It is easy to overspend when all your money sits in one place.

You check your account balance, see money available, and think, “Okay, I can spend a little.” But that same money may also need to cover groceries, gas, a birthday gift, and the bill that shows up next week with suspicious timing.

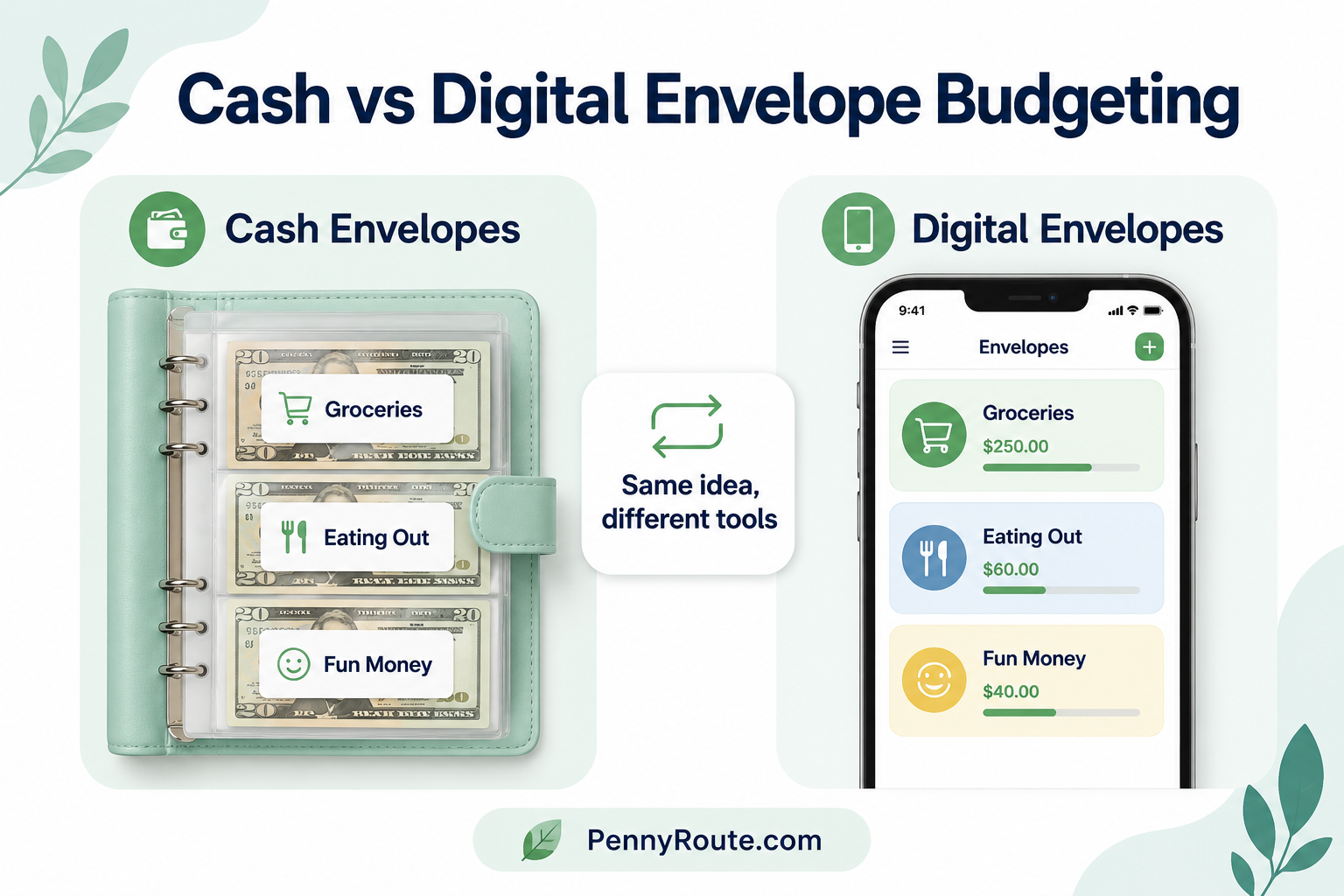

The envelope budgeting method helps fix that by separating your spending money into clear categories before you spend it.

Instead of treating your full account balance like one big pile of money, you give each category its own limit. Groceries get one envelope. Eating out gets another. Fun money gets another. Once an envelope is empty, that category is done until the next budget period.

You can use physical cash envelopes, digital envelopes, or a mix of both. The point is not the envelope itself. The point is knowing exactly how much you have left for each type of spending.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

What Is the Envelope Budgeting Method?

The envelope budgeting method is a system where you divide your spending money into separate categories, then give each category a set limit.

Traditionally, people used physical envelopes with cash inside. One envelope might be for groceries, another for eating out, another for gas, and another for personal spending.

For example:

| Envelope | Monthly Limit |

|---|---|

| Groceries | $450 |

| Eating out | $150 |

| Gas or transport | $200 |

| Personal spending | $100 |

Once the money in an envelope is gone, spending in that category stops unless you intentionally move money from another category.

Envelope budgeting is also often called cash stuffing when you use physical cash envelopes, binders, or pouches to organize your spending money.

But you do not have to use cash. You can also use separate bank accounts, budgeting apps, prepaid cards, or digital categories. The method is really about one simple idea:

Give your spending limits a place to live before the money disappears.

Why Envelope Budgeting Works

Envelope budgeting works because it makes your spending limits easier to see.

When all your money sits in one account, it can be hard to know what is actually available. Your balance might look healthy, but part of that money may already be needed for groceries, gas, bills, or next week’s plans.

Envelopes separate the money before you spend it.

That helps in a few ways:

- It gives each category a clear limit. You know exactly how much is available for groceries, eating out, shopping, or fun money.

- It makes overspending easier to notice. If your eating out envelope is almost empty halfway through the month, you can slow down before the category causes bigger problems.

- It reduces guesswork. Instead of asking, “Can I afford this?” you check the envelope for that category.

- It helps protect other money. Grocery money does not accidentally become shopping money unless you choose to move it.

This method is especially useful for flexible spending categories. Fixed bills like rent, insurance, and loan payments are usually easier to automate. Envelopes are most helpful for the areas where spending can quietly stretch.

Cash Envelopes, Digital Envelopes, or Both?

Envelope budgeting does not have to mean carrying cash for everything.

The old-school version uses physical envelopes with cash inside. That can work well because the limit is visible. When the cash is gone, the category is done.

But if you mostly use debit cards, online shopping, or automatic payments, digital envelopes may be easier. You can create category limits in a budgeting app, use separate bank accounts, or set up “spaces” or “pots” if your bank offers them.

A hybrid system can also work. For example, you might use cash for groceries and eating out, then keep bills and savings digital.

| Envelope Type | How It Works | Best For |

|---|---|---|

| Cash envelopes | Put physical cash into labeled envelopes | Visual spenders who need firm limits |

| Digital envelopes | Use apps, bank accounts, or category trackers | People who mostly use cards or online payments |

| Hybrid system | Use cash for problem categories and digital tools for the rest | People who want structure without going cash-only |

The best version is the one you will actually use.

If cash helps you slow down, use cash. If cash feels inconvenient or unsafe, use digital envelopes instead. The method should make spending clearer, not turn every errand into a banking field trip.

Envelope Budgeting Example

Let’s say you want to use envelope budgeting for the categories where your spending changes the most.

Your rent, insurance, loan payments, and subscriptions may already be fixed or automated. So instead of making envelopes for everything, you focus on flexible spending.

Here’s a simple monthly example:

| Envelope | Monthly Limit |

|---|---|

| Groceries | $450 |

| Eating out | $150 |

| Gas or transport | $200 |

| Personal spending | $100 |

| Entertainment | $100 |

| Gifts and miscellaneous | $75 |

| Total envelope spending | $1,075 |

In this example, you are not trying to manage your entire financial life with envelopes. You are using them for the areas where spending can change quickly.

If the eating out envelope has $40 left, that tells you what you can spend on restaurants or takeout for the rest of the month. If the grocery envelope is running low, you may plan simpler meals before the next refill.

That is the main value of envelope budgeting. It turns vague spending into clear limits.

Which Categories Should Get Envelopes?

Envelope budgeting works best for spending categories that change from week to week or month to month.

You usually do not need an envelope for every bill. Rent, insurance, loan payments, and subscriptions can often stay automated, especially if the amounts are predictable.

Start with the categories where money tends to disappear fastest.

Good envelope categories include:

- Groceries: helpful if food spending keeps creeping up

- Eating out: restaurants, takeaway, coffee shops, and snacks

- Gas or transport: fuel, public transport, rideshares, parking

- Personal spending: clothes, beauty, small treats, hobbies

- Entertainment: movies, events, games, activities

- Household items: cleaning supplies, toiletries, home basics

- Gifts: birthdays, holidays, small celebrations

- Kids’ activities: school extras, activities, weekend plans

- Miscellaneous: small surprises that do not fit neatly elsewhere

A good starting point is 3 to 5 envelopes. That is enough to create structure without making your budget feel like a part-time admin job.

Once those categories feel manageable, you can add more if needed.

Before You Fill Envelopes, Cover Your Fixed Bills First

Before you put money into envelopes, make sure your fixed bills and required payments are covered.

Envelope budgeting works best for flexible spending, but your rent, utilities, insurance, minimum debt payments, and other must-pay bills still need a clear plan.

A simple order can look like this:

- Set aside money for fixed bills.

- Set aside money for savings or debt goals.

- Fill envelopes for flexible spending categories.

- Keep a small buffer if possible.

This helps prevent a common problem: having cash ready for groceries or fun money, but not enough left for a bill that arrives later.

You do not need envelopes for every fixed bill unless that helps you. For many people, autopay or a separate bills account works better for predictable expenses. Then envelopes can handle the categories that tend to change, such as groceries, eating out, shopping, and entertainment.

How to Start Envelope Budgeting Without Overcomplicating It

Envelope budgeting works best when you start small.

You do not need fifteen envelopes, color-coded labels, and a full Sunday afternoon budget ceremony. Start with the spending areas that need the most attention, then build from there.

Here’s a simple way to begin:

- Look at your take-home pay. Start with the money that actually reaches your bank account after taxes and deductions.

- Set aside fixed bills first. Rent, utilities, insurance, minimum debt payments, and subscriptions should be covered before you fill spending envelopes.

- Choose 3 to 5 envelope categories. Pick the areas where overspending happens most often, such as groceries, eating out, shopping, entertainment, or personal spending.

- Set realistic limits. Use last month’s spending as a guide. If you spent $600 on groceries last month, setting the envelope at $250 may sound responsible, but it probably will not survive contact with real life.

- Fill your envelopes after payday. Add cash to physical envelopes or update your digital categories when income arrives.

- Check the envelope before spending. Before buying from that category, look at what is left. That small pause is where the method starts working.

- Review what ran out first. At the end of the week or month, notice which envelopes emptied quickly. That tells you where to adjust.

The first month is mostly about learning your real numbers. Once you know where the pressure points are, you can make better limits next time.

What to Do When an Envelope Runs Out

When an envelope runs out, pause before spending more from that category.

That does not mean your budget failed. It usually means one of two things: the limit was too low, or the category needs more attention next month.

Stop Spending If It Is Optional

If the envelope is for entertainment, shopping, takeout, or personal spending, the simplest option is to stop spending in that category until the next refill.

For example, if your eating out envelope is empty, you might cook at home for the rest of the week instead of using a credit card to “borrow from next month.”

This is where envelope budgeting does its job. It creates a clear stopping point before overspending becomes automatic.

Move Money Only on Purpose

Sometimes, moving money between envelopes makes sense.

If your grocery envelope runs out but your entertainment envelope still has money, you might move $40 from entertainment to groceries. That is not cheating. That is adjusting your budget based on real life.

The key is to make the move intentionally. Do not keep pulling from other envelopes every time one category runs out, or the limits stop meaning anything.

Adjust the Limit Next Month

If the same envelope runs out every month, the limit may be unrealistic.

For example, if you keep setting groceries at $350 but usually spend closer to $450, your budget may need a higher grocery limit. You can then reduce another category or adjust your overall spending plan.

A good envelope budget should challenge overspending, but it should still be possible to live with.

Use a Small Buffer Envelope

A small buffer envelope can help with expenses that do not fit neatly anywhere else.

This could cover things like a last-minute school item, extra household supplies, or a small price increase you did not expect.

The buffer does not need to be large. Even $25 to $50 can reduce the need to constantly reshuffle money between categories.

Avoid Using Credit Cards to Bypass the Limit

If an envelope is empty and you use a credit card anyway, the system loses its main benefit.

That does not mean credit cards are always bad. But if the card becomes a way to ignore the envelope limit, it can quietly undo the budget.

If you use credit cards for rewards or convenience, track the purchase against the right envelope immediately. The envelope should still decide whether the spending fits.

Envelope Budgeting Pros and Cons

Envelope budgeting can be very effective, especially if you need clear spending limits. But like any budgeting method, it has strengths and limits.

| Pros | Cons |

|---|---|

| Helps control overspending | Can feel restrictive if limits are too tight |

| Makes spending limits easy to see | Physical cash can be inconvenient |

| Works well for flexible categories | Too many envelopes can feel overwhelming |

| Helps protect money for each purpose | Requires regular check-ins |

| Can be done with cash or digital tools | May not work well for every bill or expense |

The biggest benefit is awareness. You know how much is left for each category before you spend.

The biggest challenge is maintenance. You need to refill envelopes, check balances, and adjust categories when real life changes.

Envelope budgeting works best when the system is simple enough to keep using. Start with a few categories, review them often, and adjust the limits when needed.

Who Envelope Budgeting Works Best For

Envelope budgeting works best for people who need clear limits around flexible spending.

It can be especially helpful if you do not have a problem paying fixed bills, but you do struggle with categories like groceries, eating out, shopping, hobbies, or weekend spending.

Envelope budgeting may work well if you:

- Overspend in a few specific categories

- Want a visual way to manage money

- Like clear spending limits

- Use cash for some purchases

- Want to reduce impulse spending

- Need a simple system for groceries, takeout, or fun money

- Feel like your bank balance makes spending look easier than it really is

Envelope budgeting may not be ideal if you:

- Want a fully automated budget

- Dislike tracking categories

- Use online payments for almost everything

- Feel stressed by strict spending limits

- Have income that changes a lot and needs more flexibility

- Prefer a broad method like the 50/30/20 budget

You do not have to use envelopes for your whole budget. For many people, envelope budgeting works best as a targeted tool.

For example, you might use envelopes only for groceries, eating out, and personal spending while keeping bills, savings, and debt payments automated. That gives you control where you need it without making the whole system harder than necessary.

Envelope Budgeting vs. Zero-Based Budgeting

Envelope budgeting and zero-based budgeting are sometimes confused because both methods give your money a job. The difference is how detailed the system is.

Envelope budgeting focuses mainly on spending limits by category. Zero-based budgeting focuses on planning every dollar of income before the month begins.

| Envelope Budgeting | Zero-Based Budgeting |

|---|---|

| Separates money into category limits | Assigns every dollar a specific job |

| Best for controlling flexible spending | Best for full budget planning |

| Often used for groceries, eating out, shopping, and fun money | Used for bills, savings, debt, spending, and buffers |

| Can be done with cash or digital envelopes | Usually done with a spreadsheet, app, or written budget |

| Helps stop overspending in problem areas | Helps organize the entire monthly budget |

The two methods can also work together.

For example, you could use zero-based budgeting to plan your full monthly income, then use envelopes for the categories where you need extra control. Groceries, takeout, entertainment, and personal spending are good places to start.

Think of zero-based budgeting as the full plan, and envelope budgeting as the guardrail for the categories that tend to wander off.

Make Your Envelopes Easy to Stick With

Envelope budgeting works best when it feels simple enough to repeat.

You do not need a perfect binder, matching labels, or an envelope for every possible expense. Start with the categories that actually need help. For most people, that means groceries, eating out, personal spending, entertainment, or shopping.

Keep your fixed bills separate if they are already working well on autopay. Let envelopes handle the spending areas that tend to stretch.

After the first month, review what happened. Which envelope ran out first? Which one had money left? Which limit felt too tight or too loose?

That quick review can tell you more than a perfect-looking budget ever could.

The envelope budgeting method is not about making spending harder. It is about making your limits clearer, so your money goes where you meant it to go.

FAQs About Envelope Budgeting

Is envelope budgeting the same as cash stuffing?

Envelope budgeting and cash stuffing are closely related.

Envelope budgeting is the overall method of dividing money into spending categories. Cash stuffing is the physical version, where you put cash into labeled envelopes, binders, or pouches.

Does envelope budgeting have to use cash?

No, envelope budgeting does not have to use cash.

You can use budgeting apps, separate bank accounts, bank “spaces,” prepaid cards, or a spreadsheet. The main idea is to separate money by category before spending it.

What categories should I use for envelope budgeting?

Start with categories where your spending changes often or gets hard to control.

Good beginner envelope categories include groceries, eating out, gas or transport, personal spending, entertainment, shopping, household items, and gifts.

What happens if an envelope runs out?

If an envelope runs out, pause spending in that category unless it is necessary.

You can stop spending, move money from another envelope intentionally, or adjust the limit next month if the amount was unrealistic. Avoid using credit cards to ignore the limit.

Is envelope budgeting good for beginners?

Yes, envelope budgeting can be helpful for beginners because it makes spending limits clear.

It works especially well if you overspend in a few specific areas, such as groceries, takeout, shopping, or entertainment.

Can I use envelope budgeting with a debit card?

Yes, you can use envelope budgeting with a debit card.

The key is to track each debit card purchase against the right envelope or category. For example, if you spend $40 on groceries, subtract $40 from your grocery envelope.

Is envelope budgeting better than zero-based budgeting?

Envelope budgeting is better if your main problem is overspending in certain categories.

Zero-based budgeting is better if you want to plan your entire income in detail. You can also combine both by using zero-based budgeting for your full monthly plan and envelopes for flexible spending categories.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.