Paying off debt gets confusing when every balance is competing for attention. One card has a small balance. Another has a higher payment. A loan is sitting in the background. And even after making payments, the list may not look much shorter.

The debt snowball method gives that chaos a simple order: start with the smallest debt, clear it first, then roll that payment into the next one.

It is not the most math-perfect payoff method, but it can make progress easier to see. When one balance disappears, the whole plan starts to look more manageable.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

What Is the Debt Snowball Method?

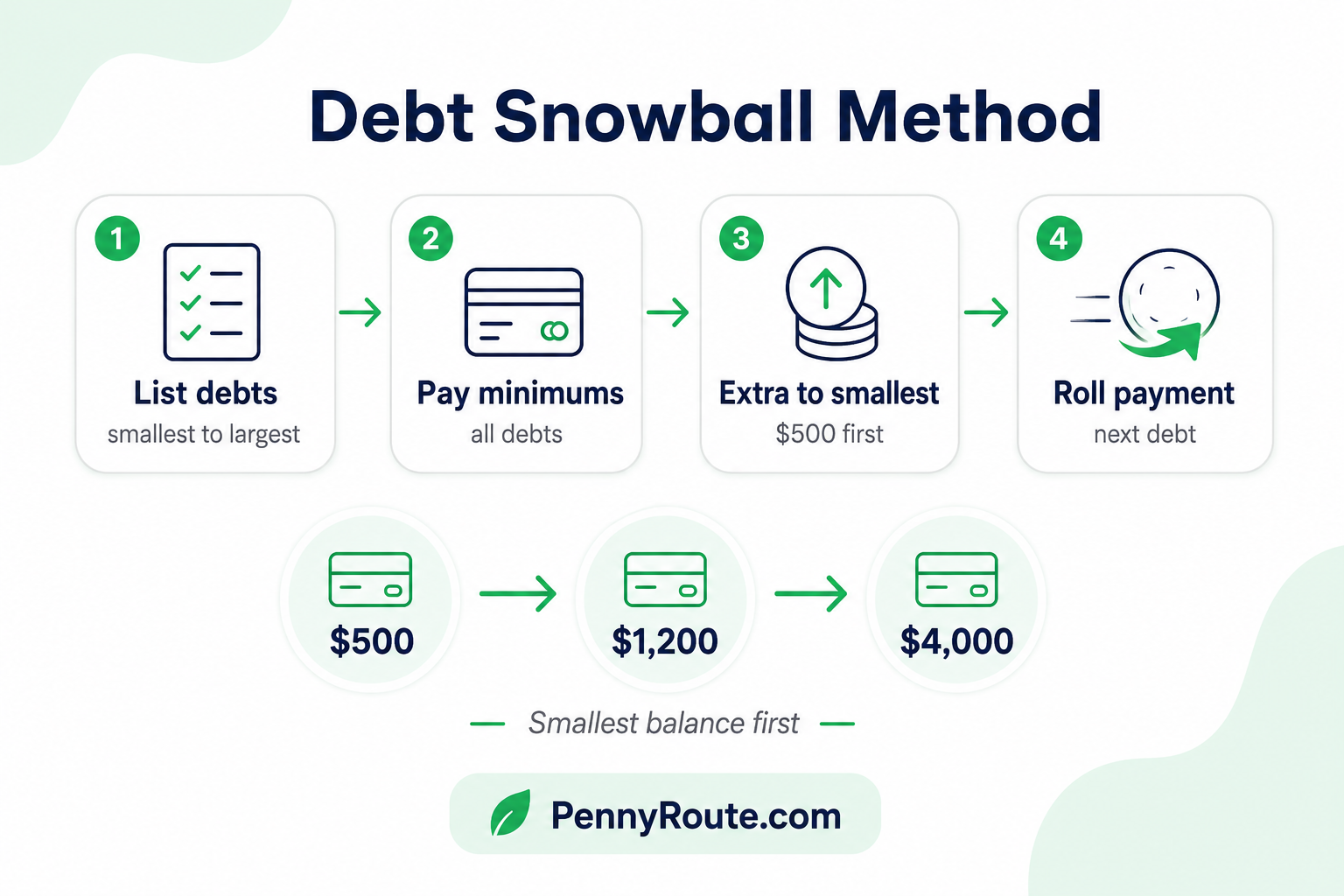

The debt snowball method is a debt payoff strategy where you make the minimum payment on every debt, then put extra money toward the smallest balance first.

Once the smallest debt is paid off, you roll that old payment into the next-smallest debt. As each balance disappears, the amount you can put toward the next one grows.

Here is the basic idea:

- List your debts from smallest balance to largest balance.

- Make minimum payments on every debt.

- Put extra money toward the smallest debt first.

- After that debt is paid off, move its payment to the next-smallest debt.

- Repeat until your debts are paid off.

The main reason people use the debt snowball method is momentum. Paying off a small balance early can make the whole debt payoff process easier to stick with.

How the Debt Snowball Method Works

The debt snowball method works by giving your extra payments one clear job at a time.

Instead of spreading extra money across every debt, you focus on the smallest balance first. The goal is to remove one debt from your list, then use that freed-up payment to move faster on the next one.

Here is the step-by-step process:

- List every debt you owe. Include the balance, minimum payment, and due date.

- Sort the debts from smallest balance to largest balance. Ignore interest rates for now.

- Make the minimum payment on every debt. This helps keep your accounts current.

- Put any extra money toward the smallest debt. Even a small extra amount counts.

- Pay off the smallest debt completely.

- Roll that payment into the next-smallest debt. Keep paying the minimums on everything else.

- Repeat the process until each debt is gone.

For example, if your smallest debt has a $25 minimum payment and you were adding $50 extra, that gives you $75 to roll into the next debt once the first one is paid off.

That is how the “snowball” builds. Each paid-off balance gives you more money to put toward the next target.

Debt Snowball Method Example

Let’s say you have four debts:

| Debt | Balance | Minimum Payment |

|---|---|---|

| Store card | $450 | $25 |

| Medical bill | $800 | $40 |

| Credit card | $2,400 | $75 |

| Personal loan | $5,000 | $180 |

With the debt snowball method, you would focus on the store card first because it has the smallest balance.

You would still make the minimum payments on the medical bill, credit card, and personal loan. Then, any extra money would go toward the store card until it is paid off.

For example, if you can put an extra $75 toward debt each month, your store card payment would look like this:

| Store Card Payment | Amount |

|---|---|

| Minimum payment | $25 |

| Extra payment | $75 |

| Total payment | $100 |

Once the store card is paid off, you do not stop using that $100. You roll it into the next debt.

That means the medical bill payment could become:

| Medical Bill Payment | Amount |

|---|---|

| Original minimum payment | $40 |

| Rolled-over store card payment | $100 |

| New total payment | $140 |

That is the snowball effect. Each paid-off debt gives your next payment more weight without needing to restart your plan from zero.

Why the Debt Snowball Method Can Work

The debt snowball method can work because debt payoff is not only a math problem. It is also a behavior problem.

When you have several debts, progress can look slow at first. You may be making payments every month, but if every balance only drops a little, it can be hard to stay encouraged.

The snowball method changes that by giving you one small target to clear first.

Paying off a small debt gives you visible proof that your plan is working. One balance disappears. One monthly payment is gone. Your debt list gets shorter.

That early win can make the next step easier to repeat. Instead of starting each month with the same long list of balances, you have one less debt to manage and a little more money to roll forward.

The debt snowball method is not perfect for every situation, but it gives many people something they need early: a clear first win.

Pros of the Debt Snowball Method

The debt snowball method is popular because it is simple and easy to follow.

You do not need a complicated spreadsheet or advanced math to get started. You list your debts by balance, choose the smallest one, and focus your extra payment there first.

Here are the main benefits:

- It gives you a clear starting point. You do not have to debate which debt to attack first. The smallest balance becomes your first target.

- It can create quick wins. Paying off a small debt early can make the payoff process more encouraging.

- It reduces the number of debts faster. Even if your total debt is still high, having fewer accounts to manage can make your monthly plan simpler.

- It helps you stay focused. Instead of spreading extra money across several debts, you give one balance your full attention.

- It works with small extra payments. You do not need hundreds of dollars extra each month to start. Even $20 or $50 can help when it goes toward one target debt.

- It builds payment momentum. Once one debt is paid off, that old payment rolls into the next one, helping your payoff amount grow over time.

The biggest strength of the debt snowball method is simplicity. It gives your extra payment one clear job.

Cons of the Debt Snowball Method

The debt snowball method is helpful, but it is not perfect for every situation.

The biggest downside is that it does not focus on interest rates. If your smallest debt has a low interest rate and your largest debt has a high interest rate, the snowball method may leave the expensive debt sitting longer.

That can cost more over time.

For example, if you have a $500 medical bill at 0% interest and a $3,000 credit card balance at 27.99% APR, the debt snowball method would focus on the medical bill first. That may give you a quick win, but the credit card is still adding interest in the background.

Other downsides include:

- You may pay more interest overall. This can happen if high-interest debts are not paid until later.

- It may not be the fastest option mathematically. The debt avalanche method often wins if the goal is to reduce interest costs.

- It can hide expensive debt for too long. A large high-interest credit card balance may need attention sooner.

- It still requires consistency. The method only works if you keep making minimum payments and roll payments forward.

- It does not fix new spending by itself. If new balances keep growing, the snowball may not move much.

The debt snowball method is best when motivation and simplicity matter most. If interest costs are your biggest concern, compare it with the debt avalanche method before choosing.

Debt Snowball vs Debt Avalanche: What’s the Difference?

The debt snowball method and debt avalanche method both help you focus on one debt at a time.

The difference is how you choose the first debt.

| Method | First Target | Best For |

|---|---|---|

| Debt snowball | Smallest balance | Motivation and quick wins |

| Debt avalanche | Highest interest rate | Saving more on interest |

With the debt snowball method, you start with the smallest balance, even if another debt has a higher interest rate.

With the debt avalanche method, you start with the highest-interest debt, even if another balance is smaller.

For a deeper side-by-side breakdown, read this guide on debt snowball vs debt avalanche.

Who Should Use the Debt Snowball Method?

The debt snowball method may be a good fit if you need a simple payoff plan that helps you stay focused.

It is especially useful when you have several balances and want to reduce the number of debts on your list as quickly as possible.

Consider using the debt snowball method if:

- You have multiple debts to manage

- You have several small balances

- You want quick wins to stay encouraged

- You prefer simple steps over interest calculations

- You have started debt payoff plans before but stopped

- You want to make your monthly payments easier to track

- You need a payoff method that works with small extra payments

The debt snowball method is not about choosing the cheapest route every time. It is about choosing a route that helps you keep moving.

When the Debt Snowball Method May Not Be Best

The debt snowball method is simple, but it is not the right fit for every debt situation.

It may not be the best choice if one of your debts has a very high interest rate. In that case, ignoring the APR could cost you more over time.

For example, if your smallest debt is a $300 medical bill at 0% interest, but you also have a $4,000 credit card at 28.99% APR, the credit card may deserve attention sooner.

The debt snowball method may not be ideal if:

- Your highest-interest debt is growing quickly

- You want to save the most money on interest

- You are comfortable using a more math-based payoff plan

- You cannot afford the minimum payments on all debts

- You are still adding new balances every month

- Your debt situation includes collections, lawsuits, or urgent financial hardship

In those cases, the debt avalanche method, credit counseling, or another option may be worth exploring.

The debt snowball method can be useful, but it should not be followed blindly. If one debt is clearly causing the biggest financial damage, it may need to move higher on your list.

Tips to Make the Debt Snowball Method Work Better

The debt snowball method is simple, but a few small habits can make it much easier to follow.

Start with these:

- Automate your minimum payments. This helps you avoid late fees while you focus extra money on your smallest debt.

- Choose a realistic extra payment. Do not make the plan so tight that one grocery run ruins it. Even a small extra amount can help when you repeat it.

- Keep your target debt visible. Write the balance on a tracker, spreadsheet, or notes app so you can watch it go down.

- Use extra money before it disappears. Refunds, cash-back rewards, bonuses, or leftover weekly money can go straight to your target debt.

- Stop adding new balances. The snowball method works better when your debts are shrinking, not growing in the background.

- Roll payments forward every time. When one debt is paid off, move that old payment to the next debt instead of letting it blend back into everyday spending.

- Celebrate progress without creating new debt. A small win is worth noticing, but try not to reward yourself with spending that slows the plan down.

The goal is to make the method easy to repeat. Once the first balance is gone, the next payment gets stronger, and the plan starts to build on itself.

Common Mistakes to Avoid With the Debt Snowball Method

The debt snowball method is simple, but a few mistakes can slow your progress.

Watch out for these:

- Skipping minimum payments: Extra payments should only go to your smallest debt after the minimum payments on your other debts are covered.

- Splitting extra money across every debt: Sending a little extra to every balance may seem helpful, but focusing on one target debt usually makes progress clearer.

- Not rolling payments forward: When one debt is paid off, move that payment to the next-smallest debt instead of letting it blend back into regular spending.

- Adding new balances while paying old ones: The snowball works best when your debts are shrinking, not growing in the background.

- Ignoring very high-interest debt completely: The snowball method focuses on balance size, but a very expensive high-interest debt may deserve extra attention.

A good debt snowball plan needs focus. Pick the smallest debt, pay it off, then keep the payment moving.

What If You Can’t Find Extra Money?

The debt snowball method works faster when you can put extra money toward your smallest debt. But that does not mean you need a huge amount to start.

Begin with whatever is realistic.

Even $10 or $25 extra can help build the habit of focused payments. The point is to send that extra money to one target debt instead of letting it disappear into everyday spending.

A few ways to find small amounts include:

- Canceling one unused subscription

- Using cash-back rewards as a debt payment

- Selling one or two items you no longer use

- Sending leftover grocery or gas money to your target debt

- Pausing one non-essential spending category for 30 days

- Using refunds, bonuses, or gift money toward your smallest balance

If there is no extra money at all, start by staying current where you can. Make minimum payments, avoid new debt when possible, and look for one small budget change at a time.

If minimum payments no longer fit your income, the issue may be bigger than a payoff method. In that case, consider speaking with a nonprofit credit counselor or another qualified professional before the situation becomes harder to manage.

Start Small, Then Let the Payments Build

The debt snowball method works because it gives your payoff plan a clear first step.

You do not have to solve every balance at once. Start with the smallest debt, keep making minimum payments on the rest, and send any extra money to that first target.

Once the smallest debt is gone, roll that payment into the next one. Then repeat the process.

The method may not save the most interest, but it can make debt payoff simpler and more encouraging. For many people, that matters.

If your debt list looks overwhelming, start with the smallest balance. One paid-off debt can turn a messy plan into a plan that finally has direction.

FAQs About the Debt Snowball Method

What is the debt snowball method in simple terms?

The debt snowball method is a debt payoff strategy where you pay the smallest balance first while making minimum payments on all other debts.

Once the smallest debt is paid off, you roll that payment into the next-smallest debt and repeat the process.

Does the debt snowball method really work?

Yes, the debt snowball method can work if you make minimum payments on every debt, focus extra money on one balance, and keep rolling payments forward.

Its main strength is early progress. Paying off a small debt can make the plan easier to continue.

What debt do you pay first with the snowball method?

With the debt snowball method, you pay the debt with the smallest balance first. Interest rates do not decide the first target. The goal is to clear one balance quickly and build momentum.

Is the debt snowball method better than avalanche?

The debt snowball method may be better if quick wins help you stay motivated.

The debt avalanche method may be better if your main goal is to save the most money on interest. Both can work, but they focus on different priorities.

Can I use the debt snowball method for credit card debt?

Yes, you can use the debt snowball method for credit card debt.

List your credit card balances from smallest to largest, make minimum payments on all cards, and put extra money toward the card with the smallest balance first.

What is the biggest downside of the debt snowball method?

The biggest downside is that the debt snowball method does not focus on interest rates.

That means you may pay more interest over time if a larger high-interest debt waits too long.

How much extra money do I need to start a debt snowball?

You can start with any extra amount that fits your budget. Even $10, $25, or $50 can help when it goes toward one target debt consistently.

What should I do after paying off the first debt?

After paying off the first debt, roll that payment into the next-smallest debt.

Do not let the old payment disappear into regular spending. That is how the snowball gets bigger.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.