Better money habits are not about becoming perfect with money overnight. They are the small things you repeat often, like checking your spending, saving before you spend, and giving your money a simple plan.

And yes, small habits count. A weekly budget check may not feel exciting, but it can help you catch overspending before it turns into stress. Saving $20 at a time may not look huge at first, but it can slowly build the emergency fund you wish you had the last time life got expensive.

The goal is not to make your money life complicated. It is to make it easier to manage.

Better money habits can help you spend more intentionally, save more consistently, avoid common money mistakes, and feel more in control of your finances, one small step at a time.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

Quick Takeaways

- Better money habits are small actions you repeat, not huge changes you make once.

- Start with simple steps like tracking your spending, making a basic budget, and saving before you spend.

- You do not need to fix everything at the same time. One habit done consistently is better than five habits you quit after a week.

- Small money routines can help you avoid surprise expenses, reduce stress, and feel more in control.

- The best money habits are the ones that fit your real life, not someone else’s perfect-looking routine.

What Are Better Money Habits?

Better money habits are the small actions you repeat to manage your money more calmly and intentionally.

They are not about being perfect. They are about building simple routines that help you know where your money is going, spend with fewer regrets, save more consistently, and avoid financial surprises when possible.

For example, a better money habit could be checking your bank balance before payday, moving a small amount into savings each week, planning meals before grocery shopping, or waiting a day before buying something you do not really need.

Over time, these small habits can make money feel less chaotic. You may still have tight months, unexpected bills, or goals that take longer than planned, but you are less likely to feel completely lost when they happen.

Why Better Money Habits Matter

Better money habits matter because most financial progress comes from what you do repeatedly, not what you do once.

Saving $25 one time is helpful. Saving $25 every week creates a routine. Checking your spending once may show you where your money went. Checking it regularly can help you catch small problems before they become stressful.

Good money habits can also make everyday decisions easier. When you already know how much you can spend, what bills are coming up, and what goal you are working toward, you do not have to guess your way through every purchase.

That does not mean money will suddenly become easy. Life can still be expensive, and unexpected costs still happen. But better habits give you a little more structure, and sometimes that structure is exactly what keeps one bad week from turning into a bad month.

15 Better Money Habits to Start Building

Better money habits do not need to be dramatic. You do not have to change your whole life by Monday morning or suddenly become the type of person who lovingly updates a spreadsheet for fun.

Start with a few habits that feel realistic right now. Once those become easier, you can add more.

Track Your Spending Once a Week

Tracking your spending helps you see what is actually happening with your money, not what you hope is happening.

You do not need to write down every purchase forever. Start by checking your bank account or expense tracker app once a week. Look at where your money went, what surprised you, and whether your spending matched your priorities.

For example, you might notice that a few small food delivery orders added up to more than expected. That does not mean you failed. It simply gives you useful information, and useful information is much better than guessing.

A simple weekly check can help you spot patterns, reduce impulse spending, and make better decisions before the month gets away from you.

Create a Budget You Can Actually Follow

A budget should help you manage your money, not make you feel like you are doing financial homework with a strict teacher watching.

Start with your monthly income and your main expenses: rent or mortgage, utilities, groceries, transportation, debt payments, savings, and regular bills. Then give yourself a realistic amount for flexible spending, like eating out, entertainment, personal care, or small treats.

The key word is realistic. If you normally spend $500 a month on groceries, setting a $250 grocery budget overnight may look good on paper, but it will probably fall apart by week two.

A better approach is to make small adjustments. Maybe you reduce one category by $25 or $50 first, then see how it feels. A budget that bends with real life is much easier to keep than one that breaks the first time something unexpected happens.

Save Before You Spend

One of the simplest better money habits is to save first, not only if there is money left over.

When saving depends on “whatever is left at the end of the month,” it often gets pushed aside by groceries, bills, small purchases, and those random expenses that seem to appear from nowhere. A few dollars here, a quick online order there, and suddenly your savings plan has quietly left the room.

Try moving a set amount into savings as soon as you get paid. It does not have to be huge. Even $10, $25, or $50 per paycheck can help you build the habit.

The goal is to make saving part of your regular routine, not something you only do during a perfect month. A simple payday routine can make this easier because it helps you set aside money for bills, savings, and spending before your paycheck starts disappearing.

Automate Bills and Savings

Automation can make better money habits easier because it removes some of the “I’ll do it later” problem.

Set up automatic transfers to savings right after payday, even if the amount is small. This helps you save before the money gets mixed into regular spending.

You can also automate important bills, such as rent, insurance, utilities, loan payments, or credit card minimums. This can help you avoid late fees and missed due dates.

Just make sure you still check your accounts regularly. Automation is helpful, but it is not a reason to ignore your money completely. Think of it as a backup system, not a magic button.

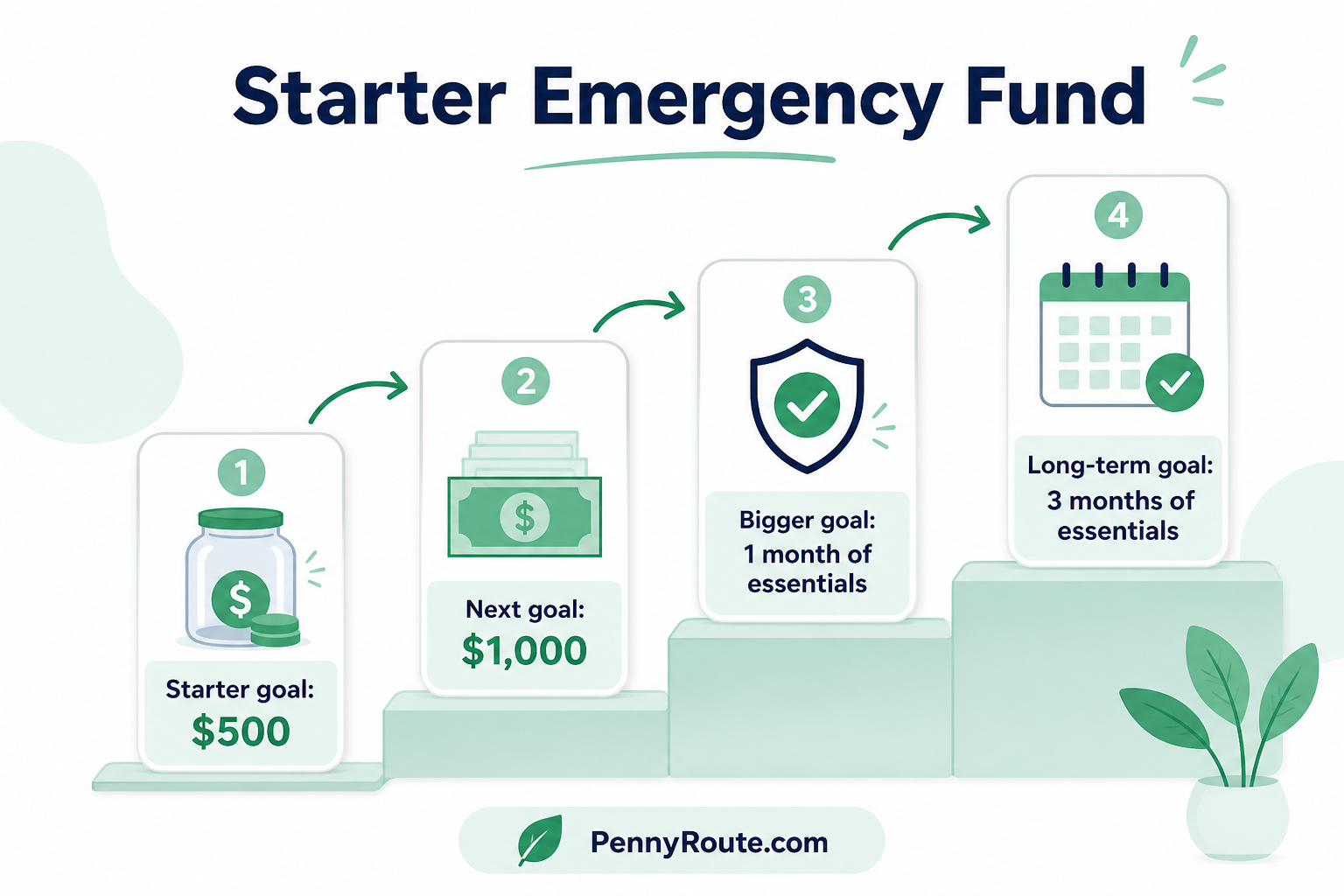

Build a Starter Emergency Fund

An emergency fund gives you a small cushion when life gets expensive without asking politely first.

Start with a realistic first goal, such as $500 or $1,000. That may not cover every emergency, but it can help with smaller surprises like a car repair, urgent bill, minor medical cost, or replacing something essential at home.

Once you reach that starter amount, you can slowly work toward a bigger goal, such as one month of essential expenses, then three months if possible.

Keep this money separate from your everyday spending account so it does not disappear into normal purchases. Your emergency fund is not for vacations, shopping, or “I deserve this” moments. It is there to protect you when something genuinely important cannot wait.

Pay Down High-Interest Debt First

High-interest debt can make it harder to move forward because the balance may keep growing even while you are making payments.

Credit cards, payday loans, and other high-interest balances usually need attention first because they can cost you the most over time. Even a small extra payment can help if you do it consistently.

There are two common ways to approach debt payoff:

- Debt avalanche: Pay extra toward the debt with the highest interest rate first while making minimum payments on the rest.

- Debt snowball: Pay extra toward the smallest balance first while making minimum payments on the rest.

The avalanche method can save more money on interest. The snowball method can feel more motivating because you get quicker wins.

The best method is the one you can stick with. Paying off debt is not just math. It is also momentum, patience, and not adding new debt while trying to clean up the old one.

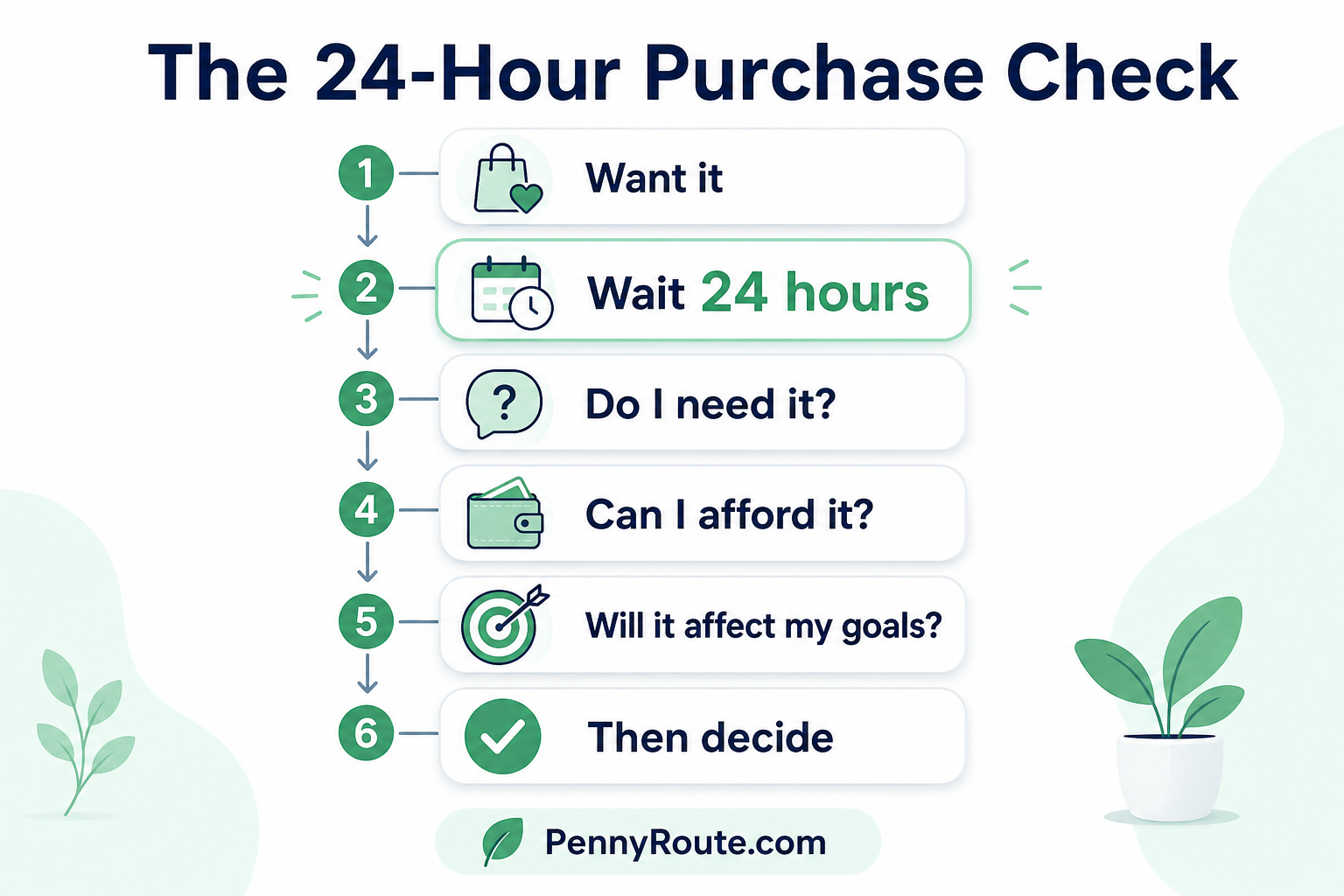

Use a Waiting Period Before Big Purchases

A waiting period can help you slow down before spending money on something you may not actually need.

This does not mean you have to overthink every small purchase. If you need toothpaste, buy the toothpaste. No one needs a 24-hour reflection period for basic hygiene.

But for non-essential purchases, try waiting at least 24 hours before buying. For bigger purchases, you may want to wait a few days or even a full week.

During that time, ask yourself:

- Do I still want this, or was it just an impulse?

- Can I afford it without using debt?

- Will this affect a bill, savings goal, or emergency fund?

- Is there a cheaper option that would work just as well?

Sometimes you will still decide to buy it, and that is okay. The goal is not to never spend money. The goal is to spend with fewer regrets.

Review Subscriptions and Small Charges

Small charges can quietly drain your budget because they do not feel like much on their own.

A $7 app, a $12 streaming service, a $15 subscription box, and a few small monthly fees may not seem serious at first. But together, they can turn into money you barely notice leaving your account.

Once a month, review your bank or credit card statement and look for recurring charges. Ask yourself:

- Do I still use this?

- Would I sign up for it again today?

- Is there a cheaper plan?

- Can I pause or cancel it for now?

You do not have to cancel everything fun. The goal is to stop paying for things you forgot about, no longer use, or only keep because canceling sounds mildly annoying.

Plan Your Grocery Spending

Groceries are one of the easiest areas to overspend because prices change, cravings happen, and somehow one “quick trip” can turn into a cart full of snacks, sauces, and one very optimistic bag of spinach.

Planning your grocery spending does not mean eating boring meals. It means going in with a simple plan so you are not making every decision while standing in the store.

Before you shop, check what you already have at home. Then plan a few meals around those items, write a list, and try to stick to it. You can also choose cheaper staples like rice, pasta, beans, eggs, oats, frozen vegetables, and seasonal produce.

A simple grocery habit can make a big difference: plan meals before you shop, not after you have already spent the money.

Set One Clear Money Goal at a Time

Trying to fix every money goal at once can get overwhelming fast.

You may want to save for an emergency fund, pay off debt, invest more, build a car fund, plan a vacation, and stop overspending, preferably by next Friday. That is a lot for one budget to carry.

A better habit is to choose one main goal for the season. For example:

- Save your first $500 emergency fund

- Pay off one credit card

- Save $1,000 for car repairs

- Build one month of essential expenses

- Stop using credit cards for everyday purchases

This does not mean your other goals do not matter. It simply gives your money a clear direction. When one goal is finished or stable, you can move to the next one with more focus and less mental clutter.

Use Extra Money With a Plan

Extra money can disappear quickly when it does not have a job.

A tax refund, work bonus, cash gift, side hustle payment, or leftover money at the end of the month can feel like “free money.” It is not wrong to enjoy some of it, but it helps to decide what you want it to do before it gets absorbed into random spending.

You could split extra money into simple categories:

- Save part of it

- Use part of it for debt

- Put part of it toward a goal

- Keep a small amount for fun

For example, if you receive $300, you might put $150 into your emergency fund, $100 toward debt, and keep $50 for something you enjoy.

That way, you make progress without feeling like every extra dollar has to be locked away forever.

Check Your Accounts Regularly

Checking your accounts regularly helps you catch problems early, before they turn into bigger money headaches.

This habit can help you spot:

- Unexpected fees

- Duplicate charges

- Forgotten subscriptions

- Low balances before bills are due

- Spending that is higher than you expected

You do not need to check your bank account ten times a day. That can make money feel more stressful, not less.

A simple routine works better. Check your checking account, savings account, and credit card balances once or twice a week. Make sure recent transactions look right and that upcoming bills have enough money set aside.

Think of it like checking the weather before leaving the house. You may not love what you see every time, but it is better than being surprised by a financial rainstorm.

Learn One Money Topic Each Week

You do not need to understand every part of personal finance at once. That is a fast way to feel overwhelmed and close the tab.

Instead, build the habit of learning one small money topic each week.

You could read about:

- How credit scores work

- How emergency funds help

- How interest charges add up

- How to compare savings accounts

- How to lower grocery spending

- How to start a simple budget

Keep it practical. Choose topics that connect to your real life right now. If you are trying to stop overspending, learn about impulse spending. If you are building savings, learn about emergency funds or automatic transfers.

Small weekly learning adds up. The more you understand your money, the less confusing your choices start to feel.

If investing is your next learning topic, Investor.gov’s beginner investing resources are a good place to understand the basics before making decisions.

Stop Comparing Your Finances to Others

Comparing your money life to someone else’s highlight reel can make you feel behind, even when you are making real progress.

You may see people buying homes, taking trips, upgrading cars, or posting perfect-looking routines online. What you usually do not see is their debt, family support, income, stress, or the trade-offs behind those choices.

A better habit is to measure your progress against your own starting point.

Ask yourself:

- Am I tracking my money more often than before?

- Did I save something this month, even if it was small?

- Did I avoid one purchase I would usually regret?

- Did I pay a little extra toward debt?

- Do I understand my money better than I did last month?

Your financial life does not need to look impressive to be improving. Quiet progress still counts.

Review Your Progress Monthly

A monthly money review helps you see what is working, what needs adjusting, and where your money may be drifting.

Set aside a little time once a month to look at your income, bills, spending, savings, and debt progress. This does not need to be a dramatic meeting with charts, candles, and a serious face. A simple 20-minute check is enough.

Look for answers to a few basic questions:

- Did I stay close to my budget?

- What expense surprised me this month?

- Did I save anything?

- Did my debt go up or down?

- What should I adjust next month?

This habit keeps your money plan connected to your real life. If groceries went up, your budget may need a change. If you saved more than expected, you can decide where that extra progress should go next.

Better money habits are easier to keep when you check in regularly instead of waiting until something feels wrong.

How to Start Building Better Money Habits This Week

You do not need to start all 15 habits at once. That would be exhausting, and honestly, probably not very fun.

A better approach is to choose a few simple actions you can do this week.

Here is an easy starting plan:

- Day 1: Check your bank account and recent transactions.

- Day 2: Write down your main monthly bills.

- Day 3: Choose one spending category to watch more closely.

- Day 4: Move a small amount into savings, even if it is just $5 or $10.

- Day 5: Cancel or pause one subscription you do not use.

- Day 6: Plan your next grocery trip before you shop.

- Day 7: Pick one money goal to focus on for the next month.

The point is not to do everything perfectly. The point is to prove to yourself that you can take small steps and keep going.

Once one habit feels normal, add another. That is how better money habits become part of your routine instead of another thing on your already-too-long to-do list.

Small Habits Can Make Money Feel Less Overwhelming

Better money habits do not have to be big, complicated, or perfect to make a difference.

Most progress starts with simple actions you repeat: checking your spending, saving a little before you spend, planning purchases, reviewing your accounts, and choosing one clear goal at a time.

You may still have months where the budget feels tight or an unexpected bill throws things off. That does not mean you failed. It means your money plan needs a small adjustment, not a full restart.

Start with one habit that feels doable this week. Keep it simple, repeat it often, and build from there. Small steps count, especially when you keep taking them.

FAQs About Better Money Habits

What are better money habits?

Better money habits are simple routines that help you manage your money more intentionally. They can include tracking your spending, saving before you spend, paying bills on time, reviewing your accounts, and setting clear financial goals.

How do I start building better money habits?

Start with one small habit that feels realistic, such as checking your spending once a week or moving a small amount into savings after payday. Once that feels easier, add another habit.

What is the most important money habit?

One of the most important money habits is knowing where your money is going. Tracking your spending helps you spot patterns, avoid surprises, and make better decisions with your money.

How long does it take to build better money habits?

It depends on the habit and your situation. Some habits may feel normal after a few weeks, while others, like budgeting or paying down debt, may take longer.

What are bad money habits to avoid?

Common bad money habits include spending without checking your budget, ignoring bills, relying on credit cards for everyday expenses, keeping unused subscriptions, and comparing your finances to others.

Can better money habits help if I live paycheck to paycheck?

Yes, better money habits can help you plan bills, avoid some fees, track spending, and start saving small amounts when possible. But if your income barely covers essentials, the issue may also involve low income, high costs, or debt, not just habits.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.