Overspending can sneak up on you. One minute, you’re buying “just one thing.” Then it’s a takeout order, a sale item, a subscription you forgot about, and a quick online purchase that somehow becomes a small financial mystery.

If you’ve been wondering how to stop overspending, the answer is not always “try harder” or “never buy anything fun again.” That usually does not work for long. Overspending often happens because spending is too easy, triggers are everywhere, and your money does not have clear boundaries.

This 7-day reset will help you slow things down, spot your biggest spending leak, and build simple rules that make your money easier to control.

You do not need a perfect budget to start. You just need one week, one honest look at your spending, and a few small changes that make overspending less automatic.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making financial decisions.

Why Overspending Happens So Easily

Overspending is not always about being careless with money.

Sometimes, it happens because spending has become too fast, too convenient, or too emotional. You may not even notice the pattern until your account balance drops lower than expected.

Here are a few common reasons overspending happens.

Spending Is Almost Too Easy

A saved card, one-click checkout, food delivery app, or “buy now, pay later” button can turn a quick thought into a purchase in seconds.

That convenience is helpful sometimes, but it also removes the pause that gives you time to think.

When buying something takes almost no effort, it becomes easier to spend money before asking, “Do I actually want this?”

Emotions Can Push You Toward Spending

Stress, boredom, frustration, excitement, and comparison can all lead to extra spending.

You might order takeout after a hard day, buy something online because you’re bored, or spend more after seeing what someone else has. The purchase may make the moment better, but the relief usually fades faster than the charge on your card.

That does not mean you are bad with money. It means your spending has a trigger.

Small Purchases Add Up Quietly

Overspending is not always one big expensive mistake.

It can be a few small purchases repeated often:

- $9 here

- $14 there

- $6 every morning

- $30 “just this once”

- $12 for a subscription you forgot about

Individually, these purchases may not seem serious. Together, they can quietly drain money you meant to save.

A Too-Strict Budget Can Backfire

Sometimes people overspend because their budget leaves no room for real life.

If your plan says you can never eat out, never buy coffee, never enjoy a small treat, and never have a fun purchase, it may look great on paper. But after a few stressful days, that kind of budget can become hard to follow.

A realistic plan works better than a perfect one you abandon by Friday.

The 7-Day Overspending Reset Plan

You do not have to fix every spending problem at once.

Trying to cut everything overnight can make the process harder than it needs to be. A reset works better when it gives you one clear step per day, so you can slow down, notice your patterns, and make spending less automatic.

Here’s a simple 7-day plan to help you stop overspending without turning your budget into a punishment.

Day 1: Look at Your Last 30 Days of Spending

Start by looking at where your money actually went over the last month. The Consumer Financial Protection Bureau also offers simple budgeting worksheets if you want a basic way to list income, expenses, and spending patterns.

You can use your bank app, credit card statement, budgeting app, or a simple notebook. You are not here to judge every purchase. You are looking for patterns.

If you need a more detailed starting point, learning how to track your expenses can help you see where your money is actually going.

Look for categories that surprise you, such as:

- Takeout or food delivery

- Groceries

- Clothes

- Online shopping

- Coffee or snacks

- Subscriptions

- Convenience store purchases

- Entertainment

- Kids’ items

- Home goods

Then ask one simple question:

“Which category is causing the most damage right now?”

Do not pick five categories. Pick one.

For example, if you spent $280 on takeout last month and expected it to be closer to $100, that is your starting point. If online shopping kept popping up every few days, start there.

This step gives you a clear target, which is much easier than saying, “I need to stop spending money” without knowing where the money is going.

Day 2: Pick One Problem Category

Once you find the spending area that stands out, make that your focus for the week.

This matters because overspending can feel bigger when you try to fix everything at once. You may want to cut takeout, cancel subscriptions, spend less on clothes, stop impulse buying, lower grocery costs, and save more money all at the same time.

That sounds productive, but it can become overwhelming quickly.

Instead, choose one category and give it a simple limit.

For example:

- Takeout: $40 this week

- Online shopping: no new purchases for 7 days

- Groceries: use a list before every trip

- Clothes: wishlist only this week

- Coffee: 2 paid coffees this week, then make it at home

- Convenience purchases: avoid gas station snacks and random add-ons

You are not trying to become perfect overnight. You are creating one clear boundary you can actually follow.

If takeout is your problem category, do not worry about fixing every other spending habit this week. Just focus on making takeout less automatic.

A small, specific rule is easier to follow than a vague promise like “I’ll be better with money.”

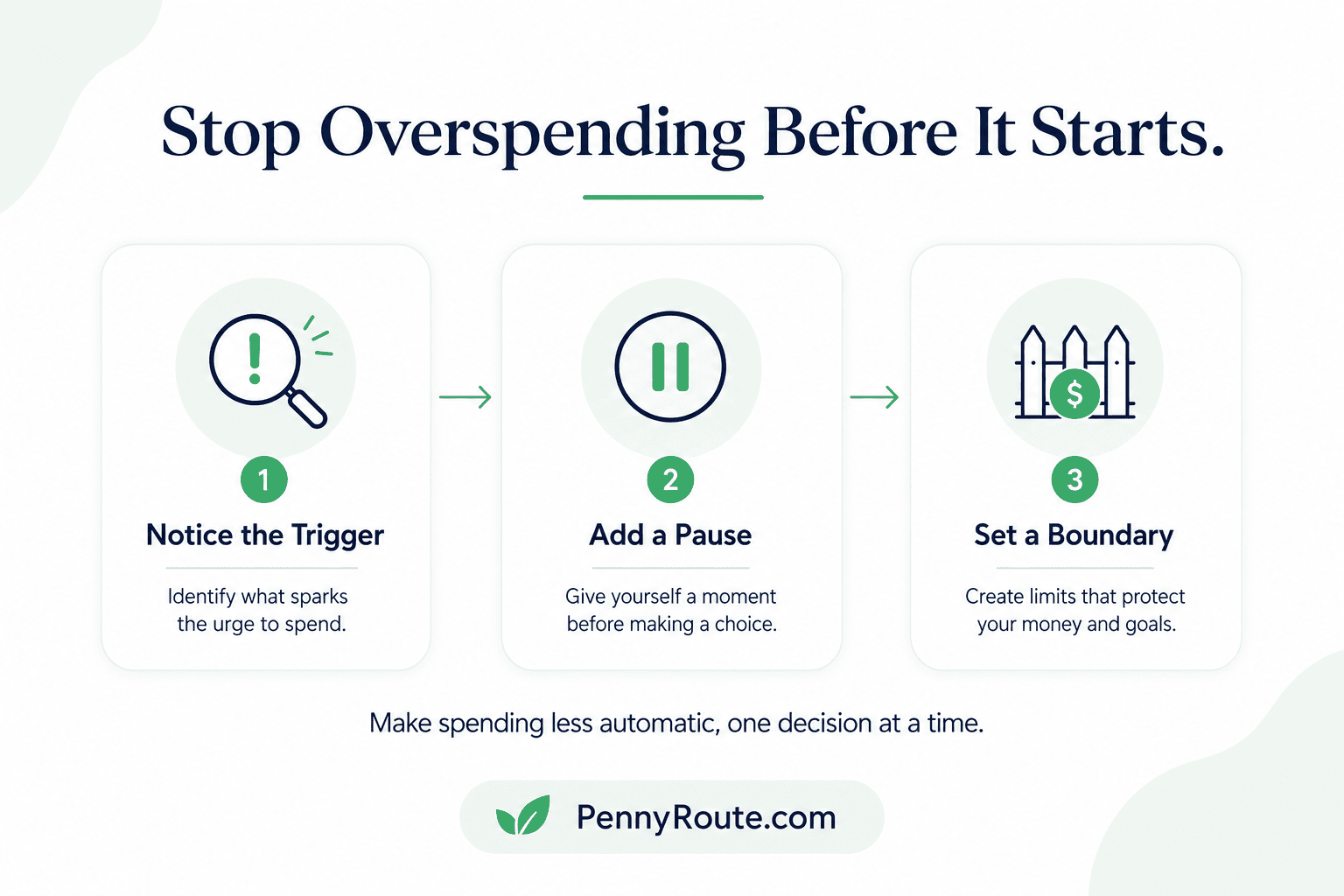

Day 3: Add a Spending Pause

Overspending often happens in the gap between wanting something and thinking it through.

That gap can be tiny. You see something, you want it, you tap “buy,” and the decision is over before your budget gets a vote.

A spending pause helps you slow that moment down.

For non-essential purchases, try this simple rule:

- Under $25: wait 24 hours

- $25 to $100: wait 48 hours

- Over $100: wait one week

You can adjust the amounts based on your budget, but keep the idea the same: the bigger the purchase, the longer the pause.

During the waiting period, add the item to a wishlist instead of buying it right away. After the pause, ask yourself:

- Do I still want this?

- Do I need it this week?

- Can I afford it without using bill money?

- Will this help me, or am I just buying it because I’m bored, stressed, or tempted by a sale?

This is especially useful for online shopping, clothes, home decor, gadgets, and “limited-time” deals.

A pause does not mean you can never buy anything. It just gives your future self a chance to join the conversation before your card does.

Day 4: Remove Easy Spending Triggers

If you want to stop overspending, make unnecessary spending a little less convenient.

This is not about making your life difficult. It is about adding enough friction that you have time to think before buying.

Start with the places where you spend without planning:

- Shopping apps

- Food delivery apps

- Store emails

- Sale text alerts

- Saved cards

- One-click checkout

- Browser payment autofill

- “Buy now, pay later” shortcuts

You do not have to delete everything forever. Try removing the biggest trigger for one week.

For example, if food delivery is your weak spot, delete the app for 7 days and keep two easy backup meals at home. If online shopping is the issue, log out of your favorite stores and remove your saved payment details.

The small delay matters.

When you have to find your card, type in the details, or log back into an app, you get a few extra seconds to ask, “Do I really want this, or am I just making a quick mood purchase?”

That pause can save more money than you think.

Day 5: Set a Weekly Fun Money Limit

Stopping overspending does not mean cutting out every enjoyable purchase.

In fact, that can make things worse. If your budget has no room for small treats, coffee with a friend, a movie night, or a random “I just want this” purchase, you may eventually rebel against your own plan.

Instead, give yourself a clear fun money limit.

This is money you can spend without guilt, as long as it stays within the amount you chose.

For example:

- $15 per week for coffee or snacks

- $25 per week for small personal purchases

- $40 per week for takeout

- $60 per month for hobbies, games, or entertainment

The amount depends on your income, bills, savings goals, and current situation. The key is to make it realistic.

If you can afford $20 a week, do not pretend you have $100. If you can afford $60 a week, you do not have to force yourself down to $5 just to prove a point.

A fun money limit gives your spending a boundary without making your budget miserable.

Once the money is gone, pause until next week. That one rule can help you enjoy small purchases without letting them quietly take over your savings.

Day 6: Separate Spending Money From Bill Money

Overspending becomes easier when all your money sits in one place.

If your rent money, grocery money, savings, bill payments, and fun money are all mixed together, your bank balance can look more available than it really is.

For example, seeing $900 in your checking account does not mean you have $900 to spend. Some of that money may already belong to rent, utilities, insurance, subscriptions, groceries, or upcoming payments.

A simple way to fix this is to separate your spending money from your bill money.

You can do this with:

- A second checking account

- A separate savings account

- Cash envelopes

- Digital bank “buckets”

- A prepaid card for personal spending

- A simple note in your budgeting app

The exact method matters less than having a clear boundary.

If you like clear spending limits, the envelope budgeting method can make this easier to manage.

For example, you might keep bill money in your main checking account and move only your weekly spending money to a separate account or card. Once that spending money is gone, you know it is time to pause instead of accidentally dipping into bill money.

This works especially well for categories that tend to run away from you, like eating out, shopping, hobbies, or entertainment.

You are not trying to make money complicated. You are making it easier to see what is actually safe to spend.

Day 7: Review and Adjust

At the end of the week, take 10 minutes to review what happened.

This step matters because stopping overspending is not only about setting rules. It is about learning which rules actually work for your real life.

Look back at the category you chose on Day 2 and ask:

- Did I stay within the limit?

- What made spending easier to control?

- What made it harder?

- Did I overspend at a certain time, place, or mood?

- Was my limit realistic?

- What should I change next week?

For example, maybe you stayed under your takeout limit because you had easy meals ready at home. Or maybe you still overspent on online shopping because you kept checking sale emails during lunch breaks.

That is useful information.

Do not treat the review like a pass-or-fail test. Treat it like a money check-in.

If something worked, keep it. If something did not work, adjust it. Maybe your fun money limit was too low. Maybe your trigger was not the shopping app but scrolling when you were bored. Maybe you need a separate account, not just a note in your budget.

By the end of the week, you should have one better rule than you had before.

What to Do If You Overspend Again

Overspending once does not mean the whole plan failed.

It means something in the plan needs a closer look. Maybe the limit was too tight, the trigger was stronger than expected, or you forgot to plan for something that was actually realistic.

Start by pausing, not panicking.

Look at the purchase or category that went over and ask:

- What happened right before I spent the money?

- Was I tired, stressed, bored, hungry, or rushed?

- Did I spend because it was convenient?

- Did I forget about an upcoming bill?

- Was my weekly limit too low for real life?

Then make one small adjustment.

If you overspent on takeout, plan two easy backup meals for next week. If online shopping was the issue, remove one more trigger, like sale emails or saved payment details. If groceries went over, check whether your budget was too low or if impulse items were the problem.

Try not to “fix” overspending by using credit cards for things you cannot currently afford. That can turn a short-term spending mistake into a longer-term debt problem.

If needed, move money from a lower-priority category to cover the gap. For example, you may pause entertainment spending for a few days to cover extra groceries or takeout. That is not ideal, but it is better than ignoring the problem.

This is not about punishing yourself. It is about understanding the pattern and making the next overspending moment harder to repeat.

When Overspending Is Not Just a Spending Problem

Sometimes overspending is not only about impulse buying or weak boundaries.

Sometimes the bigger issue is that your budget does not match your real life.

If your rent, bills, debt payments, groceries, insurance, childcare, or transportation costs are taking up most of your income, it may look like you are overspending when you are actually under too much financial pressure.

That is an important difference.

For example, if you earn $2,800 per month and your rent, utilities, car payment, insurance, debt payments, and groceries already take $2,600, the problem may not be coffee or takeout. The real issue is that your budget has almost no breathing room.

In that case, cutting small purchases can help a little, but it may not solve the bigger problem.

You may need to look at:

- Lowering fixed expenses where possible

- Reviewing debt payments

- Building a small emergency fund

- Finding ways to increase income

- Adjusting your budget categories

- Looking for cheaper options on recurring bills

- Getting help from a qualified financial counselor if debt feels unmanageable

This does not mean small spending choices do not matter. They do.

But if the numbers are too tight from the start, blaming yourself for every small purchase will not help much. You need a plan that looks at the full picture, not just the receipt from yesterday.

Start With One Spending Pattern

Learning how to stop overspending does not mean fixing every bad spending habit at once.

Start with one pattern you can clearly see: takeout after work, online shopping at night, grocery trips without a list, or spending more than planned after payday.

Then add one simple boundary. Delete the app for a week. Set a fun money limit. Wait 48 hours before buying non-essentials. Move bill money away from spending money.

Small changes work because overspending usually happens in repeated moments, not one dramatic decision.

You do not need to become perfect with money by next week. You just need to make the next spending decision a little more intentional.

FAQs About How to Stop Overspending

Why do I keep overspending?

You may keep overspending because spending is tied to convenience, emotions, habits, or unclear limits.

For example, if your card is saved in every shopping app, your budget has no fun money, and you usually shop when you are stressed, overspending becomes easier to repeat.

How do I stop impulse buying?

To stop impulse buying, add a waiting period before non-essential purchases.

Try waiting 24 hours for small purchases, 48 hours for medium purchases, and one week for bigger purchases. That pause gives you space between ‘I want this’ and ‘I bought this.

How do I stop overspending on food?

Start by separating food spending into two categories: groceries and takeout.

Then choose one area to improve first. If takeout is the problem, keep easy backup meals at home. If groceries are the issue, shop with a list, check your pantry before going, and avoid adding random extras to your cart.

How do I stop overspending with a credit card?

Set a weekly spending limit and check your balance more often than once a month. You can also turn on purchase alerts, remove your card from shopping apps, or use debit/cash for categories where you tend to overspend.

Is overspending always bad?

Not every extra purchase is a problem. Overspending becomes an issue when it regularly affects your bills, savings, debt payments, emergency fund, or peace of mind. A planned treat is different from repeated spending that keeps pushing your goals further away.

PennyRoute Editorial creates beginner-friendly guides on budgeting, saving, and everyday money habits. Our goal is to make personal finance easier to understand with clear explanations, realistic examples, and practical steps.