Keeping all your money in one account can seem simple at first. But when bills and everyday spending come from the same place, it’s not always clear what you can safely use.

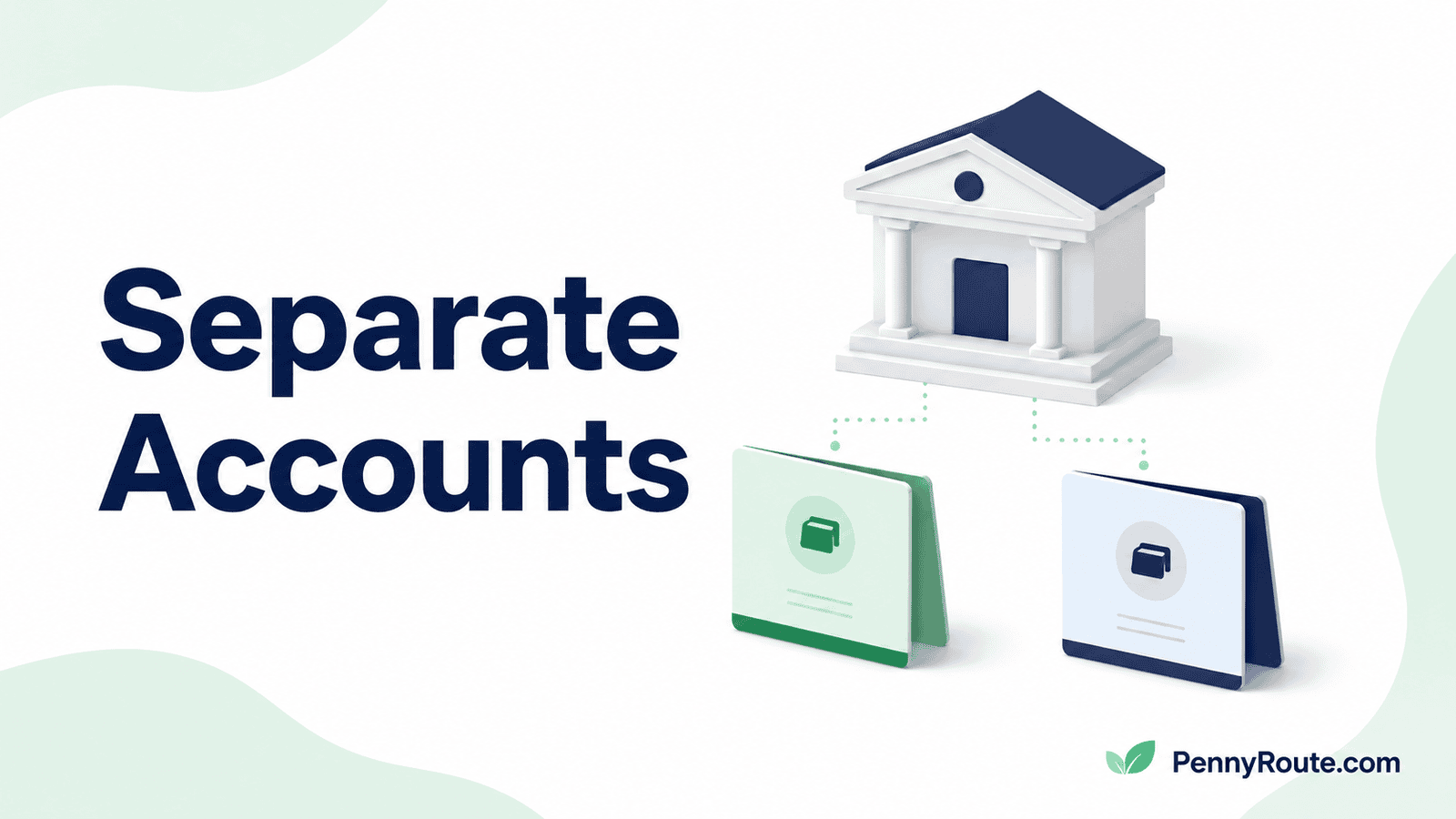

That’s where the idea of having separate bank accounts comes in. Instead of tracking everything mentally, you give your money a clear structure.

For many people, using one account for bills and another for spending makes daily decisions easier. It’s not about adding complexity. It’s about making your money easier to understand and manage.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

Should You Separate Your Bank Accounts for Bills and Spending?

Separating your bank accounts for bills and spending can make managing your money easier, but it’s not something you have to do.

Using one account for bills and another for everyday spending helps you see clearly what’s already committed and what’s available. This can reduce the chances of using money meant for rent, utilities, or other fixed expenses.

At the same time, some people prefer keeping everything in one place and tracking it with a simple plan.

Separating your accounts can help when you want clearer boundaries between bills and everyday spending.

What It Means to Separate Bills and Spending

Separating your accounts means using one account for fixed expenses and another for everyday use.

Your bills account holds money for rent, utilities, subscriptions, and other regular payments. This amount is set aside so you don’t accidentally spend it.

Your spending account is for daily expenses like groceries, transport, and small purchases. This is the balance you rely on for day-to-day decisions.

This setup creates a clear boundary. Instead of trying to remember what part of your balance is already committed, your accounts show it for you.

Why This Approach Works for Many People

Separating bills and spending works because it reduces the number of decisions you have to make during the month.

When your bills are already set aside, you don’t have to keep checking if you can afford something. Your spending account shows what’s available, so daily choices feel more straightforward.

It also helps prevent accidental overspending. If your rent and utilities are in a separate account, you’re less likely to use that money by mistake.

Another benefit is clarity. Instead of one balance that includes everything, you can quickly see what’s already committed and what’s free to use.

This kind of setup doesn’t rely on memory or constant tracking. Your accounts do part of the work for you, which can make managing money feel less stressful.

A Real Example of How This Works

A simple example can make this easier to picture.

Let’s say your monthly income is $2,400, and your fixed expenses are about $1,450. This includes rent, utilities, internet, and insurance.

At the start of the month, you move $1,450 into your bills account so those payments are already covered.

That leaves $950 in your main account. From there, you might move $150 into savings and keep $800 in your spending account for groceries, transport, and everyday expenses.

Now your setup looks like this:

- Bills account → $1,450 (for fixed expenses)

- Spending account → $800 (for daily use)

- Savings → $150 (set aside)

With this setup, you don’t have to think about your bills during the month. Your spending account shows what’s available, and your savings stay separate.

Separate Accounts vs One Account (Simple Comparison)

Both setups can work. The difference is how easy they make your day-to-day decisions.

| Setup | How It Feels | What to Watch For |

|---|---|---|

| One account | Everything is in one place, but it can be harder to tell what’s already committed | Easier to spend money meant for bills |

| Separate accounts | Bills and spending are clearly divided, so you know what’s available | Requires a simple system to move money between accounts |

With one account, you rely more on tracking and memory. You need to remember which part of your balance is already planned for bills.

With separate accounts, your setup does that work for you. Your bills are already set aside, and your spending account shows what you can use.

This difference may seem small, but it can make everyday decisions feel much easier.

When Separating Accounts Helps — and When It Doesn’t

Separating your accounts can be useful, but it depends on how you manage your money day to day.

When it helps

- You often feel unsure how much you can safely spend

- Bills and everyday expenses get mixed up

- You want clearer boundaries without tracking every purchase

- You prefer a simple structure that guides your spending

When it might not help

- Your finances are already simple and easy to manage

- Your income is tight and splitting money feels restrictive

- You prefer keeping everything in one place

- Managing multiple accounts starts to feel like extra work

If it helps you stay clear on your spending and bills, it’s working. If it adds confusion, it may need to be simplified.

How to Set It Up Without Making It Complicated

You don’t need a detailed system to make this work. A simple setup is usually enough.

- Start with two accounts

One for bills and one for everyday spending is a good place to begin. - Decide what goes into each account

Set aside your fixed expenses first, then use the rest for daily spending. - Move money once at the start of the month

This reduces the need to keep transferring money throughout the month. - Keep it easy to manage

Avoid adding more accounts unless you have a clear reason.

The goal is to create a system you can follow without much effort. Small, consistent steps tend to work better than trying to set up something complex.

Does This Replace Budgeting?

Separating your accounts can make money easier to manage, but it doesn’t replace budgeting.

You still need a simple plan for how your income is used. Your accounts can help you follow that plan, but they don’t decide how much you should spend or save.

For example, you still need to know how much goes toward bills, spending, and savings each month. Once that’s clear, using separate accounts can make it easier to stick to those amounts.

Some people combine this approach with a basic budget or a simple tracking method. If you want a starting point, you can learn how to make a budget for beginners and then use your accounts to support that plan.

Separating your accounts works best as a tool that supports your decisions, not a replacement for them.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.