Bad financial decisions are not always dramatic. Sometimes, they look manageable at first. A loan you plan to deal with later. A car payment that technically fits. A credit card balance that keeps getting pushed to next month.

The problem is that some money choices do not stay small. They can create extra costs, stress, debt, or missed opportunities long after the original decision is made.

That does not mean one mistake ruins everything. It means some decisions deserve a slower, clearer look before you commit.

Here we’ll talk about the common bad financial decisions that can cost you for years, plus better moves that can help you protect your future budget.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

What Are Bad Financial Decisions?

Bad financial decisions are money choices that can create long-term stress, extra costs, debt, or missed opportunities.

They are different from small everyday purchases. A $10 impulse buy may be annoying, but a loan, credit card balance, housing choice, or ignored bill can affect your budget for months or years.

That is why these decisions deserve more attention before you commit.

The goal is not to be perfect with money. The goal is to slow down before making choices that are hard to undo later.

Bad Financial Decisions vs. Bad Spending Habits

Bad financial decisions and bad spending habits are connected, but they are not the same thing.

Bad spending habits are usually repeated small purchases or patterns. For example, buying things because they are on sale, shopping when stressed, or making too many unplanned purchases.

Bad financial decisions are usually bigger choices that can affect your money for much longer. These may include taking on debt, buying more car than you can afford, co-signing a loan, or ignoring a growing credit card balance.

Both matter, but this article focuses on the bigger decisions. The kind that may seem fine today, then create pressure in your budget for months or years.

10 Bad Financial Decisions That Can Cost You

Some financial decisions do not look serious at first. They may even feel normal because many people make them.

But over time, they can take up more of your income, limit your choices, or make your budget harder to manage.

Here are common bad financial decisions to watch for, and what to do instead.

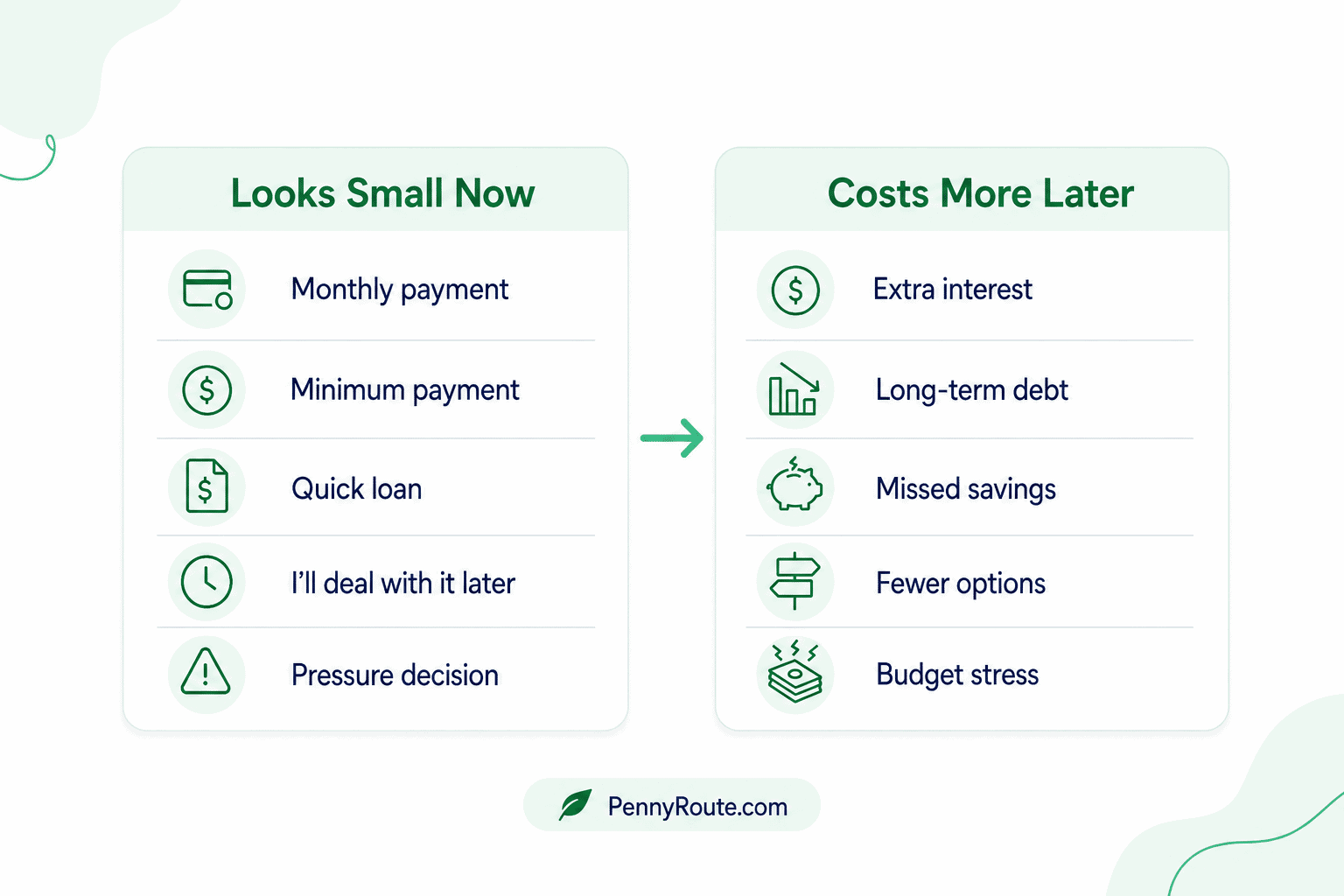

1. Taking On Debt Without a Payoff Plan

Debt can be useful in some situations, but taking it on without a clear plan can make your budget harder to manage.

This can happen with credit cards, personal loans, buy now pay later plans, store financing, or money borrowed from friends or family. The payment may seem small at first, but it still needs a place in your monthly budget.

Why it can hurt

Without a payoff plan, debt can linger much longer than expected. Interest, late fees, and extra payments can make the original purchase cost more over time.

Better move

Before borrowing, ask three questions:

- How much will I owe in total?

- What will the monthly payment be?

- When will this be fully paid off?

If you cannot answer those clearly, it may be better to pause before taking on the debt.

2. Buying a Car Based Only on the Monthly Payment

A car payment can look affordable when you only focus on the monthly number.

The problem is that the payment is just one part of the real cost. A longer loan term may lower the monthly payment, but it can also keep you in debt longer and increase the total amount you pay.

You also need to think about insurance, fuel, maintenance, registration, repairs, and possible loan interest.

Why it can hurt

A car that barely fits your monthly budget can become stressful once the full cost shows up. If the loan is long or the interest rate is high, you may also pay much more than the car’s sticker price.

Better move

Look at the total cost before saying yes. Compare the price, loan term, interest rate, insurance estimate, and expected running costs. A lower monthly payment is not always the better deal. If you are not in a rush, you can also make a plan to save up for a car so you borrow less or avoid stretching your budget.

3. Renting or Buying More Home Than Your Budget Can Handle

Housing is often the biggest monthly expense, so this decision can affect almost every other part of your budget.

A rent or mortgage payment may look manageable at first, especially if you focus only on the base payment. But the real cost can include utilities, insurance, property taxes, repairs, maintenance, parking, commuting, furniture, and moving costs.

Why it can hurt

When housing takes up too much of your income, there may be less room for savings, debt payments, groceries, transportation, and normal life. Even small surprise costs can become harder to handle.

Better move

Look at the full monthly cost before committing. Ask yourself, “Can I afford this and still pay for my other priorities without relying on debt?” If the answer is no, a lower-cost option may give your budget more breathing room.

4. Ignoring High-Interest Credit Card Balances

A credit card balance can become expensive when it keeps rolling over from month to month.

At first, the minimum payment may seem manageable. But if the interest rate is high, a large part of your payment may go toward interest instead of reducing the actual balance.

That can make the debt harder to pay off, especially if you keep adding new purchases to the card.

Why it can hurt

High-interest debt can grow quietly and take money away from other goals. The longer it sits, the more expensive it can become.

Better move

Make a debt payoff plan instead of only paying the minimum when possible. You can start by listing your balances, interest rates, and minimum payments, then choose a method that helps you stay consistent.

5. Skipping an Emergency Fund Completely

An emergency fund may not seem urgent when things are going fine.

But unexpected costs have a way of showing up at the worst time. A car repair, medical bill, job loss, urgent home expense, or surprise travel cost can quickly throw your budget off track.

Without any savings set aside, you may have to rely on credit cards, loans, late payments, or borrowed money to get through the problem.

Why it can hurt

Skipping an emergency fund can make one surprise expense turn into long-term debt. Even a small emergency can become more expensive if you have to borrow money to cover it.

Better move

Start with a small emergency fund goal, even if it is a few hundred dollars at first. You do not have to build it all at once. Set aside what you can, then keep adding to it until you have a stronger cushion.

6. Co-Signing a Loan Without Understanding the Risk

Co-signing can feel like a kind thing to do, especially when you want to help a family member or friend.

But co-signing is not just “supporting” someone’s application. You are agreeing to be responsible for the loan if the other person does not pay. That can affect your credit, your budget, and your relationship.

Why it can hurt

If payments are missed, the lender can come after you for the debt. Late payments may also show up on your credit report, even if you never used the money yourself.

Better move

Before co-signing, ask yourself, “Could I afford to make this payment if I had to?” If the answer is no, it may be better to say no or help in a smaller way that does not put your own finances at risk.

7. Using Retirement Savings for Non-Emergencies

Retirement savings can look like available money, especially when you are dealing with a cash shortage.

But using that money early can create more problems than it solves. Depending on the account and your situation, you may face taxes, penalties, or lost growth that could have helped your future self.

Why it can hurt

Taking money from retirement savings can cost you now and later. You may lose part of the withdrawal to taxes or penalties, and you also lose the chance for that money to keep growing over time.

Better move

Treat retirement savings as a last resort, not a backup checking account. Before using it, look for other options, such as adjusting your budget, pausing non-essential spending, speaking with your lender or service provider, or getting qualified advice.

8. Going Without Basic Insurance Protection

Insurance can seem like an expense you are paying for nothing, especially when you rarely use it.

But the point of insurance is to protect you from costs that would be hard to handle on your own. Depending on your situation, this could include health insurance, auto insurance, renters insurance, homeowners insurance, disability insurance, or life insurance.

Why it can hurt

One accident, illness, theft, lawsuit, or major damage claim can create a financial setback that lasts for years. Going without basic protection may save money in the short term, but it can leave your budget exposed to much bigger costs later.

Better move

Review the risks that could seriously hurt your finances. Then look for basic coverage that fits your needs and budget. You do not need every type of insurance, but you should understand what you are choosing to protect and what you are leaving uncovered.

9. Waiting Too Long to Deal With Money Problems

Money problems usually become harder when they are ignored.

A missed bill, growing credit card balance, unpaid loan, overdraft fee, or tax issue may feel stressful to look at. But waiting often limits your options and can make the cost bigger.

Why it can hurt

Delays can lead to late fees, higher interest, damaged credit, collections, service shutoffs, or fewer repayment options. The longer the problem sits, the harder it may be to fix.

Better move

Look at the problem as early as you can, even if you cannot solve it all right away. Contact the lender, bill provider, or company involved and ask what options are available. A payment plan, hardship option, due date change, or smaller first step may be possible before the situation gets worse.

10. Making Big Money Choices Under Pressure

Pressure can make a bad financial decision look urgent.

This can happen when a salesperson says the deal ends today, a friend wants you to join an expensive plan, a family member asks for financial help, or you feel behind compared with people around you.

The problem is that pressure can rush you past the questions you would normally ask.

Why it can hurt

A rushed decision may leave you with payments, contracts, debt, or responsibilities you were not ready for. It can also make it harder to compare better options.

Better move

Give yourself time before making a big money decision. Sleep on it, compare the full cost, read the terms, and ask, “Would I still choose this if there were no pressure?” If the decision is truly right for you, it should still make sense after a pause.

What to Do If You Already Made a Bad Financial Decision

If you already made a financial decision you regret, try not to turn it into a personal failure.

Most people make money choices they would handle differently later. The useful question is not, “Why did I do that?” It is, “What can I do next?”

Start with these steps:

- Look at the full situation. Write down what you owe, what it costs, the due dates, and what happens if you wait.

- Stop the problem from growing. Avoid adding new debt, signing another agreement, or ignoring notices.

- Choose one next step. This could be calling the lender, adjusting your budget, setting up a payment plan, or comparing lower-cost options.

- Ask for help if needed. If the issue involves taxes, legal problems, collections, or debt you cannot manage, consider speaking with a qualified professional. The Federal Trade Commission also shares steps for dealing with debt, including contacting creditors and being careful with debt relief promises.

A bad financial decision does not have to define your future. The sooner you look at it clearly, the sooner you can start building a way forward.

Better Money Decisions Start With a Clear Next Step

Bad financial decisions can be stressful, but they are not always permanent.

The key is to slow down before making choices that can affect your money for a long time. A payment that looks small, a loan that seems easy, or a decision made under pressure can become much harder to manage later.

Before making a bigger money decision, ask:

- What will this cost in total?

- Can I afford the payment and my other priorities?

- What happens if my income drops or expenses rise?

- Am I choosing this because it truly fits my budget, or because I feel rushed?

You do not need to make perfect decisions every time. But giving yourself time to review the numbers can help you avoid choices that create long-term pressure.

One slower, clearer decision today can protect your budget for years.

FAQs About Bad Financial Decisions

What are examples of bad financial decisions?

Examples of bad financial decisions include taking on debt without a payoff plan, buying a car based only on the monthly payment, ignoring high-interest credit card balances, skipping an emergency fund, co-signing a loan without understanding the risk, and making big money choices under pressure.

What is the worst financial decision to avoid?

The worst financial decision depends on your situation, but taking on high-interest debt without a payoff plan is one of the most damaging.

High-interest debt can grow quickly, take money away from other goals, and become harder to manage if you only make minimum payments.

How do you recover from a bad financial decision?

Start by looking at the full situation clearly. Write down what you owe, what it costs, and what options you have.

Then focus on stopping the problem from growing. You may need to adjust your budget, contact a lender, create a repayment plan, compare lower-cost options, or speak with a qualified professional if the issue is serious.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.