Credit card debt can be hard to pay down because the balance does not just sit there. Interest can keep adding up, minimum payments may barely move the total, and new charges can quietly undo the progress you just made.

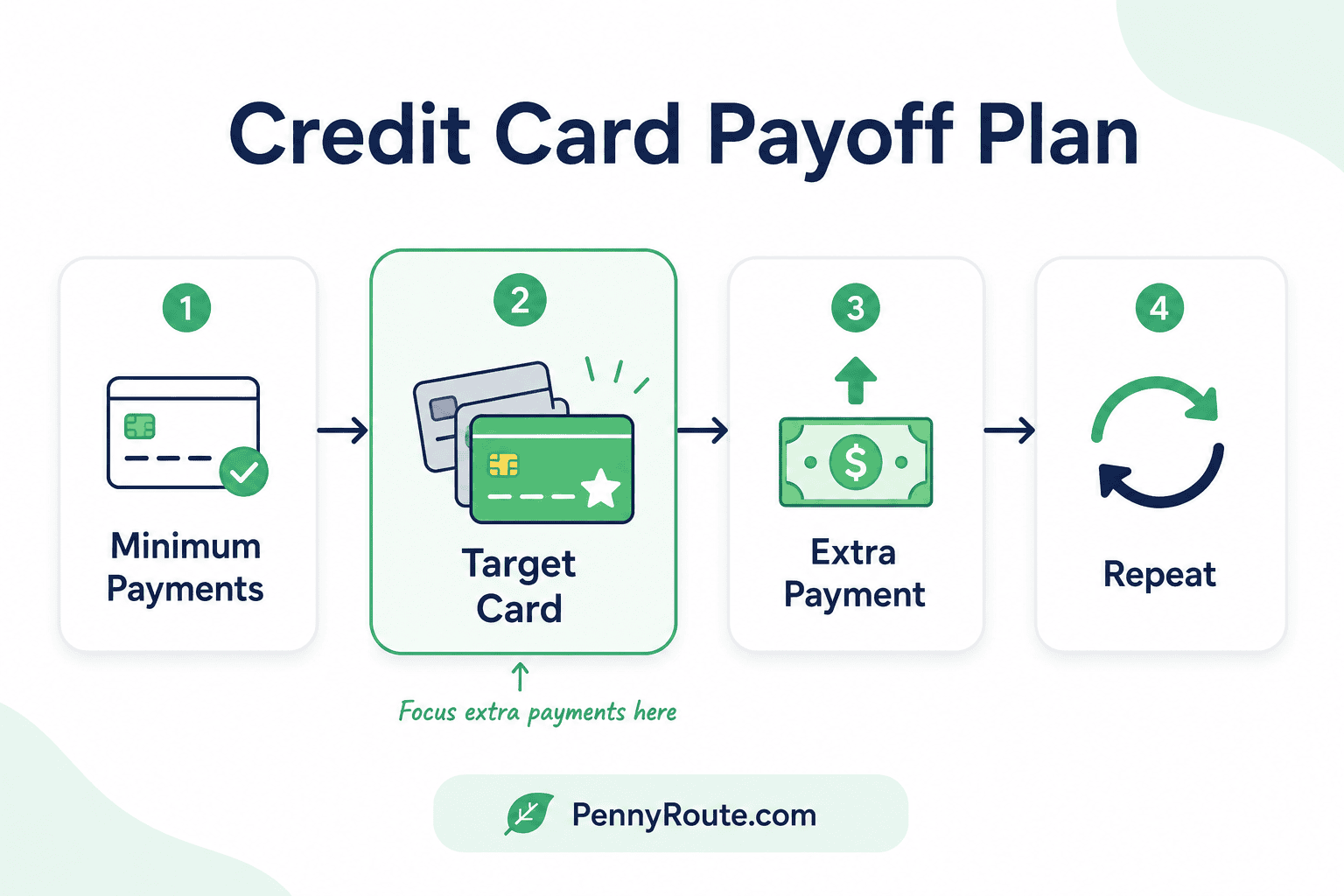

A faster payoff plan starts with making your payments count. That means keeping every card current, stopping new charges where possible, and choosing one target card instead of spreading extra money across every balance.

Before you look at balance transfers, consolidation, or lower-rate options, start with the basics: know what each card costs you, protect your minimum payments, and give your extra money one clear job.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

Quick Overview: How to Pay Off Credit Card Debt Fast

- Stop adding new charges where possible so your payments are not replaced by new spending.

- List each card’s balance, APR, credit limit, minimum payment, and due date.

- Make at least the minimum payment on every card before sending extra money to one target card.

- Choose one target card based on APR, balance size, credit utilization, or past-due status.

- Pay more than the minimum when your budget allows, even if the extra amount starts small.

- Ask your card issuer about lower-rate or payment options if interest is slowing your progress.

- Consider balance transfers or consolidation only if the fees, rates, and payoff timeline make sense.

- Get qualified help if minimum payments no longer fit your income or your cards are falling behind.

Why Credit Card Debt Is Different From Other Debt

Credit card debt can be harder to manage than some other debts because it is revolving debt.

With a car loan or personal loan, you usually borrow a set amount and repay it over a set schedule. With a credit card, the balance can go up and down every month as payments, interest, fees, and new purchases are added.

That makes progress harder to see.

A credit card can also carry a high APR, which means interest may take a large part of your monthly payment if you carry a balance. Paying the minimum can keep the account current, but it may not reduce the balance quickly.

There is another issue: credit cards are easy to reuse. You may make a payment, then use the same card for groceries, gas, or a subscription before the next statement closes. The balance drops, then climbs again.

Credit limits matter too. If one card is close to maxed out, it may create extra pressure on your budget and credit profile. That is why paying off credit card debt is not only about choosing a payoff method. It is also about understanding APR, minimum payments, credit limits, and new charges.

Step 1: Stop New Charges Before You Speed Up Payments

Before you try to pay off credit card debt faster, try to stop the balance from growing.

This does not mean you need to fix every spending habit immediately. It means your payments need a chance to work. If you send $150 to a card but add $140 in new purchases the same week, the balance will barely change.

Start by pausing new charges where you can. Use debit, cash, or a separate checking account for everyday spending if your budget allows. If the card is saved in shopping apps, food delivery apps, or your browser, removing it can add a helpful pause before checkout.

This step matters because credit card payoff is not only about how much you pay. It is also about what happens after the payment posts.

If you still need the card for essentials, do not ignore basic needs. Food, housing, utilities, transportation, insurance, and basic medical needs come first. But if new charges are mostly coming from convenience spending, subscriptions, or small unplanned purchases, stopping those charges can make your payoff progress clearer.

Step 2: List Your Credit Card Balances, APRs, Limits, and Minimum Payments

You cannot choose the best card to pay first until you can see the full picture.

Start by listing each credit card in one place. You can use a notebook, spreadsheet, budgeting app, or a simple notes app. The format does not matter as much as getting the details out of your head and onto the page.

Include these details for each card:

| Card | Balance | Credit Limit | APR | Minimum Payment | Due Date | Status |

|---|---|---|---|---|---|---|

| Card 1 | $2,400 | $3,000 | 27.99% | $75 | 12th | Current |

| Card 2 | $850 | $2,500 | 24.49% | $35 | 18th | Current |

| Card 3 | $4,100 | $4,500 | 29.99% | $140 | 25th | Current |

This table helps you spot what matters most.

If you prefer not to track everything manually, debt payoff apps and calculators can help you organize balances, APRs, minimum payments, and payoff targets in one place.

A card with the highest APR may be costing you the most in interest. A card close to its limit may create extra pressure. A card with a smaller balance may be easier to clear first. A card that is past due may need attention before any payoff method.

Do not skip the due dates. Paying late can add fees and make the situation harder, even if you are trying to make progress.

Once you have the list, you can stop guessing. You will know which cards are most expensive, which are most urgent, and which one should become your first target.

Step 3: Pay the Minimum on Every Card First

Before you send extra money to one card, try to make at least the minimum payment on every card you can.

Minimum payments may not pay down credit card debt quickly, but they help keep each account current. That matters because missing a payment can lead to late fees, penalty APRs, and more stress when you are already trying to catch up.

Think of minimum payments as the protection layer of your payoff plan.

Extra payments are what help you make faster progress, but they should usually come after the required payments are covered. For example, sending an extra $100 to one card may feel productive, but not if it causes you to miss the minimum payment on another card.

Once every card is current, any extra money can go toward one target card. That gives your plan structure without putting another account at risk.

Step 4: Choose One Target Card

Once your minimum payments are covered, choose one card for extra payments.

This matters because spreading extra money across every card can make progress harder to see. If you have $100 extra, sending $20 to five cards may not change much. Sending the full $100 to one target card gives that payment a clearer job.

There are a few ways to choose your first target.

Highest APR First

This means sending extra money to the card with the highest interest rate.

This can be a good choice if your main goal is to reduce interest costs. High-APR cards can keep getting more expensive while you carry the balance, so paying them down first may help more of your future payments go toward the balance instead of interest.

Smallest Balance First

This means sending extra money to the card with the smallest balance.

This can help if you need a quick win. Paying off one small card can remove one monthly payment from your list and make the rest of the plan easier to continue.

Highest Utilization First

This means targeting a card that is close to its credit limit.

For example, a card with a $2,800 balance and a $3,000 limit is almost maxed out. Paying that card down may reduce pressure and give your budget more breathing room.

Past-Due Card First

If one card is already past due, that card may need attention before you focus on interest rates or balance size.

A past-due account can lead to late fees, penalty rates, and more serious account problems. In that case, catching up may be the first priority before choosing a regular payoff method.

There is no single target card that is best for everyone. Choose the card that creates the biggest problem right now: high interest, a small balance you can clear, a nearly maxed-out limit, or a past-due payment.

Step 5: Pay More Than the Minimum When You Can

After the minimum payments are covered, even a small extra amount can help your target card move faster.

You do not need a huge payment to make progress. An extra $20, $50, or $100 can still matter when it goes to the same card consistently. The important part is sending extra money to one target instead of spreading it across every balance.

Look for extra money that will not leave you short before the next paycheck. That might come from:

- Rounding up your card payment

- Sending a small extra payment after payday

- Using part of a refund, bonus, or cash gift

- Moving unused subscription money to the card

- Sending cash-back rewards to the balance

- Using savings from a lower bill or reduced spending

Be careful not to overpay in a way that forces you back to the card. If you send every spare dollar to the balance and then need the card for groceries, the payment may come right back as new debt.

A better approach is to keep essentials covered, protect a small cash buffer if you can, and send extra money to the target card when it truly fits your budget.

Step 6: Ask for a Lower APR or Better Payment Option

If interest is making your credit card debt harder to pay down, it may be worth contacting your card issuer.

You can ask whether a lower APR, temporary payment option, or hardship arrangement is available. There is no guarantee the issuer will say yes, but asking can be useful, especially if your account is current or you have a history of on-time payments.

Before you call, have a few details ready:

- Your current balance

- Your APR

- Your minimum payment

- What you can realistically afford

- Whether the problem is temporary or ongoing

Keep the conversation simple. You might say:

“I’m working on paying down my balance, but the interest is making it difficult. Are there any lower-rate or payment options available on my account?”

If the issuer offers an option, ask questions before agreeing. Find out whether the change is temporary, whether fees apply, whether your account will be restricted, and how it may affect future payments.

A lower rate or adjusted payment can help, but it should fit your budget and support the payoff plan instead of creating confusion later.

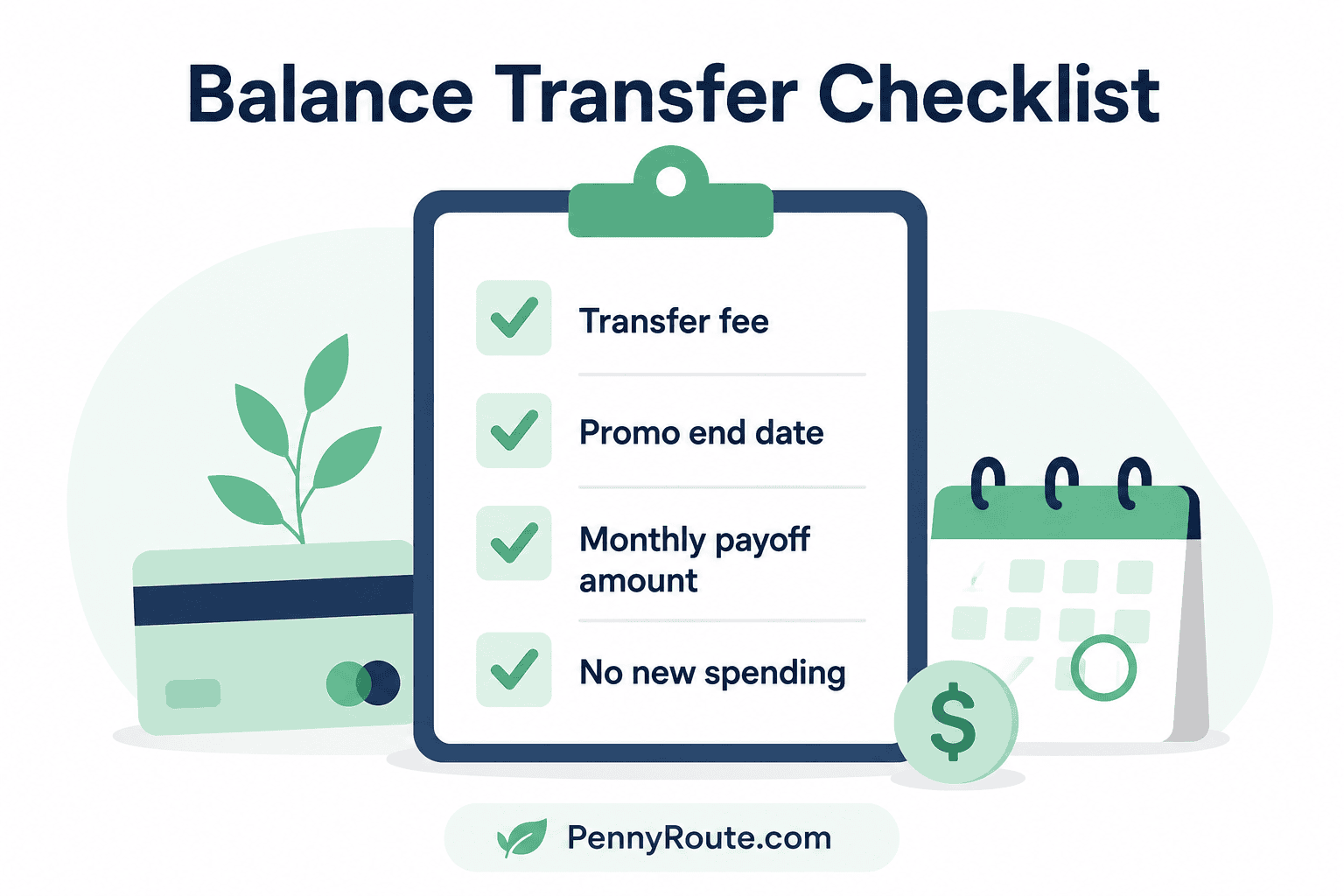

Step 7: Consider a Balance Transfer Only If the Math Works

A balance transfer can help if it lowers your interest rate long enough for you to make real progress.

With a balance transfer, you move credit card debt from one card to another, often with a lower promotional APR. The CFPB explains that a balance transfer moves an outstanding balance from one credit card to another, sometimes with a fee or limited promotional rate.

That can sound helpful, but it is not automatically the right move.

Before using a balance transfer, check:

- The balance transfer fee

- The promotional APR

- How long the promotion lasts

- The regular APR after the promotion ends

- Whether new purchases are included

- The monthly payment needed to pay off the balance before the offer expires

For example, a 3% transfer fee on a $4,000 balance would cost $120. That fee may be worth it if you save much more in interest, but not if the new payment still does not fit your budget.

The biggest risk is treating the transfer like the debt is gone. The debt has only moved. If you transfer a balance and then keep using the old card, you may end up with two balances instead of one.

A balance transfer can be useful, but only when you have a clear payoff plan and the total cost actually works in your favor.

Step 8: Consider Consolidation Only If It Lowers the Real Cost

Debt consolidation can make credit card debt easier to manage, but it should not be used just because the monthly payment looks smaller.

With consolidation, you usually use one new loan or payment plan to pay off several credit card balances. This may give you one payment instead of several, and it may lower your interest rate if you qualify.

The key question is not only:

“Is the payment lower?”

The better question is:

“Will this actually cost less and help me get out of debt?”

Before consolidating credit card debt, check:

- The new interest rate

- Any origination fees or transfer fees

- The repayment term

- The total amount you will pay over time

- Whether the payment fits your budget

- Whether you can avoid using the paid-off cards again

A lower monthly payment can be helpful, but it may cost more overall if the repayment term is much longer. For example, spreading payments over five years may feel easier each month, but you could stay in debt longer if you do not check the total cost.

Consolidation can work when it lowers your real cost, simplifies payments, and comes with a clear plan to avoid rebuilding the card balances. If it only moves the debt around, it may not solve the problem.

Credit Card Debt Payoff Example

A simple example can make the payoff order easier to see.

Let’s say you have three credit cards:

| Card | Balance | Credit Limit | APR | Minimum Payment | Status |

|---|---|---|---|---|---|

| Card A | $3,200 | $4,000 | 27.99% | $105 | Current |

| Card B | $850 | $3,000 | 22.49% | $35 | Current |

| Card C | $4,400 | $4,800 | 29.99% | $145 | Current |

First, you would try to make the minimum payment on all three cards. That keeps each account current.

After that, suppose you have an extra $150 this month.

If your main goal is to reduce interest, Card C may be the best target because it has the highest APR at 29.99%. It is also close to its credit limit, so paying it down may reduce pressure on that account.

If motivation is your biggest challenge, Card B may be a better first target because it has the smallest balance. Paying off one card can make the plan feel more manageable and remove one minimum payment from your monthly list.

The right choice depends on what is creating the biggest problem. High interest, a small balance, a nearly maxed-out card, and a past-due account can all change the priority.

Once you choose a target card, keep sending extra money to that card until it is paid off or until your situation changes. Then move the extra payment to the next card.

What to Avoid While Paying Off Credit Card Debt

Paying off credit card debt is not only about making bigger payments. It is also about avoiding moves that make the balance harder to reduce.

Watch out for these common problems:

- Using one credit card to cover another payment: This can move the pressure around without lowering what you owe.

- Treating a balance transfer like the debt is gone: A transfer can lower interest, but the balance still needs a payoff plan.

- Consolidating without checking the total cost: A lower monthly payment may cost more over time if the repayment term is much longer.

- Using paid-off cards again: If an old balance is replaced with new purchases, the progress can disappear quickly.

- Ignoring a card that is close to its limit: A nearly maxed-out card can create extra pressure and may need attention even if another card has a smaller balance.

- Missing due dates while trying to pay extra: Minimum payments still matter, even when you are focused on one target card.

- Assuming rewards are worth carrying a balance: Cash back or points usually do not make up for high credit card interest.

A good payoff plan should lower the balance, not just move it to a different place. Before you use a new tool or strategy, ask whether it actually reduces the cost, simplifies the plan, and helps you avoid adding new debt.

When to Get Help

Sometimes credit card debt becomes too difficult to manage with small budget changes alone.

It may be time to get help if:

- You cannot afford the minimum payments

- You are using credit cards for basic needs every month

- Several cards are past due

- Interest and fees are growing faster than your payments

- You are considering debt settlement

- You are getting calls or letters about unpaid accounts

- You are not sure which payment to make first

In these situations, guessing can make things harder. The FTC notes that a credit counselor may review your financial situation and help with a plan for managing unsecured debts like credit cards.

Be careful with any company that promises to erase debt quickly or asks for large upfront fees. Credit card debt can be stressful, but quick-fix promises are not always safe.

Getting help does not mean you failed. It means the payment plan may need more support than your current budget can give.

Make Your Next Credit Card Payment Count

Paying off credit card debt starts with one clear target.

Once your minimum payments are covered, choose the card that needs your attention most and send extra money there when your budget allows. That might be the card with the highest interest rate, the smallest balance, a high utilization, or a payment that needs to be caught up.

The plan does not have to be perfect right away. What matters most is that new charges slow down, payments stay current, and each extra dollar has a clear place to go.

FAQs About Paying Off Credit Card Debt

What is the fastest way to pay off credit card debt?

The fastest practical way is to stop adding new charges, make minimum payments on every card, and send extra money to one target card. If interest is the biggest problem, start with the card that has the highest APR.

Should I pay off the smallest credit card or the highest-interest card first?

Paying the highest-interest card first may help reduce interest costs. Paying the smallest balance first may help you stay motivated by clearing one card sooner.

Is it bad to only make the minimum payment on a credit card?

Making the minimum payment is better than missing a payment, but it usually will not pay down the balance quickly. Interest can keep adding up, so paying more than the minimum can help when your budget allows.

Can I ask my credit card company to lower my interest rate?

Yes, you can ask your card issuer whether a lower APR or payment option is available. Approval is not guaranteed, but it may be worth asking if you are trying to pay down the balance.

Is a balance transfer a good way to pay off credit card debt?

A balance transfer can help if the lower promotional rate saves more than the transfer fee and you have a plan to pay the balance before the promotion ends. It can backfire if you keep using the old card and build a new balance.

What should I do if I cannot make my credit card payments?

Start by reviewing your income, basic expenses, and minimum payments. Contact your card issuer before missing a payment and consider nonprofit credit counseling or qualified help if the payments no longer fit your budget.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.