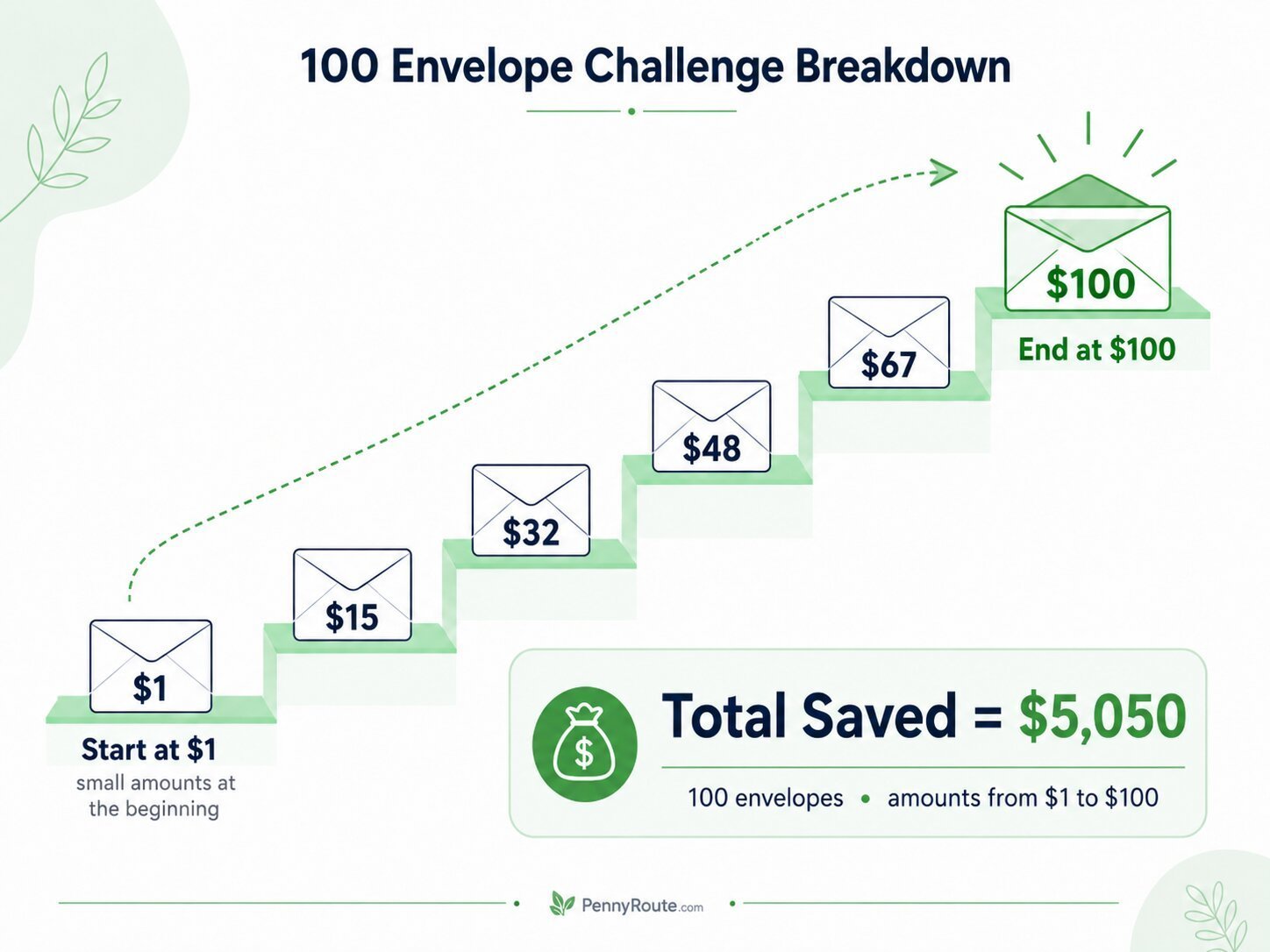

The 100 envelope challenge is a savings challenge where you label 100 envelopes with the numbers 1 through 100. Each envelope number tells you how much money to save.

For example, envelope 1 gets $1, envelope 25 gets $25, and envelope 100 gets $100. Once every envelope is filled, you will have saved $5,050.

The challenge is popular because it makes saving money feel more visual. Instead of trying to “save more” in a vague way, you have a clear number to follow each time you pick an envelope.

You can do the challenge with physical cash, a printable tracker, or a separate savings account. The method can change, but the basic idea stays the same: choose a number, save that amount, and mark it complete.

How Does the 100 Envelope Challenge Work?

The 100 envelope challenge works by giving each savings step a clear dollar amount. You do not have to decide what to save each time. The envelope you choose tells you what to put aside.

This is sometimes called the 100 day envelope challenge when people complete one envelope per day.

Here is the basic process:

- Get 100 envelopes or create a simple tracker.

- Number them from 1 to 100.

- Pick one envelope at a time.

- Save the amount written on that envelope.

- Mark that number as complete.

- Keep going until all 100 numbers are finished.

You can pick envelopes randomly to make it feel more like a challenge, or you can go in order if you prefer to plan ahead. Random picks can be fun, but going in order may be easier if you want more control over your budget.

For example, if you pick envelope 12, you save $12. If you pick envelope 87, you save $87. Each completed envelope moves you closer to the full $5,050 total.

How Much Money Do You Save With the 100 Envelope Challenge?

If you complete the full 100 envelope challenge, you save $5,050.

That total comes from adding every envelope amount from 1 to 100:

$1 + $2 + $3 + … + $100 = $5,050

The average envelope amount is $50.50. So if you try to finish the challenge in 100 days, you are saving an average of $50.50 per day.

That is why the challenge can feel exciting at first but harder as the bigger numbers come up. Saving $8 or $19 may feel easy on a normal week. Saving $82, $94, or $100 may need more planning.

Here is a simple breakdown:

| Challenge Pace | Approximate Savings Needed |

|---|---|

| 100 days | $50.50 per day on average |

| About 15 weeks | Around $337 per week |

| 8 biweekly paychecks | Around $631 per paycheck |

| 4 months | Around $1,263 per month |

These numbers are not meant to scare you away. They help you choose a version that fits your real budget before you start.

Is the 100 Envelope Challenge Realistic for Your Budget?

The 100 envelope challenge is simple, but that does not automatically make it easy.

Saving $5,050 in 100 days can be a lot if your budget is already tight. Before you start, look at what is left after your must-pay expenses, such as rent or mortgage, utilities, groceries, minimum debt payments, insurance, and transportation.

If you usually have $100 left after every paycheck, trying to save $600 or $700 from that same paycheck may create stress instead of progress. The challenge should help you build savings, not make you fall behind on bills.

A better approach is to treat the challenge as flexible. You can stretch it over several months, fill envelopes only on payday, use smaller amounts, or start with the 50 envelope challenge instead.

The safest version is the one you can keep doing without using credit cards to cover normal expenses, skipping bills, or draining money you already set aside for emergencies.

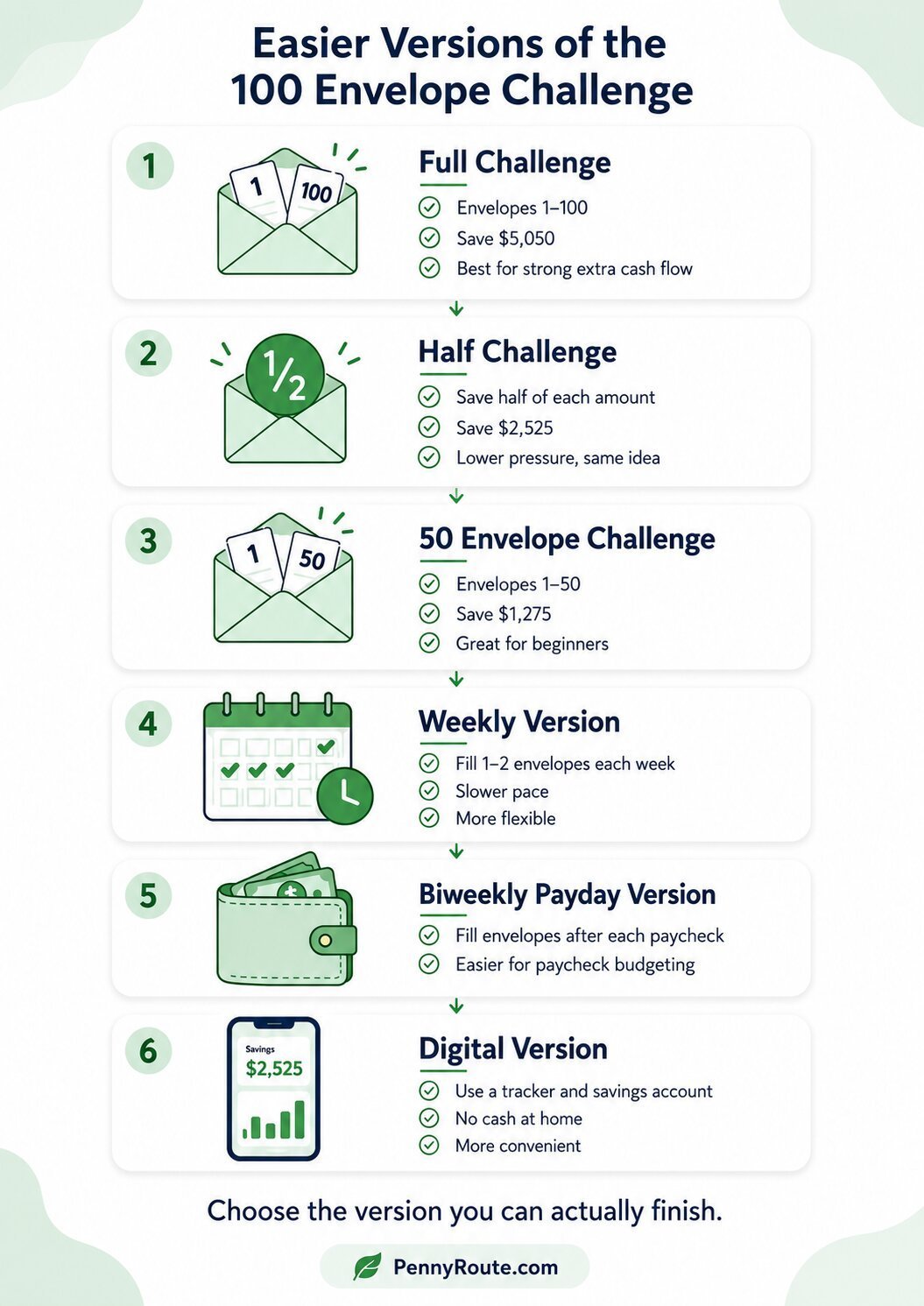

Easier Versions of the 100 Envelope Challenge

The full 100 envelope challenge is not the only way to do it. You can adjust the challenge and still build a strong savings habit.

The goal is not to copy the hardest version. The goal is to choose a version you can finish without making your budget feel squeezed.

| Version | How It Works | Total Saved | Best For |

|---|---|---|---|

| Full 100 envelope challenge | Save the amount on envelopes numbered 1 to 100 | $5,050 | People with steady extra cash flow |

| Half challenge | Save half of each envelope amount | $2,525 | People who want the same structure with less pressure |

| 50 envelope challenge | Use envelopes numbered 1 to 50 | $1,275 | Beginners or lower-income budgets |

| Weekly version | Fill one or two envelopes each week | $5,050 eventually | People who need a slower pace |

| Biweekly payday version | Fill envelopes after each paycheck | Flexible | People who budget around paydays |

| Digital version | Track numbers and transfer money into savings | Flexible | People who do not want to keep cash at home |

Which Version Should You Choose?

Choose the full version only if you have enough extra money after your regular expenses. It can work well for a short-term goal, but it should not compete with rent, groceries, insurance, or minimum debt payments.

Choose the 50 envelope challenge or half challenge if you want something more manageable. You will save less than $5,050, but you may be more likely to finish — and finishing a smaller challenge is better than quitting a bigger one halfway through.

Choose the weekly or biweekly version if your income comes in paychecks. This makes the challenge easier to plan because you can decide how much to save after each payday instead of trying to save every single day.

Choose the digital version if you want less cash around the house. You can still use the envelope numbers, but move the money into a separate savings account instead.

Cash, Printable, or Digital: Ways to Track the Challenge

You do not need a perfect setup to start the 100 envelope challenge. The best tracking method is the one you will actually use.

Some people like the feeling of putting cash into real envelopes. Others prefer a printable tracker or a digital savings account. All three can work as long as you can clearly see which numbers are done and how much you have saved.

Cash Envelope Method

The cash method is the classic version of the challenge. You label 100 envelopes, choose one at a time, and place the matching amount of cash inside.

This can be motivating because your progress is visible. Watching the envelopes fill up can make saving feel more real than numbers sitting in an app.

The downside is safety. If you complete the full challenge, you may have thousands of dollars in cash at home. Keep that in mind before choosing this method. If cash helps you stay motivated, consider depositing the money into your bank account every few weeks instead of holding the full amount until the end.

Printable Tracker Method

A printable tracker is a simple option if you do not want 100 envelopes sitting around. You can print a chart with numbers 1 through 100, then color in or check off each number after you save that amount.

A 100 envelope challenge printable can help you mark each number as complete without keeping 100 envelopes around.

This works well if you prefer a cleaner setup. You can still use cash, but you can also transfer the money to savings and use the tracker only to mark progress.

A good tracker should include:

- numbers 1 through 100

- a place to mark completed numbers

- total saved so far

- savings goal or reason for doing the challenge

Adding the reason matters. Saving for “emergency fund,” “car repairs,” or “moving costs” feels more meaningful than saving just because a chart said so.

Digital 100 Envelope Challenge

The digital 100 envelope challenge uses the same idea without physical cash. Instead of putting money into envelopes, you transfer the matching amount into a separate savings account.

For example, if you pick number 42, you transfer $42. Then you mark 42 as complete on a checklist, spreadsheet, notes app, or printable tracker.

This version is safer if you do not want to keep cash at home. It can also help your money stay separate from everyday spending, which makes it less tempting to use for random purchases.

Some financial experts also point out that moving money into a savings account can help avoid the downsides of storing large amounts of cash at home.

To make the digital version easier, you can:

- use a separate savings account

- rename the account “100 Envelope Challenge” if your bank allows it

- use a random number generator to pick numbers

- update your tracker right after each transfer

- check your progress once a week

The method matters less than the habit. Whether you use envelopes, a printable, or a savings account, the point is to save the amount, mark it done, and keep moving.

What Should You Use the $5,050 For?

Finishing the 100 envelope challenge is a big win, but the money should have a clear job once you save it.

Without a plan, $5,050 can slowly disappear into regular spending. A little here, a little there, and suddenly your savings challenge turns into “where did that go?” Not ideal. Your future self deserves better.

Here are smart ways to use the money:

- Build or grow your emergency fund: Use the money for unexpected expenses like medical bills, job loss, urgent home repairs, or car problems.

- Pay down credit card debt: If you have high-interest debt, using part of your savings to lower the balance can reduce financial pressure.

- Start a sinking fund: Put the money toward planned expenses like holidays, annual insurance, car repairs, school costs, or home maintenance.

- Create a bill buffer: Keep extra money in your checking account so one late paycheck or surprise bill does not throw off your entire month.

- Save for a specific goal: Use it for moving costs, a used car, a vacation, pet emergencies, or another goal that matters to your life.

You do not have to use the full amount for one thing. For example, you might put $2,000 toward an emergency fund, $1,500 toward credit card debt, and keep $1,550 for upcoming expenses.

The best use depends on your situation. If you have no emergency savings, start there. If high-interest debt is costing you money every month, that may deserve attention too. The point is to give your savings a purpose before it blends back into everyday spending.

Pros and Cons of the 100 Envelope Challenge

The 100 envelope challenge can be a helpful way to save money, but it is not perfect for every budget. Before you start, it helps to look at both sides.

| Pros | Cons |

|---|---|

| Simple to understand | The full version can feel too aggressive |

| Makes saving feel visual and motivating | Larger envelope amounts may be hard to manage |

| Can help you save $5,050 if completed | Keeping a lot of cash at home can be risky |

| Easy to adjust for different budgets | Cash does not earn interest while sitting in envelopes |

| Works with cash, printable trackers, or digital savings | It may not work well if your budget is already stretched |

The biggest benefit is that the challenge gives your savings a clear system. You are not just telling yourself to “save more.” You are following a number, marking progress, and watching your savings grow.

The biggest downside is that the full version can put pressure on your cash flow. If the challenge makes you rely on credit cards, skip bills, or feel behind every week, it is no longer helping.

Use the pros as motivation, but pay close attention to the cons. A savings challenge should make your money feel more stable, not more stressful.

100 Envelope Challenge vs. Other Savings Challenges

The 100 envelope challenge is not the only way to save money. It works well for people who like a clear number-based system, but another savings challenge may fit better if your budget needs more flexibility.

| Savings Challenge | How It Works | Best For |

|---|---|---|

| 100 envelope challenge | Save amounts from $1 to $100 until you reach $5,050 | People who want a bigger short-term savings goal |

| 50 envelope challenge | Save amounts from $1 to $50 until you reach $1,275 | Beginners or anyone who wants a smaller goal |

| 52-week money challenge | Save a set amount each week for one year | People who prefer slow, steady progress |

| No-spend challenge | Pause non-essential spending for a set time | People who want to find extra money in their budget |

| Sinking fund | Save gradually for a specific planned expense | People preparing for known costs like car repairs or holidays |

The 100 envelope challenge is best when you want a structured goal and can handle changing savings amounts. A 52-week challenge may feel easier if you prefer a slower pace. A no-spend challenge can work well if your main issue is impulse spending.

A sinking fund is different because it is not really a challenge. It is a planned savings system for expenses you know are coming. If your goal is car repairs, holiday gifts, insurance, or pet costs, a sinking fund may be more useful after you finish the challenge.

You can also combine methods. For example, you might use a short no-spend challenge to free up extra money, then put that money toward your 100 envelope challenge.

Final Thoughts: Make the Challenge Fit Your Real Life

The 100 envelope challenge can be a simple way to save money because it gives every dollar a clear step.

But the challenge should support your budget, not compete with it. You can slow it down, cut the amounts in half, try the 50 envelope version, or do it digitally.

Start with the version you can finish comfortably. Saving $1,275, $2,525, or $5,050 is still progress when it helps you build a habit that lasts.

FAQs About the 100 Envelope Challenge

How much money do you save with the 100 envelope challenge?

You save $5,050 if you complete the full 100 envelope challenge. That total comes from saving every amount from $1 to $100.

How long does the 100 envelope challenge take?

The traditional version takes 100 days if you complete one envelope per day. You can also stretch it over several months by filling envelopes weekly, biweekly, or whenever your budget allows.

How do you save $5,000 in 100 days with envelopes?

You number 100 envelopes from 1 to 100, then save the dollar amount shown on each envelope. Once all envelopes are filled, the total comes to $5,050.

Can you do the 100 envelope challenge digitally?

Yes. Instead of using cash envelopes, you can use a checklist or spreadsheet and transfer the matching amount into a separate savings account. This can be safer than keeping a large amount of cash at home.

What is the 100 envelope challenge biweekly?

The biweekly version means you fill envelopes every two weeks, usually after payday. You can choose a few envelopes per paycheck based on what your budget can handle.

Is the 100 envelope challenge good for low income?

It can work for a lower income if you adjust the amounts or slow down the timeline. The full version may be too aggressive, so a 50 envelope challenge, half challenge, or payday version may be more realistic.

What is the 50 envelope challenge?

The 50 envelope challenge is a smaller version where you number envelopes from 1 to 50. If you complete all 50 envelopes, you save $1,275.

Where should I keep the money from the 100 envelope challenge?

You can keep it in cash envelopes for a short time, but a separate savings account is usually safer for larger amounts. A savings account can also help keep the money away from everyday spending.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.